How a Private Equity Approach Can Drive Auto Suppliers’ EV Transition

By adopting a PE lens, companies can transition more smoothly from legacy internal combustion engine business to the EV market.

![]()

TAKEAWAYS:

● The $1.9 trillion global auto supply sector will experience a shakeout in the changeover to EVs, and the slowest movers risk losing opportunities or bankruptcy.

● Companies that have hesitated to initiate change can benefit by assessing future options using the relentless, enterprise-value based approach of private equity firms.

● Lessons from early movers highlight the value of planning the funding, rigorous execution and governance, and workforce transformation.

The global automotive industry is undergoing existential disruption as the world market embraces electric vehicles (EV) over internal combustion vehicles and hybrids. At this point—in the early stages of the transition and with a long way still to go—some challenges facing the diverse auto parts supplier industry are becoming clearer; however, many companies are still figuring out how quickly to embrace those changes.

The market transition to EVs is gaining momentum due to advances in technologies such as batteries and charging stations, and growing buyer interest thanks to the success of Tesla and other electric models. The U.S. and other governments are doubling down on commitments to transition to EVs. Recently proposed federal emissions limits in the U.S. would effectively require two-thirds of cars sold in the country to be electric by 2032; California will require that all new vehicles sold in the state after 2035 be zero-emission vehicles.

Parts suppliers—from gas tanks to fuel injectors—for traditional cars are already seeing their market shrink, and the decline will only worsen. This $1.9 trillion industry will see a painful slowing of growth in coming years as internal combustion engine (ICE)-based product lines are phased out. About one quarter of profits currently generated from legacy ICE components will be the most adversely affected, resulting in a 50 percent decline from current levels by 2030. For some suppliers, the market will eventually resemble a game of musical chairs, with fewer and fewer safe economic places to land—and the slowest movers losing the game.

Segments of the ICE market will remain, such as parts for existing vehicles, and suppliers can continue to earn some revenue in this area long after production of new ICE models is phased out. Also, commercial vehicles have lagged passenger cars in the EV transition, so far, and are likely to offer another “long tail” of continuing opportunity for parts makers.

“About one quarter of profits currently generated from legacy ICE components will be the most adversely affected, resulting in a 50 percent decline from current levels by 2030.”

The impacts are hitting auto suppliers in different ways and at different velocities, depending on the parts they make and the size of the company. For example, many larger makers of powertrains and other ICE components, whose production lines require long development lead times to transition, have embraced the need to change. They are developing transformation strategies and making operational changes, announcing new manufacturing strategies, new partnerships, and new product lines. Public companies also benefit from the involvement of boards of directors and stockholders that push them to adopt transformation strategies earlier while balancing risks.

In contrast, small, medium and privately held companies, with traditional, risk-averse management styles and fewer resources tend to lag. Companies that continue to delay adoption of an operational transition strategy may soon find themselves at risk.

Julie Fream, president and CEO of the Motor & Equipment Manufacturers Association – Original Equipment Suppliers (MEMA), says that one of the biggest challenges companies face is estimating when the growing market for EV products will overtake the ICE components they are replacing. This uncertainty is causing many executives to hesitate as they plan their company’s operational transition from ICE to EV.

“Suppliers know they need to be able to do both, but they are asking, ‘How do I know the volumes?’” Fream says. “How do they manage the crossover point, knowing that you can’t accurately predict at this point where the two lines will cross—where EV becomes dominant, and ICE becomes a secondary product line. That’s the question they are all asking.”

Companies that invest in EV too early could end up financially overextended, with excess capacity and a market that is not ready for their new products. Late arrivals could lose opportunities completely if faster competitors beat them to the punch.

Companies seeking ways to exit ICE businesses also face challenges as certain, carved-out legacy ICE assets will become steadily less attractive to buyers. Without successful consolidation or divestiture, many will be forced to shut down, particularly if cost cuts and efficiency improvements cannot keep pace with commercial declines. At the same time, suppliers wishing to embrace new technologies must invest heavily in new product and service innovations targeted at EVs. Often, these competing priorities absorb cash while also preventing the bold action that is needed in today’s market.

The Private Equity Mindset as Transformation Catalyst

Many auto suppliers, especially those that are small or mid-sized and often privately owned, have relied successfully on a traditional management approach of incremental improvement and risk management. This approach, however, is ill-suited for the current market upheaval. Tomorrow’s winners will innovate and reinvent their whole business, embracing their initial entrepreneurial spirit.

Fortunately, a ready model for bold decision-making exists that can serve as a model for the aggressive approach these companies will require—that of the private equity (PE) investor. Two aspects of the PE mindset stand out as the essential, outside-investor viewpoints that many ICE suppliers urgently need:

- The ability to make bold decisions, without attachment to unprofitable “sacred cows”; and

- A relentless focus on enterprise value.

For companies accustomed to incremental change that need to become unstuck, the PE lens can be a catalyst for the swift cultural makeover needed to get moving.

“The PE mindset is something many suppliers should consider,” says Fream. “There’s a lot of money on the sidelines right now that could eventually come in. This would create some opportunities if you accurately analyze your business and understand what needs to be done.”

“For companies accustomed to incremental change that need to become unstuck, the PE lens can be a catalyst for the swift cultural makeover needed to get moving.”

This is not easy, she notes: “Suppliers need the skill set to assess what’s happening in the marketplace. The PE firm is ultimately trying to drive the company to be more focused on the marketplace. Generally, they don’t tolerate anything outside of that. But this can be very difficult for some suppliers, especially smaller, privately-held companies.”

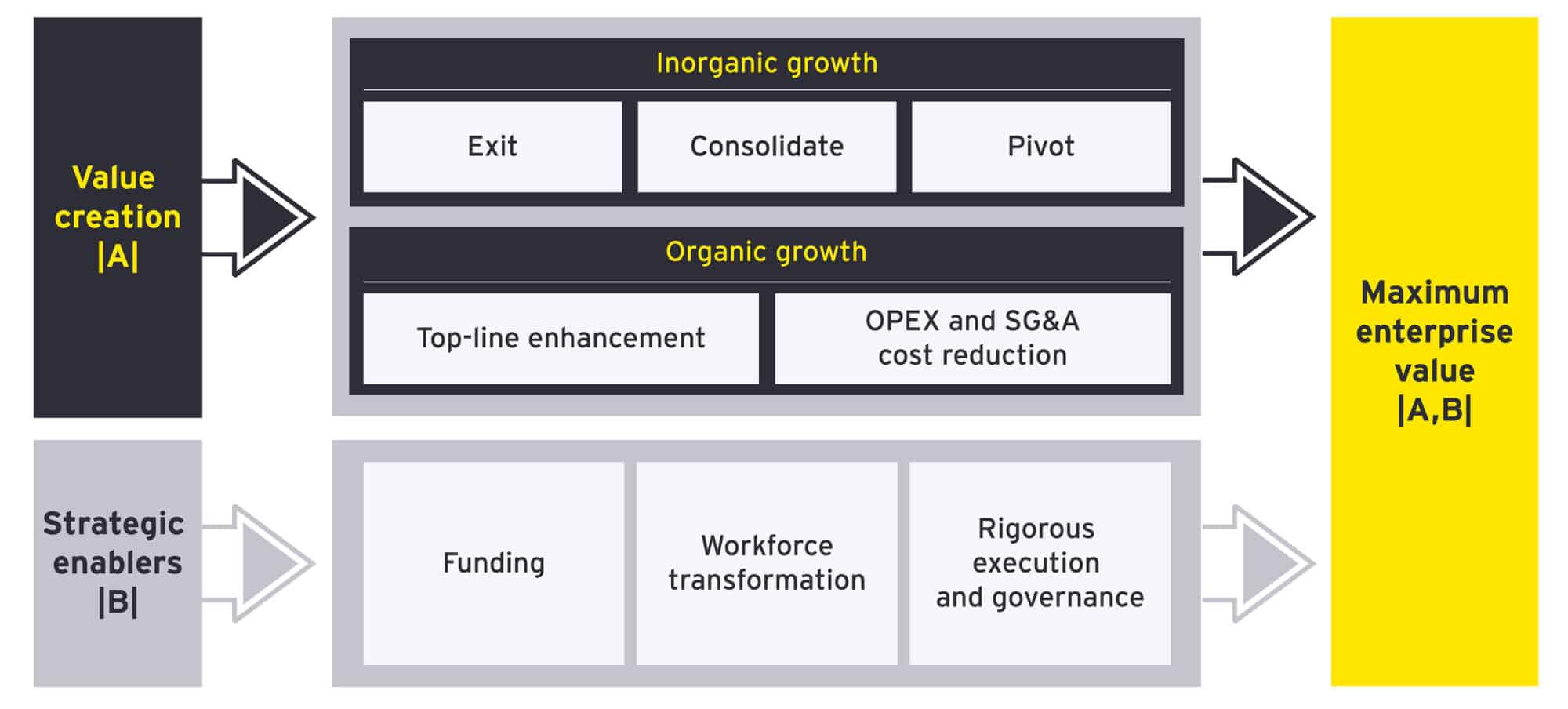

Typically, PE has a variety of strategic approaches to generate profits from companies in either fading industries or startups in new technology fields. PE investors can improve enterprise value and prepare an asset for profitable sale through organic upsides—topline growth and bottom-line improvements—as well as inorganically, through a potential portfolio play (Figure 1).

Figure 1: Private equity value creation approach

Leadership can use the PE agenda to conduct a data-based assessment of how their business creates value today and its potential future role in the developing EV ecosystem. Based on this deeper understanding, leaders can adopt and implement a transformation strategy that aims to maximize enterprise value, as highlighted in the 2022 EY article “How auto suppliers can navigate EV technology disruption in four steps.”

Identify the Appropriate Operational Strategy Using the PE Approach

Not all traditional product components are expected to decline in the near term. Many product lines can be suitable candidates to pivot to other markets, and some can continue as sources for income that can be invested in new EV product development. Strategic approaches for how companies are managing their existing ICE businesses can be grouped in three broad categories:

- Exit (cash out and focus): One clear option is for suppliers to wind down or sell their ICE products businesses to a buyer that can squeeze value from them, for longer, than the original owners can. The spin-off strategy can reduce exposure to the declining demand for ICE products and can raise capital for reinvestment in new market opportunities.

- Consolidate (double down): Suppliers can prepare for the coming shakeout by consolidating existing ICE-only businesses to create synergies and scale so they can continue to derive value from their operations for as long as possible, with the option to continue to operate them alongside new EV businesses.

- Pivot (parallel pursuit): Companies can wind down their ICE businesses according to a clear step-down plan, while pivoting product lines to new EV products. This may require massive investment in R&D, innovation, and digitization to develop new EV products and services. It could include acquiring EV startups or niche players to expand product portfolios and acquire new skills or technologies.

The Transformation Journey So Far: Signs of Success and Warnings

Quite a few original equipment (OE) suppliers have identified enterprise EV transformation strategies and begun to execute them. Based on these OE suppliers’ track records, other suppliers can ascertain the challenges of redesigning value chains or operating models.

Example: A Supplier Divests ICE Divisions and Invests the Proceeds in EV Partnerships

A German powertrain company with ICE and EV products that was spun off in 2021 is following a two-part strategy of divesting its remaining internal combustion divisions to help fund its growing EV business, which is focused on EV innovation and growth through investments and partnerships.

“Companies must take care to minimize the impact on employees. . . . Employees should have the option of transitioning to new business roles, where possible. Companies should develop and activate a clear engagement strategy for unions early in the process.”

The company is selling its catalyst and filters operation and intends to divest its ICE division, which has been profitable since 2021 after years of losses. Meanwhile, it is bolstering its EV business through partnerships with automakers to jointly develop power electronics and electronics companies for access to semiconductors. The company’s electronic mobility business has significant orders from Hyundai and is expected to break even in 2024.

Enablers of Transformation: Risks and Opportunities

Once organizations have determined the strategic way forward, they will face significant challenges in executing the agreed-upon roadmap. The experiences of companies that are already making progress, coupled with recent EY work with automotive supplier clients, can make it easier to identify which strategic enablers companies will need to carry out the transition, as well as useful observations and lessons (Figure 2).

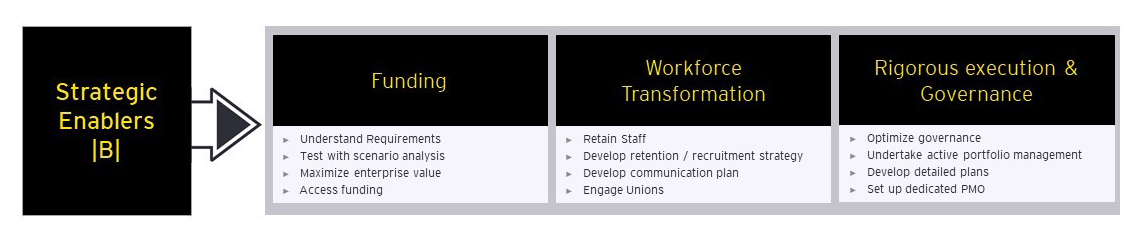

Figure 2: Strategic enablers

Rigorous Execution and Governance

Companies will need to review and adjust their governance so they can manage a rapidly growing, subscale new business and another business in slow decline. Many larger companies are opting to carve out their legacy EV business into a separate division.

Cash flow must be tightly monitored as, given the likely scale of costs, budgeting can be extremely sensitive to small changes in assumptions. Companies should implement robust short- and medium-term forecasting processes during the transition period where cash flow may be tight.

Active portfolio management is equally critical, so that only products with profit potential continue to receive investment. Companies should tier their governance to match the investment and uncertainty levels and to ensure they maintain appropriate controls. They should also take care to avoid excessive reporting and bureaucracy, which can steal oxygen from innovative new ventures.

Workforce Transformation

Staff who will be transferred to new products will need retraining. In cases where companies require new skills that are hard to find within the sector, they can recruit from adjacent industries where employees have transferable skills. In addition, companies will require creative solutions to retain key staff from the legacy business, for as long as is required, to ensure a smooth transition.

Companies must take care to minimize the impact on employees. Open and transparent communication and change management are important, as communication vacuums tend to be swiftly filled with rumors and uncertainty and that can raise stress levels and harm operations. Employees should have the option of transitioning to new business roles, where possible. Companies should develop and activate a clear engagement strategy for unions early in the process.

Funding

Once a company sets its strategy, it needs to fund it, and change can be costly. New products will require expensive capital equipment purchases, and the new business is likely to lose money at first. Companies will need to write down legacy machinery and obsolete stock and take special care to avoid large customer and supplier claims.

Cost control will also be critical during this period, particularly given the long timeframes involved. It is important that companies understand the combined costs of legacy products being ramped down and new products being ramped up. They should do sensitivity analysis to stress-test this requirement, identify budgets, and fund them appropriately. Companies should establish and implement their strategy soon to avoid facing simultaneous closure and setup costs. M

About the authors:

Joern Buss is an EY-Parthenon Partner, Advanced Manufacturing and Mobility, Ernst & Young LLP. Focused on strategic growth, product technology, transformation, and turnaround, he supports manufacturing and mobility companies, alongside private equity and investors.

Jon Slatkin is an EY-Parthenon Partner, Turnaround and Restructuring Strategy, Ernst & Young LLP. He is an Ernst & Young – United Kingdom Strategy and Transactions Partner.

James Nicholson is an EY-Parthenon Partner, Advanced Manufacturing & Mobility, Ernst & Young LLP. He is one of the leaders in the EY UK&I Strategy practice. He helps clients plot successful paths to growth, adopt new business models and evolve their core capabilities and global footprints.

Kevin Rebbereh is Director, Automotive Strategy, EY-Parthenon GmbH. He is a director with EY-Parthenon in Hamburg, Germany and is in the leadership team of the automotive strategy practice in Europe West.

Lloyd McRitchie is EY-Parthenon Partner, Turnaround and Restructuring Strategy, Ernst & Young LLP. He is a partner on the Turnaround and Restructuring Strategy team.