Survey: Smart Factories Enter the Execution Era

Manufacturers push deeper into execution as smart factory strategies mature, AI advances and digital transformation gains as a competitive advantage.

![]()

KEY TAKEAWAYS:

● Smart factories have entered the execution era with manufacturers now wrestling with how to scale digital transformation efforts

● AI is maturing beyond experiment into value-driven, smart factory deployments

● Digital transformation is shifting from table stakes to a game-changing advantage

The Manufacturing Leadership Council’s 2026 Smart Factories and Digital Production Survey shows an industry that has moved beyond experimentation and into a more disciplined phase of execution, integration and operation. Manufacturers are increasingly committed to digital transformation and are now figuring out how to scale it.

While economic optimism and investment intent remain strong, the tone of this year’s survey reflects a more mature mindset. Expectations remain high for AI, automation and end-to-end digitization, but respondents also demonstrate a clearer understanding of the legacy, data and organizational challenges that accompany scale. Compared to 2025’s resurgence of momentum and 2024’s momentary hesitation, 2026 signals a new phase: steady progress, pragmatic confidence and a sharper focus on execution.

SECTION 1: Economic Outlook and Investment Trends

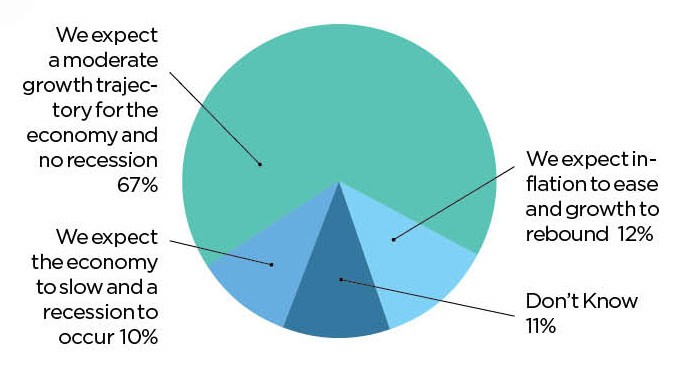

Manufacturers enter 2026 with cautious optimism about the broader economy. A strong majority (67%) expect moderate growth, while only 10% anticipate a significant downturn (Chart 1). These numbers remain similar to the 2025 survey results where 69% expected moderate growth while 8% expected an economic slowdown.

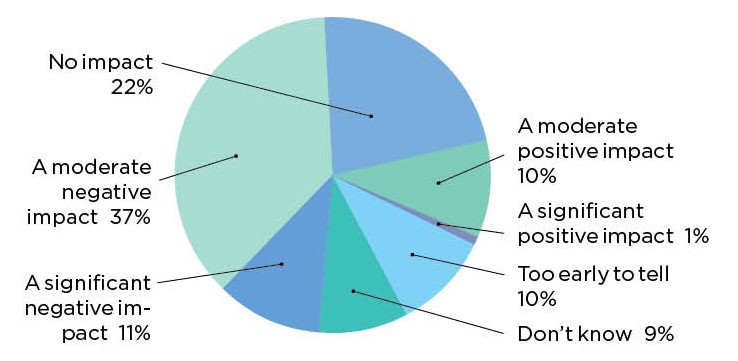

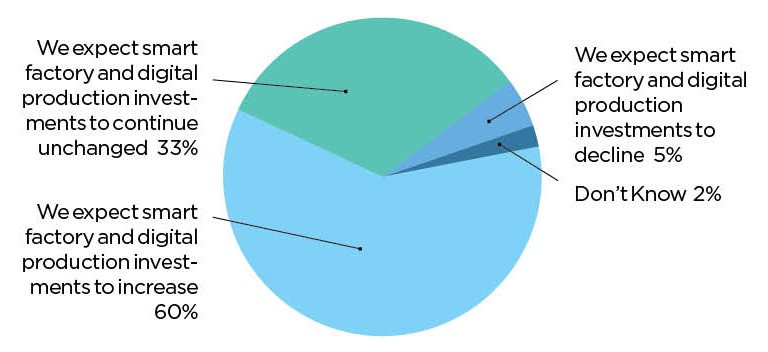

Meanwhile, nearly half of the respondents (48%) say U.S. tariffs are having a moderate or significant impact on their smart factory implementation (Chart 2). While those sentiments are worth watching going forward, the tariff negatives are not enough to undermine Manufacturing 4.0 digital investments. More than 90% of respondents say they expect to maintain or increase smart factory and production technology investments in 2026, with a sizable share planning increases rather than flat spending (Chart 3). The data suggests that digital investment has become embedded in long-term operating plans rather than driven by short-term economic sentiment.

1. Strong majority expect moderate economic growth ahead

Q: What is your company’s outlook for the economy in 2026? (Select one)

2. Nearly half experiencing negative impact from U.S. tariffs

Q: What impact are U.S. tariffs having on your company’s smart factory implementation? (Select one)

3. More than 90% plan to maintain or increase smart factory investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2026? (Select one)

SECTION 2: Smart Factory Maturity and Adoption

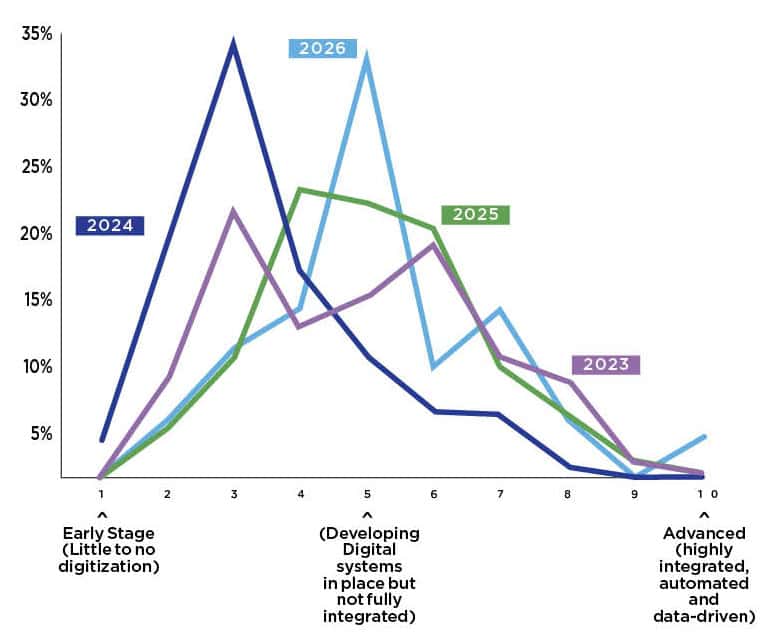

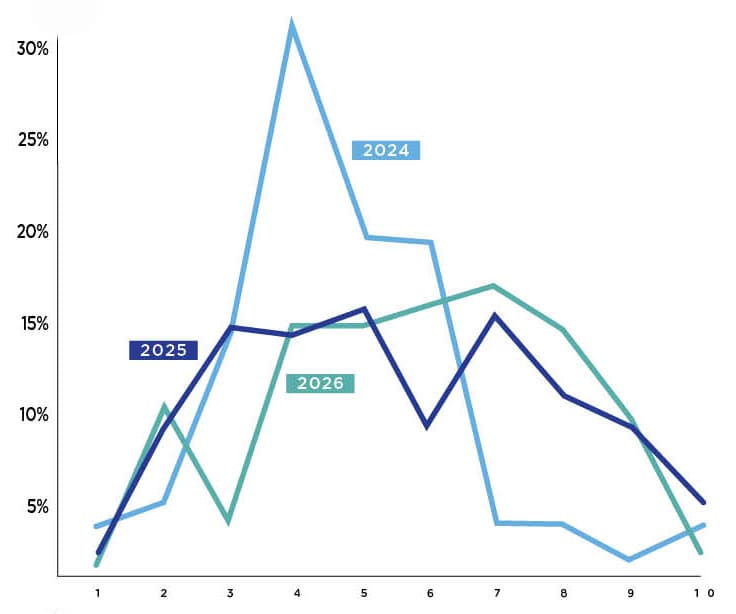

Smart factory maturity is a moving target. When new transformative technologies, like generative AI in 2022 and 2023, find their way into factories, it is natural for manufacturers to reassess how mature they truly are. This is one possible cause for the dip in maturity that our 2024 survey unveiled. As manufacturers have gotten more comfortable with GenAI and other emerging technologies, they’ve been able to find their footing and move forward on the maturity scale, and our survey saw a strong rebound in 2025 that remains consistent in 2026.

The vast majority still place themselves at a mid-level maturity (72% in 2026 vs. 75% in 2025), but our survey shows that those placing themselves firmly at the middle level, or a 5, has hit a high-water mark. This year, more than one-third of respondents say they are at a 5, compared to 22%, 11% and 16%, in 2025, 2024 and 2023, respectively. Growth at the highest maturity levels (8-10) remains incremental—rising from 9% in 2025 to 10% in 2026—reinforcing that advanced smart factories are still the exception rather than the rule. (Chart 4)

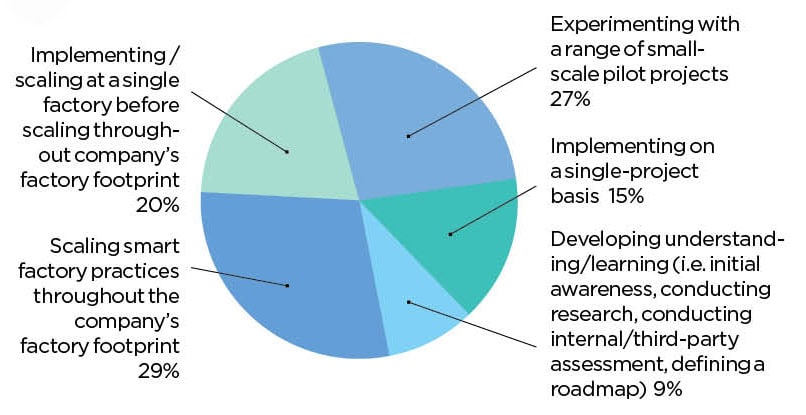

This pattern is echoed in how manufacturers describe their digital activities. Fewer than 10% of respondents report being in the learning stage. Meanwhile, a nearly equal number report that their company is scaling at either a single factory or rolling out initiatives across multiple sites (49%) compared to those in the learning or experimental stages (51%). (Chart 5)

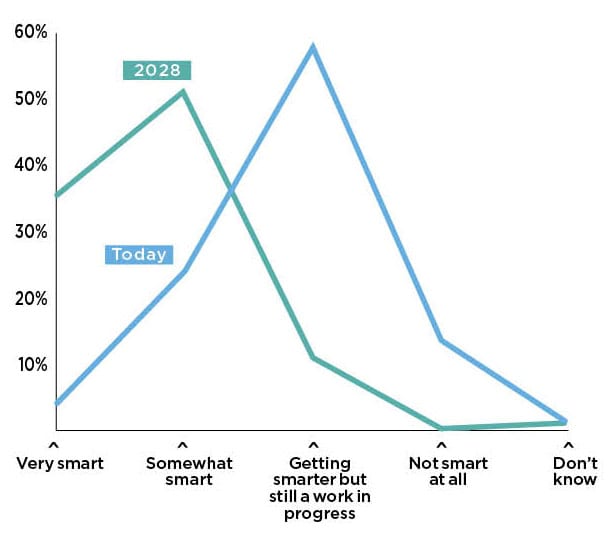

Looking ahead, confidence in future progress remains strong. While only a minority (28%) consider their factories very or somewhat smart today, a substantial majority (88%) expect to reach those levels by 2028. (Chart 6)

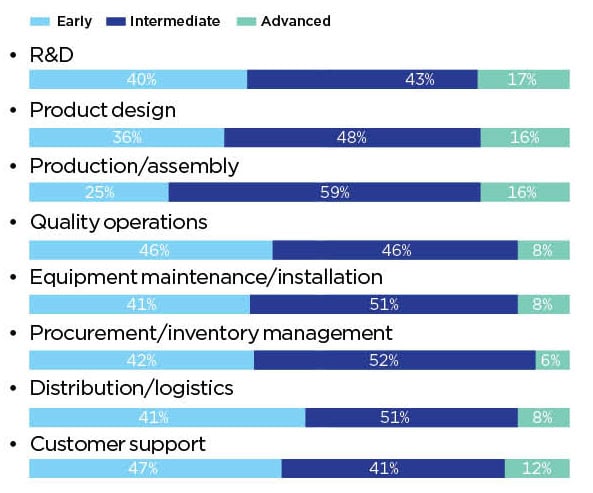

The data suggests that manufacturers believe the foundation is now in place, and they are heading toward the destination. Diving into the digital adoption of specific functions bears this out. It is clear that digital efforts are still a work in progress. Only product design, production/assembly and R&D rise above 15% of respondents reporting that these functions are at an advanced level for their company. The good news is that more than 40% of respondents say they are at least at an intermediate level for every single function we asked about in our survey. (Chart 7)

4. Smart factory maturity continues to advance

Q: How would you assess the maturity level of your smart factory journey? (Scale of 1–10, with 10 being the highest level of digital maturity)

5. Those scaling nearly equal to those in the experimentation and learning stages

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today? (Select one)

6. Manufacturers expect smarter factories ahead

Q: How “smart” do you consider your factory and plant operations to be today, and what do you anticipate they will be by 2028?

7. Advanced digital adoption remains a work in progress across functions

Q: At what stage of digital adoption are the following functions in your company? (Rate as early, intermediate, or advanced)

SECTION 3: Digitization and Automation Growth

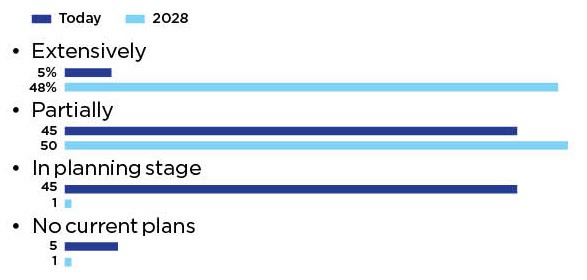

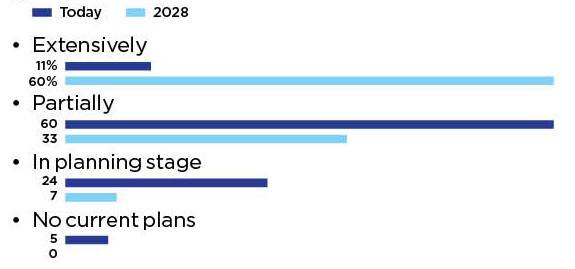

Digitization across factory operations is currently mixed. When considering production, maintenance, quality, planning scheduling and support functions, an equal number of respondents report partial end-to-end digitization or that end-to-end digitization is in the planning stage (45% each). At the extreme ends of the spectrum, 5% say they are extensively digitized or have no plans to digitize. But there are reasons for optimism, with 98% saying that their factory operations will be extensively or partially digitized end-to-end by 2028. (Chart 8)

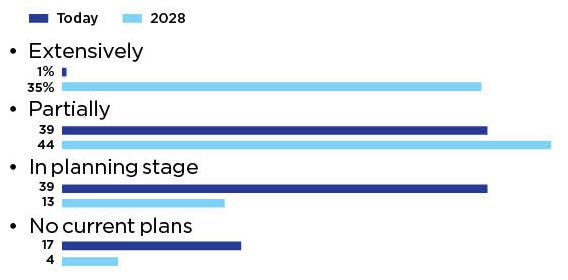

Production and assembly processes remain the focal point of digital efforts today. While extensive digitization is still limited to 11% today, expectations for the future are strikingly high, with most respondents anticipating at least partial digitization by 2028. (Chart 9)

Integration beyond the factory, however, continues to lag. Digital integration with suppliers and customers shows improvement but remains well behind internal digitization efforts. This gap highlights both the complexity of ecosystem integration and a major opportunity for future value creation. (Chart 10)

8. End-to-end factory digitization expected to accelerate

Q: Thinking about your overall factory operations (production, maintenance, quality, planning, scheduling, support functions, etc.), to what extent are they fully digitized end-to-end today, and to what extent do you anticipate they will be by 2028? (Select one for today and one for 2028)?

9. Assembly process digitization on the horizon

Q: Focusing specifically on your core production and assembly processes (activities taking place on the manufacturing line), to what extent are these processes digitized today, and to what extent do you anticipate they will be by 2028? (Select one for today and one for 2028)

10. Customer and supplier digital integration lags behind other functions

Q: To what extent are your production functions digitally integrated with customers and suppliers today, and what do you anticipate they will be by 2028? (Select one for today and one for 2028)

SECTION 4: Future Factory Models and AI-Driven Operations

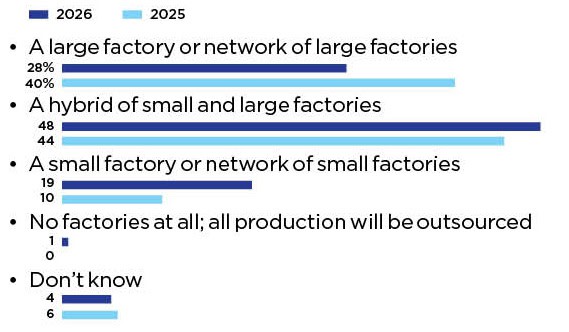

Manufacturers continue to envision a hybrid future for their factory networks. Most expect a mix of large-scale facilities and smaller, more specialized sites, balancing efficiency with flexibility. Compared to 2025, the biggest shifts occurred around the size of the future factory footprint. In 2025, 40% expected their future factory model would be a large factory or network of large factories, compared to just 28% in 2026. Meanwhile, the expectation to have a small factory or network of small factories grew from 10% in 2025 to 19% in 2026. (Chart 11)

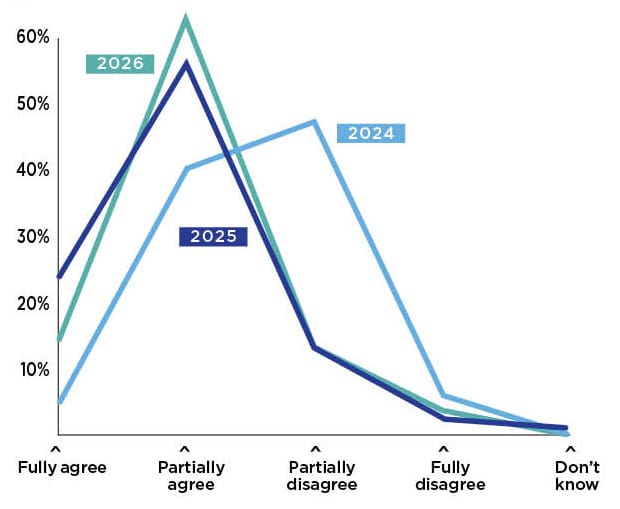

Confidence in AI-driven operations has remained steady. In 2026, 79% of respondents tell us they fully or partially agree that factories will evolve into self-managing, self-learning facilities. This aligns closely with last year’s survey where 80% fully or partially agreed. In both years, it’s important to note that those who partially agree far outweigh those who fully agree. This outlook has increased significantly since 2024, reflecting a more informed outlook that is, perhaps, shaped by leaders’ early experiences with AI technologies. (Chart 12)

11. Hybrid factory model remains dominant future strategy

Q: As you think about your factory footprint in the future, what is the expected future state of your factory model? (Select one)

12. Most partially or fully agree that tomorrow’s factories will be self-managing/learning

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.” (Select one)

SECTION 5: Technology Adoption and Priorities

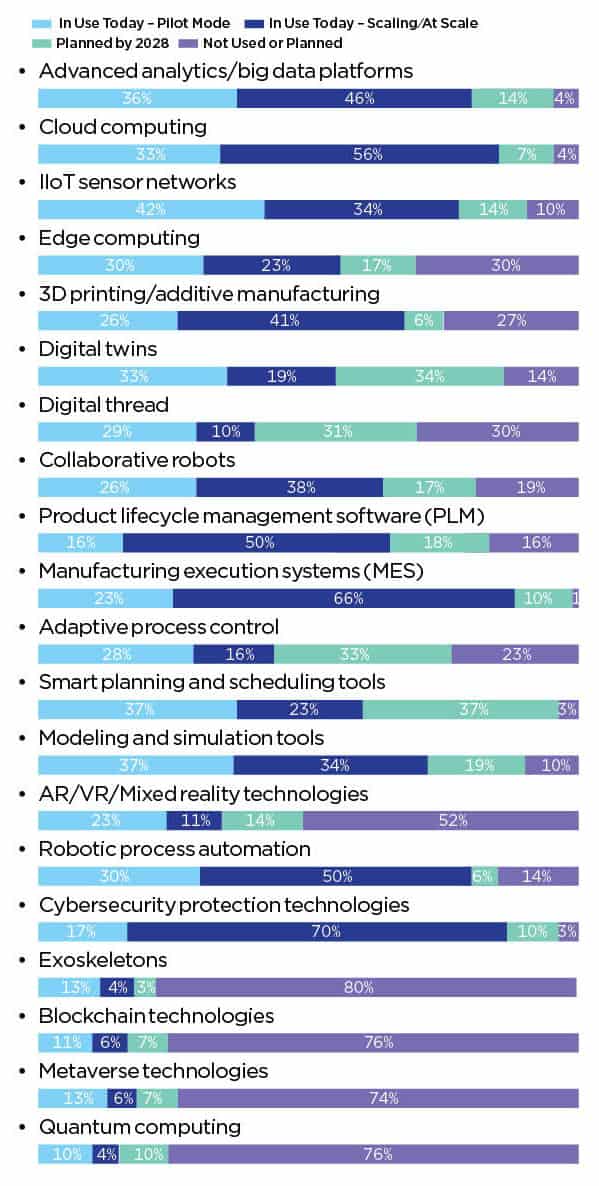

To that end, technology adoption in production operations continues to expand. Cybersecurity, manufacturing execution systems (MES), cloud computing, product lifecycle management software (PLM) and robotic process automation are the highest technologies deployed at scale today. These technologies are increasingly viewed as foundational rather than optional. Looking ahead to 2028, smart planning and scheduling tools, adaptive process control, digital twins, and digital thread are poised to make the largest leap forward. (Chart 13)

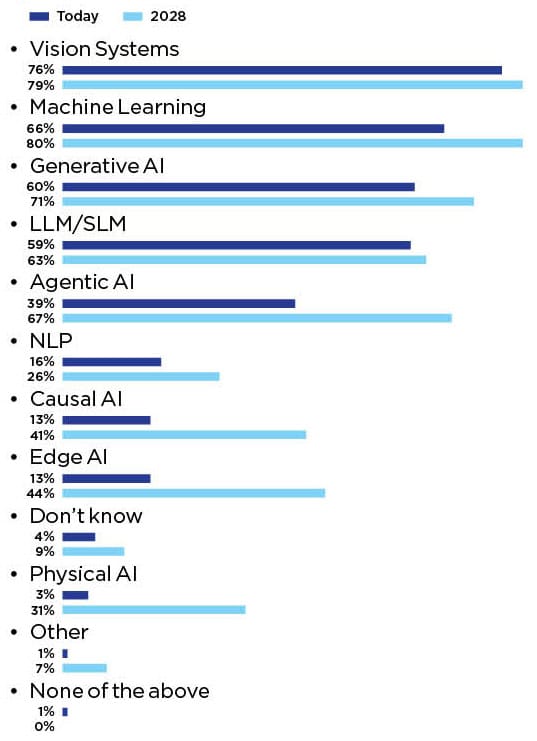

AI adoption is also advancing, with at least two-thirds of manufacturers reporting active deployment of traditional AI tools like vision systems (76%) and machine learning (66%). Across the board, every AI solution we asked about is expected to grow in its usage by 2028. Edge AI, causal AI and physical AI are expected to see the largest increases in use in that timeframe, while machine learning is expected to just surpass vision systems to become the most deployed AI solution. (Chart 14)

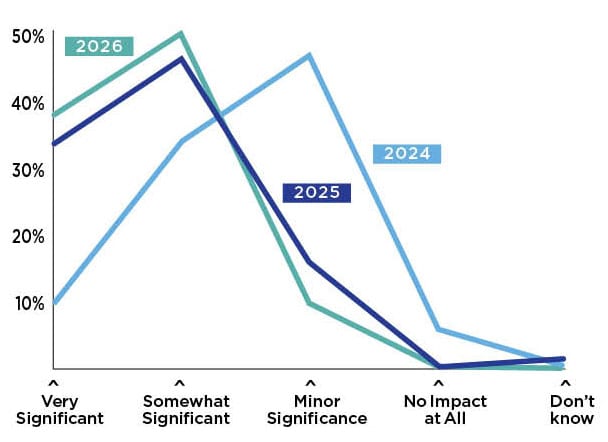

This measured pace is reflected in perceptions of AI’s impact. A growing percentage of respondents describe AI’s future impact on production as very significant (39%), continuing the upward trend from 2025 (34%) and 2024 (10%). (Chart 15)

Together, these findings suggest AI has moved beyond hype, entering a phase of value-driven deployment.

13. Multiple production operation technologies now surpass 50% scaling mark

Q: Where does your company stand in regard to the following technologies in its production operations? (Select one answer per technology)

14. Future growth ahead for every type of AI solution

Q: What types of AI solutions are you using today? (Select all that apply)

15. AI expected to have significant impact on production operations

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations? (Select one)

SECTION 6: Challenges and Benefits of Digital Transformation

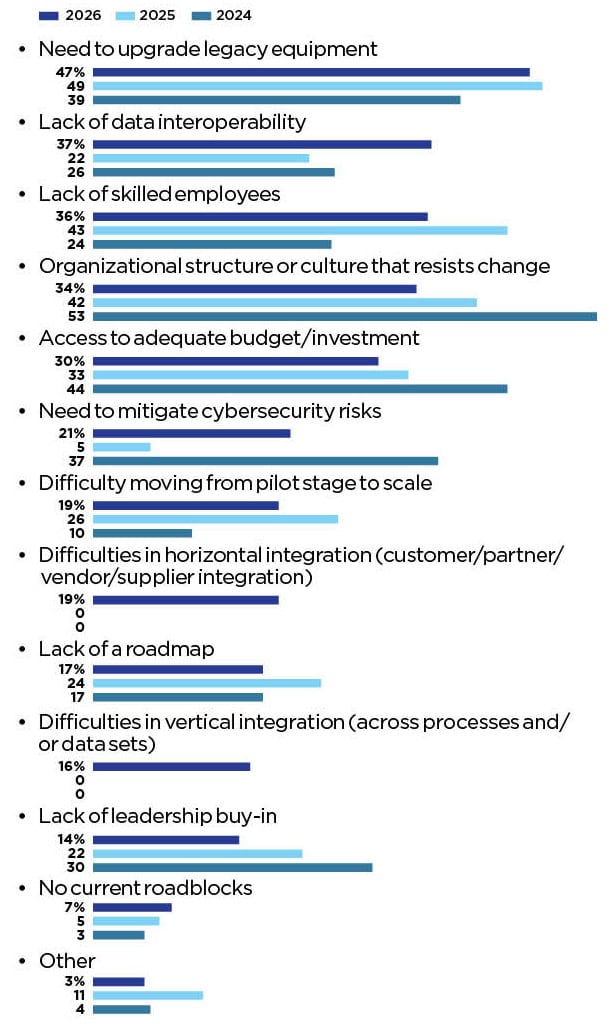

As digital transformation matures, so do the challenges manufacturers face. Legacy equipment remains the most frequently cited obstacle, though this concern has dropped slightly from 2025’s survey. Meanwhile, there has been a sharp increase in those identifying data interoperability as a roadblock to their smart factory strategy. In 2025, only 22% of respondents identified data issues as a primary roadblock, but that has increased to 37% in 2026. Only cybersecurity had a larger increase. In a sign of progress, five roadblocks fell by at least seven percentage points from 2025 to 2026: lack of leadership buy-in, organizational structure or culture that resists change, lack of a roadmap, difficulty moving from pilot to scale, and lack of skilled employees. (Chart 16)

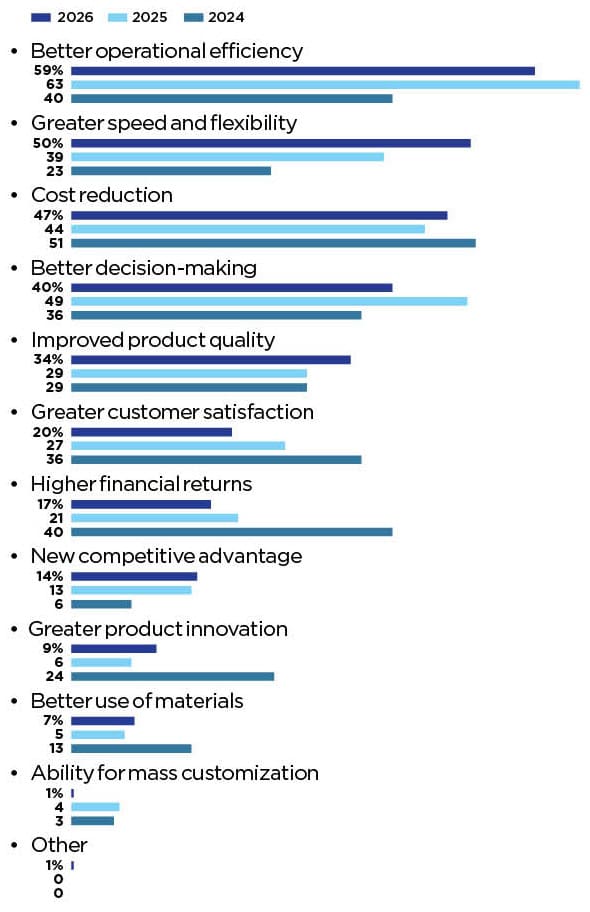

At the same time, perceptions of benefit continue to strengthen. Operational efficiency remains the top expected outcome, with greater speed and flexibility and cost reduction close behind. These results reinforce the growing belief that digital transformation is about more than technological advancement—it delivers measurable business value. (Chart 17)

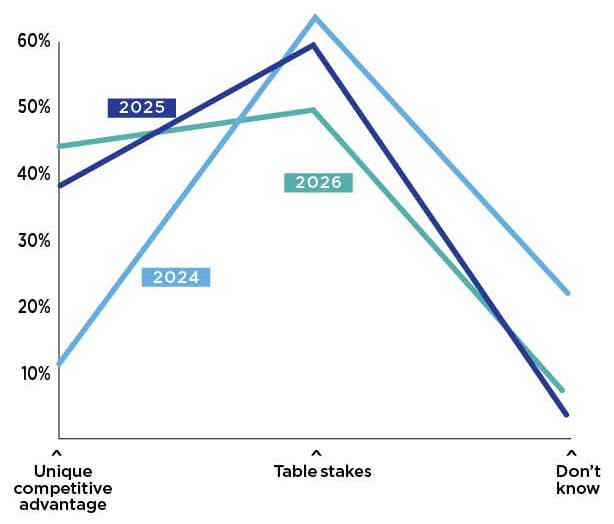

Importantly, while the largest group of manufacturers continue to believe that digital transformation is table stakes to stay in the game, 43% now view digital transformation as a competitive advantage—the highest percentage in the past three years. Because different companies progress on their digital transformation journey at different paces and with different success rates, those who are more successful are seeing a competitive advantage arise. While table stakes still dominate, the momentum is unmistakable. (Chart 18)

16. Legacy equipment, data and workforce are top roadblocks

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top three)

Note: horizontal and vertical integration difficulties were not included on 2025 or 2024 surveys

17. Better operational efficiency remains top benefit of smart factories

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top three)

18. Digital transformation seen as table stakes by nearly half

Q: Do you believe that digital transformation of your company’s manufacturing operations will create a unique competitive advantage for your company or is it merely table stakes to remain in the game?

SECTION 7: The Strategic Value of Digital Transformation

Manufacturers’ views on the strategic importance of digital transformation remain overwhelmingly positive. Perhaps that is why we have seen an increase in those reporting better integration of their smart factory strategy with their company’s overall business strategy. In 2026, 58% say they have passed the midway point (6 or higher) on their integration journey. That is up 11 percentage points from 2025 and a full 30 percentage points from 2024. (Chart 19)

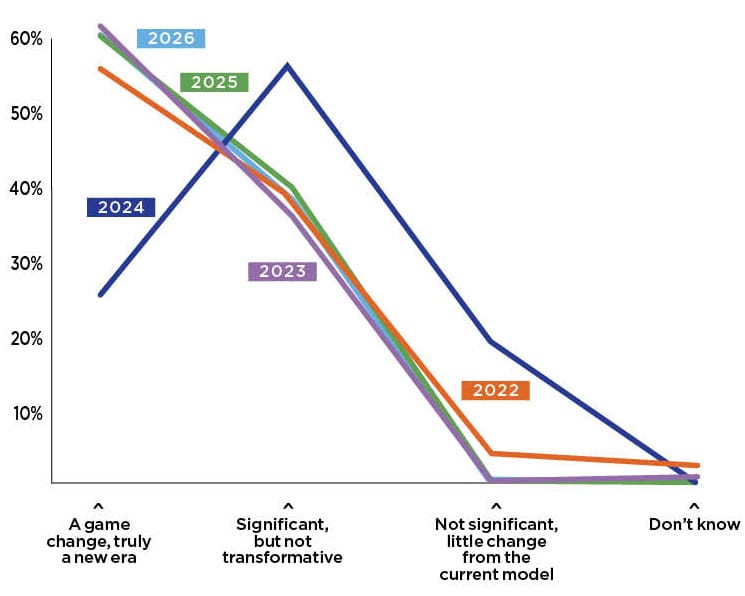

As digital transformation becomes more aligned with overall business strategy, it is not surprising that a clear majority believe digital transformation represents a fundamental shift in the manufacturing industry. Consistent with sentiment seen in 2025 and well above the dip recorded in 2024, 61% of respondents tell us that digital transformation is a game changer, indicating a truly new era for manufacturers. (Chart 20)

19. Smart factory strategy shows stronger alignment with business goals

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy? (Scale of 1–10, where 10 is fully integrated)

20. Optimism around digital transformation impact remains steady

Q: Ultimately, how significant an impact will digital transformation have on the manufacturing industry?

The Bottom Line

What has changed is tone. The 2026 survey reflects less exuberance and more resolve. Digital transformation is shifting from proving its value to delivering on it. As manufacturers move deeper into execution, the 2026 Smart Factories and Digital Production Survey confirms that Manufacturing 4.0 has entered perhaps its most consequential phase yet. The leaders of the next decade will be defined by who executes best on the new technologies available to manufacturers. M

About the author:

Jeff Puma is content director at the NAM’s Manufacturing Leadership Council.