MLC Research

Survey: GenAI Adoption Surges In Manufacturing

Manufacturers are rapidly adopting generative AI, with 71% already using it and nearly 90% planning to expand use in two years. Most have corporate AI policies, though maturity remains early amid data and skills challenges.

Survey: Smart Factories Enter the Execution Era

Manufacturers say smart factories have moved into an execution era, with AI maturing, digital transformation becoming a competitive advantage, and more than 90% planning to maintain or increase investments in 2026.

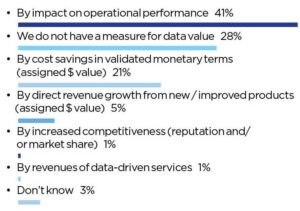

Survey: Manufacturers See Data, Lack Strategy

Manufacturers say data is driving efficiency, cost savings and better decisions, but nearly half lack corporate governance plans and many still struggle to turn data into strategy.

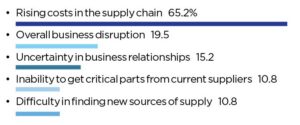

Survey: Tariff Tumult Roils Supply Chains

More than 40% of manufacturers say tariffs are already hurting supply chains, with rising costs the biggest impact. Most are turning to digital tools, analytics and resiliency efforts to boost visibility and reduce disruption.

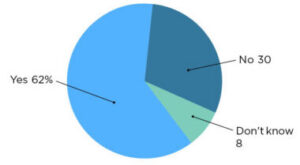

Survey: M4.0 Appears Poised for A Significant Leap

Manufacturers are boosting AI and smart factory investments as digital transformation gains momentum. Most expect economic growth, and 75% now rate their digital maturity at a mid-level.

Survey: Leadership Preparedness Improves, but Gaps Remain

Digital manufacturing leaders are improving change management and restructuring for M4.0, but most still lack formal training and feel unprepared for future digital demands.

Survey: Manufacturers See AI as a “Game-Changer” as They Ramp Up Investments

Manufacturers are rapidly increasing AI investment, with 78% planning higher spending and nearly half already using generative AI tools. Despite early-stage adoption and workforce/data challenges, 55% expect AI to transform the industry by 2030.

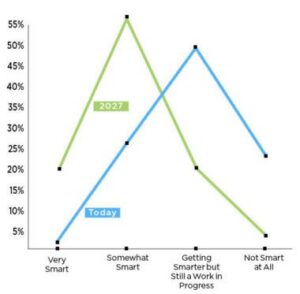

Survey: Smart Factories Are Still a Work in Progress

Manufacturers are steadily investing in smart factories, but most remain at an intermediate stage of M4.0 adoption. Cultural resistance and organizational change remain the biggest obstacles.

SURVEY: Manufacturers Go All-In on AI

MLC survey shows manufacturers are rapidly adopting AI, with 40% using it widely or in pilots and most expecting it to have the biggest future impact. Companies also say AI is driving process improvement, predictive maintenance, and broader supply chain use.

The Industrial Metaverse May Be Closer Than You Think

Manufacturers are increasingly investing in the industrial metaverse, with most executives expecting it to transform R&D, design, and operations within five years. Key challenges include cybersecurity, data protection, and talent retention.