Survey: M4.0 Appears Poised for A Significant Leap

Manufacturers are ramping up digital investments, with AI, automation, and smart factories reshaping the industry faster than ever.

KEY TAKEAWAYS:

● Digital transformation is a game changer. Sixty percent see it as a defining shift for the industry, marking a strong rebound in enthusiasm after a dip in 2024.

● Manufacturers digital maturity continues to increase as 75% believe they are at a mid-level maturity—up significantly from the 2024 and 2023 survey results.

● AI expectations have rebounded. A full 80% now fully or partially agree that self-managing and self-learning facilities powered by AI and machine learning are on the horizon.

Manufacturers are charging ahead with their digital transformation efforts. The Manufacturing Leadership Council’s Smart Factories and Digital Production Survey reveals an increase in smart factory maturity and optimism about continued digitization and adoption.

Fueled by an expectation of economic growth and a corresponding plan to increase or maintain smart factory investments, respondents share an outlook that includes AI adoption, end-to-end digitization, and belief that the game changing power of digital transformation is moving beyond mere table stakes.

Section 1: Economic Outlook and Investment Trends

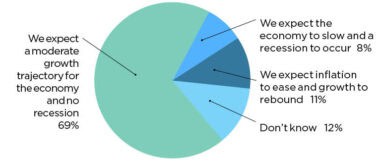

Manufacturers are optimistic about the economy in 2025, with 69% expecting moderate growth and no recession, while only 8% anticipate an economic slowdown. Encouragingly, 11% expect inflation to ease and growth to rebound, signaling greater confidence in market stability. (Chart 1)

This optimism extends to smart factory investments, with 89% of manufacturers planning to maintain or increase spending in 2025. Within that number, it’s notable that 44% expect to ramp up investments, aligning with a broader push for digital transformation. (Chart 2) In the 2024 version of this survey, only 9% expected to increase their Manufacturing 4.0 investment.

Meanwhile, only 8% foresee a decline in spending in 2025, underscoring that despite economic fluctuations, smart factory adoption remains a strategic priority. The data suggests that as confidence in economic growth solidifies, companies are doubling down on automation and digitalization efforts to remain competitive.

1. Strong Majority See Growth on the Horizon

Q: What is your company’s outlook for the economy in 2025? (Select one)

2. 89% see smart factory investments increasing or remaining unchanged

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2025? (Select one)

Section 2: Smart Factory Maturity and Adoption

The digital transformation journey continues to advance, with manufacturers steadily maturing their smart factory strategies. Compared to previous years, the percentage of companies rating themselves at lower maturity levels (1-3) has declined significantly, from 57% in 2024 to just 16% in 2025. Meanwhile, those ranking their factories at a mid-level maturity (4-7) increased to 75%—up from 42% in 2024 and 58% in 2023—and 9% now place themselves in the advanced range (8-10). (Chart 3)

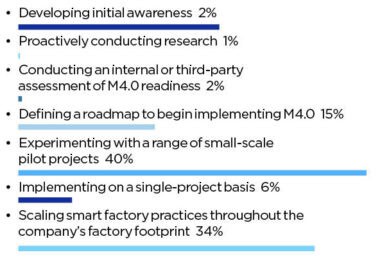

While progress is evident, most companies are still in experimental phases—40% are piloting small-scale projects and 6% are implementing on a single-project basis. Meanwhile, 34% are scaling these initiatives company-wide. Only 15% are just beginning their digital journey, emphasizing a strong industry-wide shift toward implementation. (Chart 4)

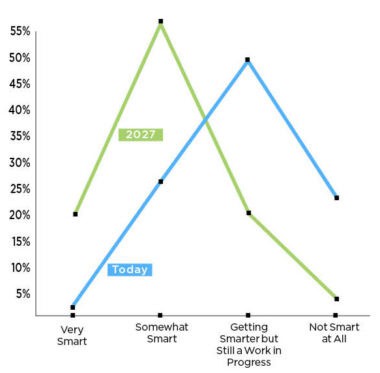

In fact, only 28% believe their factories are very smart or somewhat smart today. That number is expected to skyrocket to 76% by 2027. (Chart 5)

For this to happen, specific functional areas must advance. So it is a positive that manufacturers aspire to reach advanced adoption in every area included in our survey. Many find themselves in the intermediate range, with procurement/inventory management the area most ripe to move from early adoption to this stage. (Chart 6)

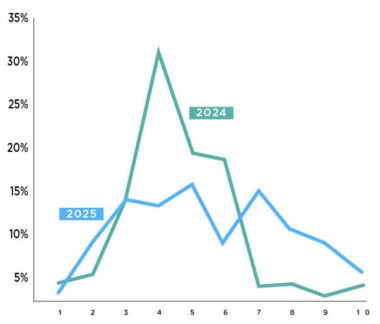

Despite this, full integration with business strategy remains a work in progress, with just 24% rating their integration at eight or higher on a 10-point scale, though this is an improvement from 7% in 2024. (Chart 7)

3. Smart factory journeys continue to mature

Q: How would you assess the maturity level of your smart factory journey? (Scale of 1-10, with 10 being the highest level of digital maturity)

4. Most experimenting with small-scale pilots or scaling smart factory practices

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today? (Select one)

5. Smart factory explosion expected by 2027

Q: How “smart” do you consider your factory and plant operations to be today and what do you anticipate they will be by 2027?

6. Manufacturers still striving to reach advanced digital adoption stages

Q: At what stage of digital adoption are the following functions in your company? (Rate as early, intermediate or advanced)

7. Smart factory strategy becoming more integrated with business strategy

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy? (Scale of 1-10, where 10 is fully integrated)

Section 3: Digitization and Automation Growth

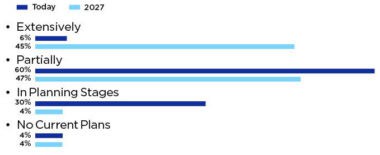

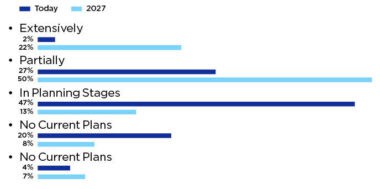

Manufacturers anticipate a significant leap in factory-wide digitization by 2027. Today, only 2% report being extensively digitized, but this is expected to surge to 38% within the next two years. Similarly, partial digitization is set to grow from 47% to 52%, while the number of companies still in planning stages will plummet from 43% to just 5%. (Chart 8)

Production and assembly processes are on a similar trajectory. Only 6% of companies currently consider these processes extensively digitized, but this figure is projected to jump to 45% by 2027. (Chart 9)

Integration with customers and suppliers, however, remains a weak spot—just 2% report extensive digital connectivity today, though 22% expect to achieve this by 2027. (Chart 10)

Taken together, these findings highlight a growing recognition of end-to-end digital transformation as essential for operational agility and supply chain resilience, while identifying an opportunity for improved digitization between manufacturers and their customers and suppliers.

8. Significant end-to-end digitization on the horizon

Q: To what extent are your factory operations fully digitized end to end today, and what do you anticipate they will be by 2027?

9. 92% predict extensive or partial digitization of production/assembly by 2027

Q: To what extent are your production/assembly processes digitized today, and what do you anticipate they will be by 2027?

10. Digital integration with customers and suppliers lags behind in-house digitization

Q: To what extent are your production functions digitally integrated with customers and suppliers today, and what do you anticipate they will be by 2027?

Section 4: Future of Factory Models and AI-Driven Operations

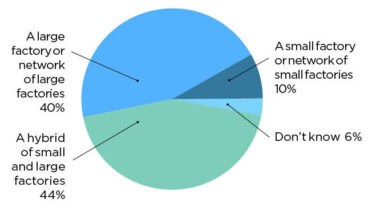

Manufacturers envision a hybrid future for their factory networks, with 44% expecting a mix of small and large facilities, reflecting the need for both localized agility and economies of scale. Large-scale production remains dominant, with 40% favoring large factories or networks of large facilities, while only 10% see a shift toward smaller, more agile production models. (Chart 11)

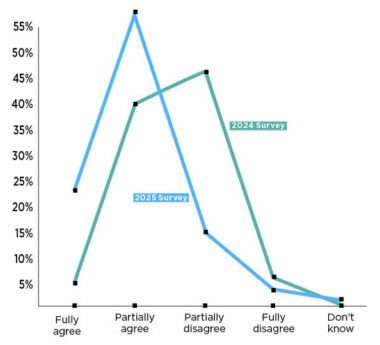

AI-driven automation is also gaining traction. Almost one quarter (23%) of manufacturers fully agree that factories will evolve into self-managing, self-learning facilities, a dramatic increase from just 6% in 2024. Another 57% partially agree, suggesting growing confidence in AI’s ability to optimize operations. This shift reflects the industry’s increasing focus on AI-driven decision-making and predictive analytics as key enablers of the smart factory vision. (Chart 12)

11. Only 10% see small, agile factories and networks as the future

Q: What is the expected future state of your factory model?

12. Expectation of self-managing, self-learning factories increase significantly

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.”

Section 5: Technology Adoption and Priorities

The 2025 survey highlights strong momentum in advanced technologies, particularly cybersecurity (73% scaling/at scale), IIoT sensor networks (46% scaling/at scale), and advanced analytics (56% scaling/at scale). AI adoption is also accelerating, with 22% of manufacturers now scaling/at scale with AI solutions, and another 42% piloting at least one AI project. Machine learning follows a similar trend, with 21% scaling/at scale and 29% planned for future deployment by 2027. (Chart 13)

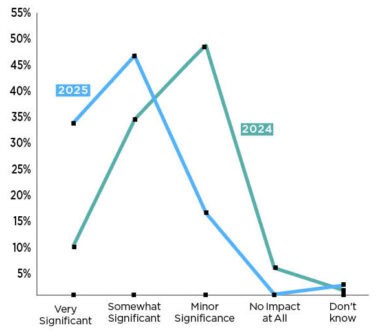

AI’s perceived impact is rising sharply—34% now see it as very significant, compared to just 10% in 2024. (Chart 14) This signals a shift from experimentation to real-world application, as manufacturers increasingly leverage AI for predictive maintenance, process optimization, and adaptive automation. However, emerging technologies like the metaverse, blockchain, and exoskeletons remain niche, with over 70% of companies having no plans to adopt any of them. (Chart 13)

13. Cyber, advanced analytics, IIoT sensor networks top production operations tech list

Q: Where does your company stand in regard to the following technologies in its production operations?

14. AI’s expected significance increases

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations?

Section 6: Challenges and Benefits of Digital Transformation

Manufacturers continue to grapple with major roadblocks in their smart factory journeys. Nearly half (49%) cite outdated legacy equipment as their top challenge, up from 39% in 2024, highlighting the complexity of modernization. Workforce-related barriers are also growing—43% point to a lack of skilled employees, a sharp increase from 24% in 2024. Resistance to change remains a persistent issue, with 42% citing organizational culture as a challenge, though this has improved from 53% last year.

But it’s not all bad news. In 2024, a lack of leadership buy-in and access to adequate budget/investment both ranked among the top four roadblocks. Improvements have been seen in both these issue areas. Leadership buy-in and increasing budgets may very well prove to be leading indicators that the current issues discussed above may become lower hurdles rather than roadblocks. (Chart 15)

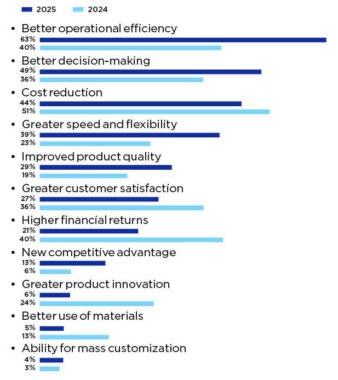

Despite these current roadblocks, companies recognize the benefits of transformation. Nearly two-thirds (63%) rank operational efficiency as the top expected gain, a significant jump from 40% in 2024. Better decision-making (49%) and cost reduction (44%) follow closely, demonstrating that digital adoption is increasingly seen as a performance and profitability driver. (Chart 16)

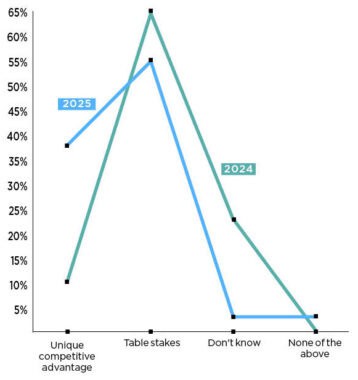

Notably, the percentage of companies expecting digital transformation to create a competitive advantage has soared from 11% in 2024 to 38% in 2025. While the majority still see digital transformation as table stakes, the dramatic increase in those who see it as a competitive advantage marks a major shift in strategic thinking. This shift suggests that as adoption accelerates, digital capabilities are becoming key differentiators rather than mere necessities for survival. (Chart 17)

15. Legacy equipment, lack of skilled employees and organizational culture are biggest smart factory roadblocks

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top 3)

16. Better operational efficiency outpaces all other smart factory benefits

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top 3)

17. Digital transformation still seen as table stakes for majority, but increasing number see it as a competitive advantage

Q: Do you believe that digital transformation of your company’s manufacturing operations will create a unique competitive advantage for your company or is it merely table stakes to remain in the game?

Section 7: The Strategic Value of Digital Transformation

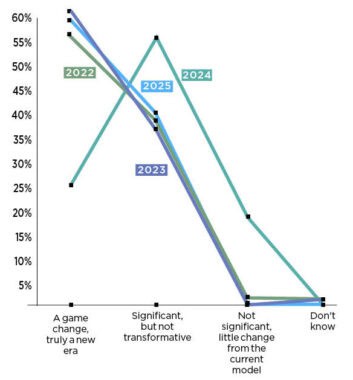

After a dip in enthusiasm in 2024, manufacturers now overwhelmingly see digital transformation as a game-changer—60% believe it signals a new era for the industry, up from just 26% last year. Another 40% still see it as significant but not transformative, while no respondents consider it insignificant. Apart from our 2024 survey, these numbers have remained largely consistent over the past four years. (Chart 18). M

18. After dip in 2024, majority now see digital transformation as a clear game changer

Q: Ultimately, how significant an impact will digital transformation have on the manufacturing industry?

About the author:

Jeff Puma is content director at the NAM’s Manufacturing Leadership Council.