Practical AI Steps to Build Smarter Factories in 2026

AI is enabling factories to respond faster to customer demand, adapt to disruption, and operate more profitably.

![]()

TAKEAWAYS:

● Modernize smart factories via digitization; choose technologies based on business outcomes and validate data availability before designing AI solutions.

● Prioritize use cases for business impact, short time‑to‑value, and data availability; target 60–90 day pilots that can scale.

● Embed AI into human operational workflows and governance so intelligence drives actions while people retain accountability and judgment.

In manufacturing across the globe, a consistent theme emerged in 2025: volatility is now an operating condition. Geopolitical friction, supply disruptions, regulatory shifts, and rising customer expectations have combined to make speed, resilience, and real‑time visibility essential. Manufacturers best prepared to absorb disruption had unified data, process automation, and operational transparency, while those hampered by fragmented systems and manual workarounds struggled to respond effectively. While modern factories often conjure up images of physical automation such as robotics and automated lines, digital automation is equally important, with AI taking center stage.

This year, the conversation has shifted from AI experimentation to embedding intelligence and resilience into daily operations and integrating coordinated capabilities into core workflows. Agentic AI is one of the most consequential developments. These systems go beyond providing insights and recommendations by autonomously planning, deciding, and taking actions to achieve a goal.

Principles to Help Pilots Scale

Three practical principles separate pilots that scale from those that stall: business outcome before technology; prioritize for impact, speed, and data; and industrialize with humans in the loop.

1. Business outcome before technology

Successful projects begin with a measurable business problem, such as boosting first‑time service fixes, shortening order‑to‑cash, reducing obsolete inventory, or lowering energy consumption. Define the key performance indicator (KPI) first, then assess whether you have the data required to solve it. If the data isn’t available or trusted, the immediate focus should be data readiness: integration, master‑data remediation, and governance.

Real-life example: A materials‑handling original equipment manufacturer (OEM) used historical service records to predict likely faults on forklifts and provisioned the correct spare parts for field engineers. The result was an approximately 30% increase in first‑time fixes, directly improving margins and customer service through a rapid pilot.

2. Prioritize for impact, speed, and data

Manufacturing is target‑rich for AI. Prioritize use cases using a simple triage:

- Impact: Will solving this issume significantly improve something important to the business—margin, throughput, quality, lead time, or customer service?

- Time‑to‑value: Can a meaningful pilot be delivered within 60–90 days?

- Data: Do you have the data needed to support AI and automation? Prioritize use cases where data readiness exists, even if imperfect, over those requiring time to build a data repository.

Small, fast wins build momentum and confidence.

Real-life example: A mid‑market equipment manufacturer still receives many of its orders via PDF email. Capturing these with optical character recognition (OCR), validating inventory with simple rules, and auto‑confirming when possible produced immediate ROI and relieved customer service teams hours of repetitive work. Adoption was high because it added true value and removed tedious steps.

3. Industrialize with humans in the loop

While we’re moving toward more agentic capabilities, full autonomy entails a long journey to build trust. Frame AI as a “digital co-worker,” reducing cognitive load, surfacing prioritized actions, and allowing people to make final decisions in safety‑critical or high‑risk contexts. Human oversight shortens the trust curve, improves training data, and preserves accountability.

Foundations matter, so integrate before you automate. AI can only scale on a solid digital foundation and only be effective when it has context within the business processes it is acting on. Organizations that invested in integrated platforms connecting machines, logistics, planning, and service are able to activate AI more quickly. Removing data silos turns visibility into recommended actions: predictive inventory shortfalls trigger auto‑replenishment, plans adapt in real time, and exceptions are addressed before they cascade.

A recommended sequence might be: process mining to diagnose variability and bottlenecks first; automate repetitive steps with robotic process automation (RPA); and finally, apply AI for pattern recognition and optimization.

Real-life example: One contract steel manufacturer used process mining to reveal hundreds of return‑handling variations. Process redesign plus automation subsequently delivered measurable improvements in cycle time and cost.

Manufacturers need a pragmatic rollout playbook:

- Diagnose with low‑friction visibility tools (process mining, transaction audits).

- Automate routine, documented tasks first, before adding predictive layers.

- Prioritize AI use cases that can deliver results in 60–90 days with impactful KPIs.

- Keep the human in the loop to build confidence and trust.

- Measure business KPIs and iterate.

2026 is about realizing AI value, not by chasing novelty, but by industrializing proven approaches on solid digital foundations. Start with the business problem, move quickly on high‑value, short‑cycle pilots, keep people at the center, and treat agentic capabilities as workflow amplifiers. That’s how factories become smarter, more adaptive, and more profitable in measurable time.

To learn about how Infor Velocity Suite helps customers achieve sustained business value and more customer use cases, click here. M

About the author:

Andrew Kinder is Senior Vice President Industry Principal for Manufacturing at Infor.

Can AI Agents Catalyze Faster, Smarter Product Design?

AI agents grant product designers faster data access and decision support to reduce rework and enable smarter, more efficient product development.

![]()

TAKEAWAYS:

● AI agents speed product development by automating routine tasks and surfacing cross-system insights, helping teams avoid errors and make more optimized decisions.

● AI agents elevate human judgement rather than replacing it by surfacing relevant options and historical insights for designers to evaluate.

● Organizations that focus on targeted reuse scenarios, strong governance and clear KPIs will be best positioned to capture measurable impact from AI agents.

Manufacturers face a familiar but intensifying challenge: competitive pressure demands greater speed, lower cost and continuous innovation—yet product design cycles aren’t keeping pace. Compounding this, every product iteration now generates exponentially more data, and instead of streamlining decisions, that complexity too often creates more noise than clarity. AI is changing that—not by replacing engineering judgment, but by giving teams the tools to move faster and decide smarter.

The real opportunity for decision enhancement lies not in any single system, but in the connections across all of them. Manufacturers already sit on vast reservoirs of institutional knowledge—embedded in product lifecycle management (PLM) systems, enterprise resource planning (ERP) data, quality records, supplier histories and engineering documentation accumulated over decades. The problem is that this knowledge has historically lived in silos, forcing engineers and product teams to make critical decisions with only a fraction of the relevant context. When AI can surface patterns and relationships across these enterprise systems simultaneously, the nature of the decision itself changes—teams stop reacting to incomplete information and start anticipating outcomes before they occur.

This is where AI agents are beginning to redefine what’s possible in product development. Unlike traditional search or analytics tools, agents can traverse both structured data and unstructured content—think engineering specifications, change orders, inspection reports and supplier emails—inferring connections and similarities that no individual engineer could reasonably track across a complex product portfolio. In practice, this means teams can identify potential quality issues before they propagate, assess manufacturability earlier in the design cycle when changes are least costly, and automate time-consuming but critical tasks like compiling regulatory documentation. The result is less time spent hunting for answers and more time spent acting on them.

AI Agents for Connecting Data to Better Decisions

AI agents are not simply better search tools; they fundamentally change how designers leverage enterprise knowledge and make decisions. They can surface relevant prior designs and approved components, predict quality risks, highlight manufacturability constraints, summarize regulatory requirements and automate routine data compilation.

A few high‑value use cases illustrate the potential:

- Finding previously approved formulations or components that match new design requirements

- Surfacing similar products or variants to accelerate early design concepts

- Predicting quality or manufacturability risks based on historical patterns and design attributes

- Summarizing regulatory requirements and automating administrative, repetitive or retrieval-heavy portions of the design process

- Synthesizing cross-system insights to support faster, more informed design decisions

By reducing time spent navigating systems and reconstructing prior decisions, AI agents shift engineering effort from information retrieval to design evaluation. Rework declines as teams confidently build on proven designs and previous guidance. With faster access to the insights they need, designers are free to explore faster, more broadly, and with more context. As the final judges on design decisions, humans remain in the driver’s seat.

Evolving the Product Development Ecosystem with AI Agents

AI agents don’t replace existing systems or enterprise architecture—they complement PLM, ERP, quality management systems (QMS) and other repositories by connecting information and uncovering insights. Most companies are only beginning to experiment with AI in design workflows. Understanding the path from early pilots to full AI adoption can help companies capture value faster while mitigating risk.

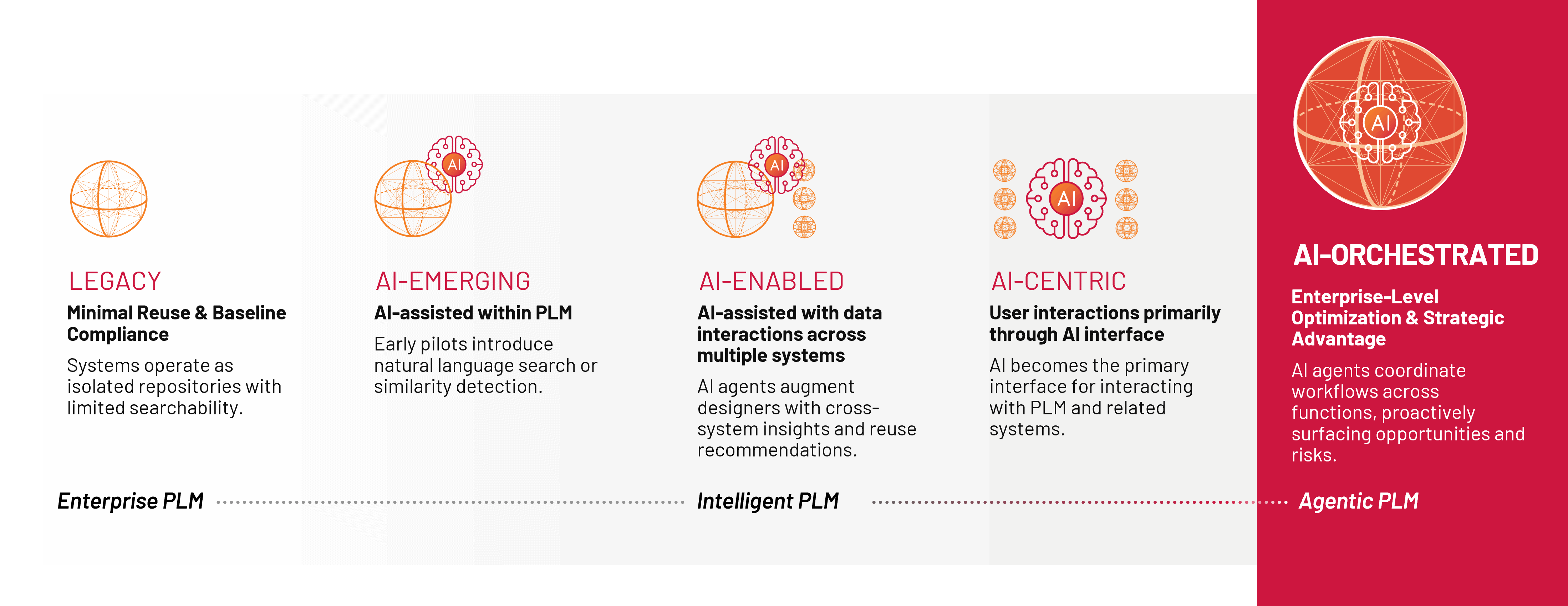

This shift to an AI-assisted design workflow represents a new evolution in PLM maturity:

Figure 1: A new PLM Maturity Model

Advancement along this model hinges on both technological and cultural preparedness. Teams must trust the data, understand how AI agents derive conclusions, and provide proper oversight. Transparency and traceability are crucial, especially in regulated sectors. Progressive organizations will view AI agents as collaborative tools that augment human ability, rather than substitute it.

How Manufacturers Can Start the Journey

The most successful manufacturers will follow these steps:

- Diagnose pain points and process inefficiencies

Identify where mistakes are made, where reinvention or repetition is prolific or where you stand the most to gain from more optimized decisions. Define the personas impacted and map information needs from across the enterprise, not just PLM – ERP, MES, QMS, and RIM systems. - Match the right AI capabilities to the right problems

Different challenges require different tools:

a. Generative AI for summarization, interpretation and chat interaction

b. Predictive models to catch errors and forecast the outcome of a decision

c. Prescriptive models to optimize design, such as for cost or manufacturability

d. Retrieval-augmented generation (RAG) for intelligent search across document stores and databases

The goal is not broad AI adoption but targeted solutions that reduce cycle time and rework. - Build a prioritized use case pipeline

Start with narrow, high-value scenarios to demonstrate measurable improvements in speed or rates of reuse. Use early wins as momentum to refine the operating model. - Establish the operating model early

AI agents require continuous improvement, not a one-time implementation. Leaders should build an AI-ready PLM architecture that accounts for governance, data structures and a federated model connecting central AI teams with product design functions. This ensures that AI agents remain accurate, trusted and aligned with business needs.

Future-Looking Product Designers Have AI Assistants

AI agents will not replace product designers—they will amplify their expertise and creativity. But capturing this value requires discipline and cultural readiness; many organizations fall into the trap of “doing AI” without clarity on business value or underestimating the complexity of PLM and adjacent systems. Clear KPIs, strong governance and a focus on real problems—reuse, visibility, cycle time—keep teams grounded in outcomes rather than hype.

Equally important, leaders must help culture evolve alongside new technologies. Job loss fears and uncertainty can slow adoption unless teams understand that AI agents relieve administrative burden rather than eliminate design roles. When designers see AI as a partner that expands their creative capacity, adoption accelerates.

The future of product development belongs to teams that treat AI agents as true collaborators—tools that help them move faster, design smarter and innovate with confidence. M

About the Authors:

Chelsea Barnes is a Data Science Director at Rockwell Automation Digital

David Miracle is Global Lead Principal of Consumer Packaged Goods at Rockwell Automation

The Data-Ready Factory Starts With Trust

Manufacturing executives who master data governance and interoperability will define the competitive landscape of the next industrial decade.

![]()

TAKEAWAYS:

● Manufacturers that treat data governance as a strategic capability to gain measurable advantages in operational agility, forecast accuracy, and capital allocation.

● Interoperability is the prerequisite for autonomous decision-making, and organizations that cannot bridge their data silos see diminished returns on AI investments.

● Data mastery starts with shared definitions and ownership, aligning people, processes, and architecture before selecting any platform or technology.

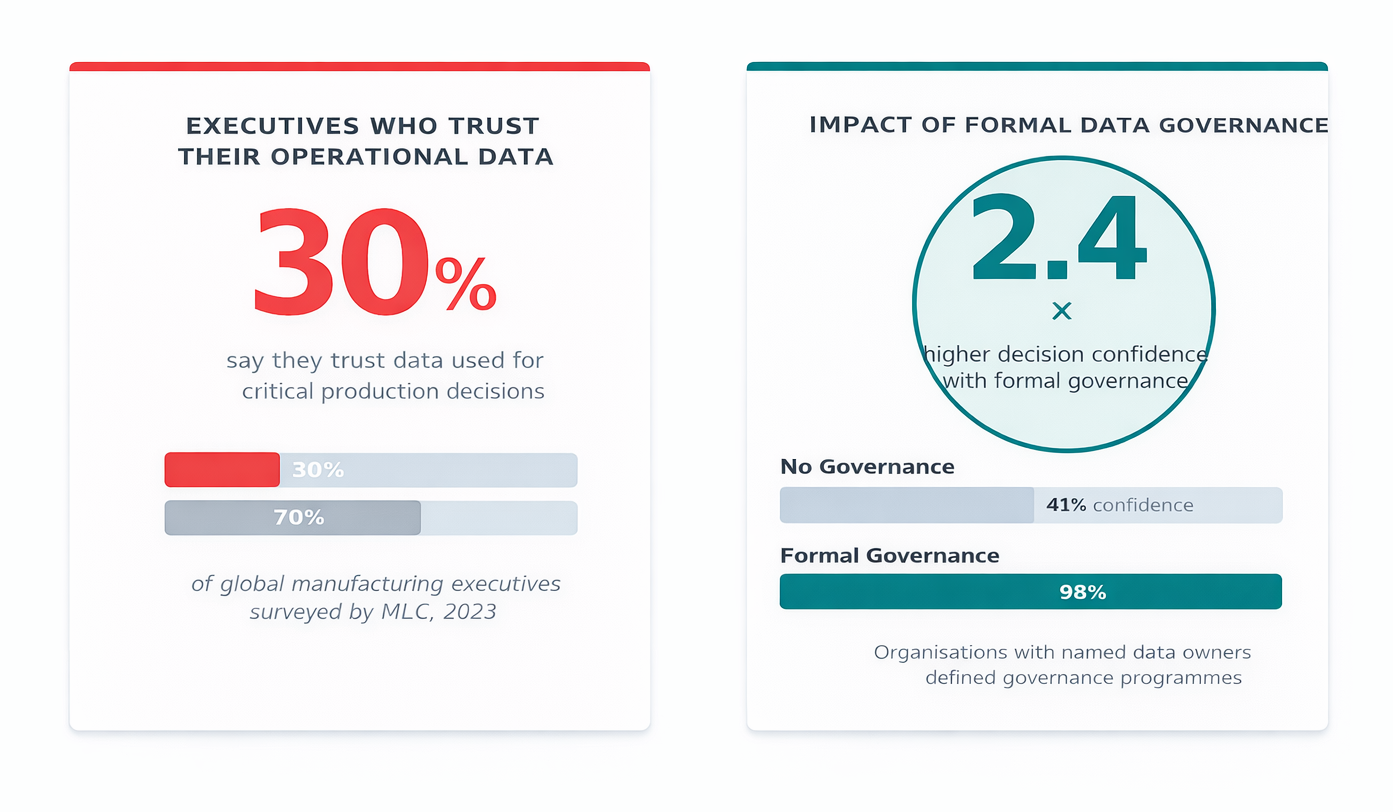

There is a paradox at the heart of modern manufacturing. Factories today generate more data than at any point in industrial history. Terabytes of sensor readings, production events, quality flags, supply signals, and energy metrics flow continuously through operations that would have been unimaginable a generation ago. Yet, when executives are asked whether they trust the data they use to make decisions, fewer than a third express confidence.

This gap between data volume and data confidence is not a technology problem; it is a governance problem. Closing it has become one of the most consequential leadership challenges of the decade.

Why Data Trust Has Become the Central Issue

The ambitions of Manufacturing 4.0/5.0, autonomous scheduling, predictive quality, and AI-driven supply chain optimization, all rest on a single premise: that the data underpinning those algorithms is accurate, timely, and consistent across the enterprise. When it is not, the consequences are not merely inefficient, they are actively misleading.

A 2023 study by the Manufacturing Leadership Council (MLC) found that data quality and integration ranked among the top three barriers to advanced analytics adoption across a global panel of manufacturing executives. The same research—available in the MLC’s State of Smart Manufacturing Report—noted that organizations with formal data governance structures reported 2.4 times higher confidence in their production decisions than those without.

This matters because the cost of bad data in manufacturing is not abstract. For example, when a scheduling algorithm relies on yield data that has not been reconciled across shifts, the resulting plans will appear optimal on paper but fail on the floor. Similarly, when procurement models ingest supplier lead times from multiple systems that define “confirmed order” differently, inventory buffers expand and working capital erodes. The downstream effects of these upstream data ambiguities compound silently until they surface as a missed quarterly target.

Figure 1: Data Trust and Governance Maturity in Global Manufacturing Operations

The Data Confidence Gap share of manufacturing executives who trust data used for operational decisions vs. those who have formal governance structures in place. Source: Manufacturing Leadership Council, 2023.

The Three Dimensions of Data Mastery

Data mastery in manufacturing is not a destination; it is an operating discipline built across three interconnected dimensions: governance, quality, and interoperability. Each is necessary, yet none is sufficient alone.

Governance establishes the rules of the road: who owns which data, what it means, how it is measured, and who is accountable when it is wrong. Without governance, even the most sophisticated data infrastructure becomes an expensive source of competing truths. The critical insight for manufacturing executives is that governance is fundamentally an organizational design challenge, not a software configuration. It requires naming data owners—not merely nominal data stewards—but senior leaders who bear consequences when the numbers are unreliable.

Data governance is not a technology initiative. It is a leadership decision about who owns the truth.

Quality is governance in motion. It means building operational processes that catch errors at the source—at the machine, at the shift handover, at the supplier portal—rather than attempting to clean data downstream after it has already influenced decisions. Leading manufacturers are embedding data quality metrics directly into operational performance scorecards, treating a data error rate the same way they treat a defect rate: as something that carries an owner, a target, and an escalation path.

Interoperability is the architectural expression of governance and quality. It is the capacity of data to flow accurately and meaningfully across systems—from production execution to enterprise planning, from plant to boardroom—without losing fidelity or requiring manual translation. This is where most organizations are furthest behind, and where the consequences of inaction are becoming most acute.

The Interoperability Imperative

The average large manufacturer operates with dozens of disconnected systems across its production and supply chain footprint, including programmable logic controllers (PLCs), supervisory control and data acquisition (SCADA) systems, manufacturing execution systems (MES), enterprise resource planning (ERP) systems, and increasingly, cloud-based analytics environments. These systems were implemented at different times, by different teams, and with different data models, resulting in an architecture that cannot support the decision velocity that competitive manufacturing now demands.

Consider what autonomous production optimization actually requires. A system that can recommend a schedule adjustment in response to an upstream supply disruption needs to simultaneously read inventory positions from ERP, current work-in-progress status from MES, equipment availability from maintenance systems, and energy pricing signals from utility feeds. This information must be contextualized and available with sufficient confidence to act without human validation. This is not a challenge any single system can solve; it is an interoperability challenge.

Data mastery in manufacturing is not a destination; it is an operating discipline built across three interconnected dimensions: governance, quality, and interoperability.”

The emergence of open standards, including ISA-95, OPC-UA, and the IDTA Asset Administration Shell, has created a more navigable path toward semantic interoperability than existed five years ago. But standards adoption alone does not solve the problem. It creates the conditions under which the problem can be solved—if the governance foundations are already in place.

Organizations that have made meaningful progress on interoperability share a common characteristic: they started with alignment on what data means before they invested in infrastructure to move it. They built shared data dictionaries. They mapped the lineage of key operational metrics—where a number originates, how it is transformed, and where it lands—and they resolved definitional conflicts at each step before connecting systems.

Framework for the Path Forward

For manufacturing leaders assessing their data readiness, the following framework offers a practical starting point:

- Audit the definitional layer first. Before discussing platforms, map the 10 to 15 most critical operational metrics—overall equipment effectiveness (OOE), yield, schedule adherence, and lead time—and determine whether they are defined consistently across every system and site that uses them. Most organizations find they are not.

- Assign data ownership at the executive level. Every critical data domain should have a named owner—not an IT team, but an operational leader whose performance is affected by the reliability of that data. This single structural change has more impact on data quality than any tooling investment.

- Treat integration as infrastructure, not as a project. Organizations that achieve durable data flow do so by adopting architectural patterns—data fabric, unified namespace, or semantic layer approaches—that decouple data sharing from individual system upgrades.

- Measure data health as an operational key performance indicator (KPI). Data quality metrics—completeness, accuracy, timeliness, and consistency—should appear on operational dashboards alongside throughput and quality. What gets measured gets managed.

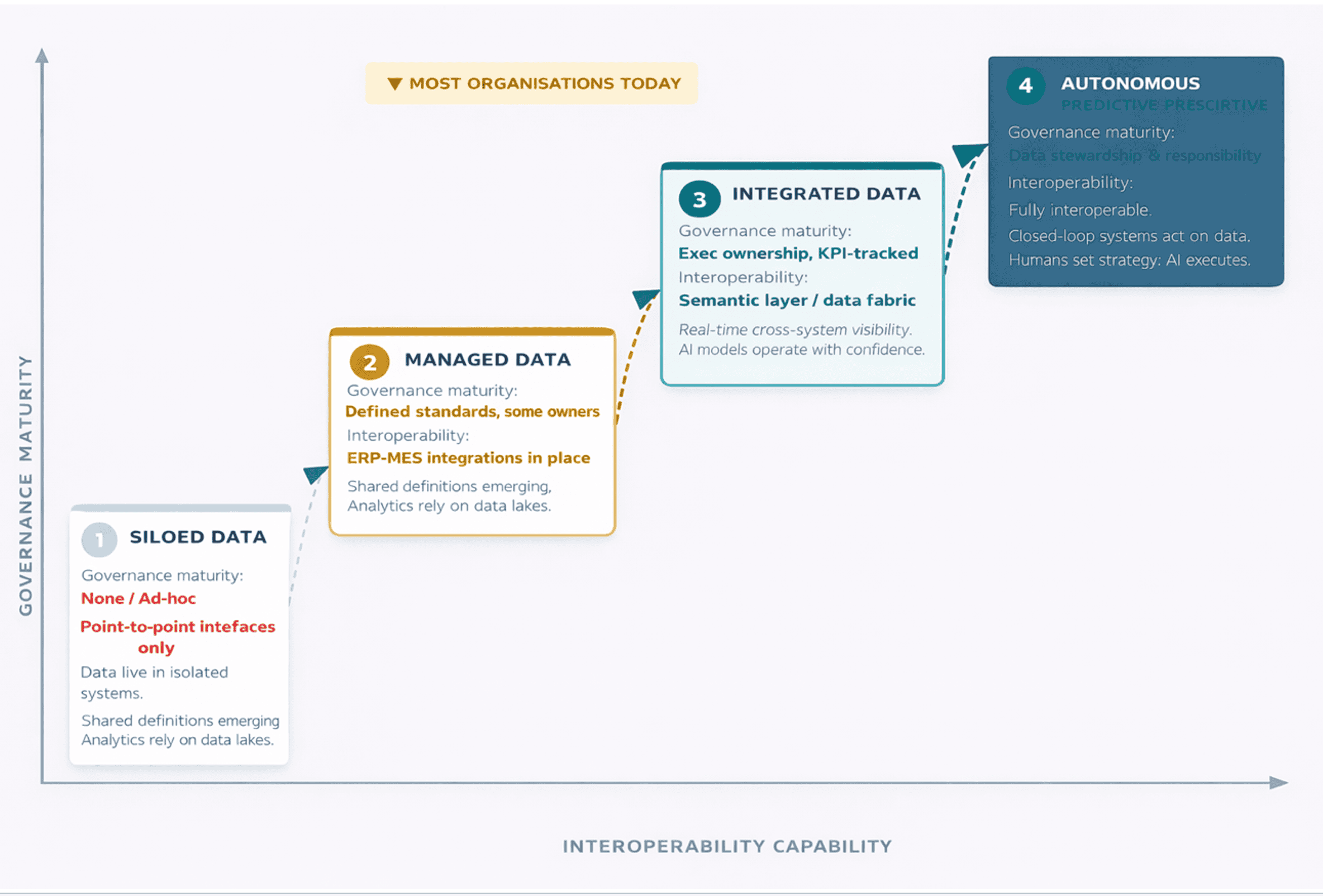

Figure 2: Industrial Data Maturity: From Siloed to Autonomous

The Data Mastery Maturity Model four stages from siloed data to autonomous decision intelligence, mapped against governance maturity and interoperability capability. Source: Original illustration

The Leadership Imperative

Data governance is not a program that manufacturing IT departments can manage in isolation. The organizations making the most progress are those where the chief operating officer, or an equivalent executive, has placed data quality on the same agenda as safety, quality, and delivery, treating it not as a technology initiative, but as an operational discipline with corresponding accountability structures.

The logic is straightforward. If the purpose of a Manufacturing 4.0 investment is to improve decision-making to enable better planning, faster responses to disruption, and more precise capital deployment—then the quality of the data informing those decisions is not a mere technical detail. It is the foundation. Every advanced algorithm is only as reliable as the data it consumes.

“Data governance is not a program that manufacturing IT departments can manage in isolation.”

The manufacturers who will define the competitive landscape of the next decade are not necessarily those with the most sophisticated AI or the most connected factories. Rather, they are those who have built the discipline of data trust deeply into their operations, ensuring that applied intelligence amplifies human judgment instead of distorting it.

The factory of the future runs on data, but it runs well only when that data is governed, mastered, and shared with integrity. M

About the author:

Prashanth Mysore is Global Strategic Business Development Senior Director at Dassault Systèmes.

Sources:

— 2023 State of Smart Manufacturing Report — Manufacturing Leadership Council

— ISA-95 Enterprise-Control System Integration Standard — ISA

— Asset Administration Shell Specification — IDTA

Dialogue: Leading Manufacturing Through AI Change

Rockwell’s Blake Moret on urgency, AI adoption, policy shifts and why manufacturers must become learning organizations

![]()

David Brousell (DB): I’m David Brousell, the founder of the Manufacturing Leadership Council, the digital transformation arm of the National Association of Manufacturers.

I’m here with Blake Moret, the chairman and CEO of Rockwell Automation.

Congratulations, Blake, on becoming chair of the NAM this year. From your position as chair of the NAM as well as CEO of Rockwell, what is your sense of the state of the industry at this point in time? And where do you see digital transformation in manufacturing and smart manufacturing?

Blake Morret (BM): To begin with, the importance of manufacturing has never been more widely recognized by, governments around the world, but in no place, more urgently than in the U.S. And I think that’s a very good thing. I think that manufacturing is at the core of the American economy.

The magic multiplier of jobs outside of just direct manufacturing, is often underestimated. And so the recognition by the government, by, you know, our population, is very encouraging to see that.

How do you increase the manufacturing in the U.S.? I think it’s going to be important to recognize that in a place with relatively high labor costs, to be competitive with other strong companies around the world, you have to include the technology with that. So smart manufacturing, advanced manufacturing techniques are going to be really important. And of course, artificial intelligence is a part of that as well. And policy that creates a conducive environment is going to be really important as well.

The NAM is in an amazingly important place because, on the other end, there’s a lot of uncertainty where tariffs are going, where regulations are going to lead us? And the NAM, with its understanding of these issues and the aggregate power of the thousands and thousands of members, has an opportunity to really make a difference.

DB: If we all work together.

BM: Yeah

DB: If we all orchestrate together all those things you just talked about.

Why Smart Manufacturing is Accelerating

DB: Let’s drill a little bit into smart manufacturing.

One of the main conclusions of your 10th annual state of manufacturing or smart manufacturing report was that, due to global risks, including tariffs, supply chain disruptions, the industry seems intent on accelerating its adoption of smart manufacturing.

Yet we know that many manufacturers, deal with a lot of challenges about adopting smart manufacturing, whether it’s the legacy systems, the cost, budget constraints, understanding how to deploy new technologies, etc.

What pace do you think the industry is poised to move at this point in order to accelerate their adoption of smart manufacturing? And do you think we can get past just incremental improvements? Is there something you see, perhaps, on the horizon that could enable us to make a leap?

BM: I think there is a heightened sense of urgency about moving faster and complementing continuous improvement, incremental improvements, which remains very important.

People are still needed. The idea is to give them superpowers with some of the new technologies.

It has to be a part of the culture, but also being willing to compare all the other options that are out there, other competitors who have found different ways to do things, different internal techniques that can change the game, so to speak.

I think of, you know, the importance in our own culture of being willing to compare ourselves against all the other choices that a stakeholder has, whether it’s a customer, an employee, an investor, to increase the speed of decision making, which is especially important in a, you know, long standing company like, like Rockwell.

And then making sure you have a steady stream of new ideas from both the lifers in the organization, as well as, people with new perspective.

DB: The right ten incremental improvements could add up to a leap.

BM: When we look at our productivity, when we look at the way that we slice our engineering and development budgets, it’s going to be a mix of incremental improvements, fixing things, adding new functionality that’s important to a specific customer, but it’s also about the big leaps as well.

In our own roadmaps, adding more software, infusing artificial intelligence, in some cases needing to create products and software from the ground up to be able to have modern code bases, to be able to expand still further into the future. And sometimes incremental approaches just aren’t enough.

But I think there is that sense of urgency. Tariffs have increased the need for speed, so to speak. Being able to move around your manufacturing footprint, to be able to add resilience into your operations, the agility that’s required for that. And sustainability is still important and being the best steward of water, air, gas, electricity and steam, because in the end, that’s a measure of efficiency.

DB: That’s a lot of balls to juggle.

BM: It’s a lot of balls to juggle and to prioritize and to weave it into something cohesive.

Leadership in a Time of Constant Change

BM: And that’s an important point in that, just like the technologies we’re talking about that move from automation to autonomy using artificial intelligence to help machinery actually learn how to be more performant, organizations have to be learning organizations.

The things that I thought were going to be priorities when I moved into this job have changed quite a bit over the time. And, you have to be comfortable with that pace of change.

DB: You have to be comfortable with being uncomfortable.

BM: Yeah, there is a certain amount of that.

The Future of Industrial Operations

DB: Let’s dive a little bit into the future you just mentioned. You’ve been talking about and Rockwell’s been talking about the future of industrial operations. And in your articulation of that future, you have talked about what you call intelligent autonomous systems. What’s the extent of autonomy that you envision coming into the industry? Do you think the manufacturing companies are going to be embracing a fully lights out model? Do you see a more of a hybrid coming in where certain functions will be completely autonomous, but others that have more criticality will not be?

BM: I get asked this a few times, as you can imagine.

DB: Yeah.

BM: I think it’s still a human-centric view of the future of automation in factories. People are still needed. The idea is to give them superpowers with some of the new technologies. But there are going to be very few truly light-out factories.

People are still needed. But to be freed up from repetitive physical labor—moving a heavy thing from one place to another—I think those are some of the opportunities that are ahead for us. Particularly in higher labor cost countries like the U.S., being able to take an engaged and enabled workforce, people who are trained to do a good job and want to do a good job because they like the organization that they’re working for, and they like the work they’re doing, complemented by the technology. That’s really the winning hand.

And we see that, across multiple industries. Some industries have had more technology in them. They’re further along in that journey. Others are really at the at the front end of that. But it’s the ability to make improvements to meet those companies and those industries where they are to bring it in, to be able to pay a lot of attention to the change management that’s required so that operators recognize that this can create more meaningful work—it’s not just being used blindly to reduce headcount. For managers to understand how the technology can be best used and to have a thoughtful plan.

Rockwell’s in the automation and the efficiency business, but I fully expect we’ll have more people at the end of 2026 than we enter 2026 with, because we’re going to be more competitive as we use this technology, and we’ll be able to do more of the things that we’re already doing, will be able to enter into new lines of business—and that all requires people.

From Artificial to Augmented Intelligence

DB: Perhaps we should call it augmented intelligence.

BM: I think it’s a good way to frame it because, again, that concept of human-centric automation and an approach to this is really important to keep in mind. A lot of the benefits of AI are going to be simplifying technology that remains very advanced, but to bring it together in a way that you can interact with it, that people can interact in the technology with natural language, for instance, rather than having to know the arcane programing languages that were developed half a century ago.

And I think those are really exciting opportunities for advancement in the whole interaction between people, operators, technicians and the technology itself.

DB: We can’t have one of these conversations without talking a lot about AI. It’s so present in our lives now.

You’ll have to spend more time than you think on change management.

We did a big report that we released in May called Shaping the AI-Powered Factory of the Future. And one of the key findings in that study was that 68% of the respondents said they believe that AI will be essential to their competitiveness and growth as we head toward 2030. I think that’s quite a statement. And to me, it meant that a lot of companies are looking at this to propel themselves forward. There’s a bandwagon effect happening. As all these companies start to get their toes and their feet and their ankles and their legs into AI, where do you think they’re going to get the most value from AI? And what do you think the competitive differentiators are going to be for companies as we all embrace AI and it becomes kind of like a high school diploma.

BM: At a high level, across multiple industries, the importance to add additional resilience and agility and sustainability to your operations are really going to be important.

Having people who are comfortable with the tools, who also know the workflows in their individual areas of responsibility—whether it’s in a certain business unit, your coding, your applications, it’s in back office functions, human resources, things like that, in marketing—it’s going to be applying artificial intelligence to workflows to simplify them, to give them more impact in the organization.

What I don’t want, as our people become more literate with AI, is to just go out on fishing trips, you know, to see what turns up. I want them to first identify what are problems that have been vexing their particular areas for a long time, and how can we apply a toolset which includes AI to identify that and then to bring it, in our case, with multiple centers of excellence, to be able to then decide, okay, what’s the best tools, either things that we ourselves have created or what’s already out there in the open market, and to try to standardize as much as possible. But to be able to work with folks who have the pattern recognition to say, “Okay, you’re trying to do this. We’ve done something very similar over here,” so that we can do it in a common way.

But there is an accountability. How is this going to show up?

In the organization, you know, there’s a certain amount of productivity that I expect already this year to come from AI. And going forward, it will be a mix of the quick hits, so to speak, and the moonshots that are going to completely change some of the ways that we do things. For customers, it’s applying AI at all levels of the technology stack, from vision AI to mobile robots to scheduling software that includes AI and then bringing it together into a coordinated, highly orchestrated system.

DB: I almost thought you were going to say the word architecture, how important this is going to be with AI.

BM: Yeah, I think it is. I mean, we talk about the three underpinning areas of technology—and I’m talking about in factories today—is a software-defined automation architecture, it’s the use of artificial intelligence, and then it’s robotics.

DB: At MLC we call AI a “pervasive technology,” and we mean it in a couple of ways. One is what you mentioned that AI was going to find itself into every system, on the factory floor at the EBS level, at the ERP level, at the PLM level, CRM level, everywhere. At the same time, it touches every piece of what the NAM does.

How Policy Can Enable AI

DB: There’s kind of an important question about what steps can policymakers take to create a supportive framework for manufacturing and AI that drives innovation, efficiency and all the things we as an industry need to advance? How do we do that at a policy level?

BM: Let me step back a minute. Before talking specifically about AI, let’s talk about the environment that has to be created for durable and persistent support of manufacturing, in general.

The first important step with getting some certainty around tax, statutory tax rate, incentives for new investments with the One Big, Beautiful Bill, I think that’s really important and giving that level of certainty has been an absolute positive.

In any change, explaining the “why” is really important.

The work on permitting reform and streamlining regulations, I think those are important areas. Additional certainty with respect to tariffs, of course. And then, the final one and maybe most important long term is workforce—being able to provide purpose-built education that doesn’t require necessarily a four-year degree or even a two-year degree, to be able to be really effective.

And that bridges to the specific question about artificial intelligence, in that the workforce, the education, helping companies understand how to set up a functioning infrastructure and governance to make sure that as new ideas are created, you have knowledgeable people who can translate that into action, who, again, can draw from the tool sets that are appropriate for their enterprise to be able to make it reality, but also to have the governance to make sure that safety, you know, privacy, all the things that you know, are brought up as potential risks are looked after and including the disruption of certain roles are changed through the increased use of AI. How do you make sure that that doesn’t destroy the culture of a company? Because all of us know that that culture is really, really important.

DB: Change management takes on a new dimension, doesn’t it?

BM: You’ll have to spend more time than you think on change management.

DB: And cyber will be a key piece of this too.

BM: That’s absolutely right, because the bad guys are using AI as well.

DB: Yeah. Any tool could be used for good or bad, right?

BM: Right.

Reducing Complexity in an AI World

DB: You continue to emphasize that manufacturers should continue to emphasize reducing complexity. We’re building layers and layers and layers of IT and OT technology in our companies, and now the wave of AI is going to come in as well. That takes an incredible amount of orchestration, architecture, real hard thinking about how you’re going to do this as a company.

How do manufacturers deal with all those requirements and yet reduce complexity at the same time when it seems like inexorably things are getting more complex?

BM: Well, first of all, it takes a commitment to that and to really devote that effort and the right expertise to develop that thoughtful approach.

And I think it then requires the convening of stakeholders, whether it’s your machinery suppliers, your subject matter experts who are on the plant floor who know, what happens and what can go wrong and what contributes to the best output, bringing them all together. Sometimes it requires, you know, a handful of trusted consultants as well to come together and look at a specific problem and how we can apply these things to create the best outcome.

Again, don’t go at it with a fishing trip with a bunch of tools and to look at what shows up. It’s better to go say, “Here’s a specific problem that I have in a location, and let’s put the right team together so that it’s endorsed with the people who have to keep it running and are responsible for the production.”

DB: Yeah, let me kind of bubble a little bit. Don’t worry about a strategy right away. Get some experience, do some experimentation.

BM: Yeah. Play yourself into shape to some extent.

DB: Yeah I like that.

BM: But that simplification is really, really important because then you’re not as dependent on individual heroics to keep it running.

DB: Yeah that’s quite a challenge.

Leadership Through Change Fatigue

DB: We have a lot of challenges in an industry we’re facing, but it’s so exciting too. I find this whole thing with AI so exciting—what’s going to happen to the industry in the next 10 or 15 years.

Which kind of takes us back to the question about leadership, because leadership, we’ve always felt, is the key to digital transformation.

It’s not the technology, it’s leadership. It’s changing the organization to take advantage of the technology. It’s changing the culture. And all those “soft issues,” so to speak.

Going back to the Rockwell report, the Rockwell report says that effectively managing people and resources and dealing with resistance to change are some of the biggest issues facing manufacturing companies.

And it’s not slowing down, and it’s led to what the report called “change fatigue.” How can manufacturers overcome these challenges and keep their teams motivated, sustain momentum? Is it just a question of stamina, or is there some technique to it too?

BM: In any change, explaining the “why” is really important. To be sure, we’ve had a lot of externally generated challenges and requirements for change. Recently it’s been things like, the COVID pandemic. It’s been supply chain shortages. Overstock in certain industries. Tariffs. And so there have been a lot of things that we didn’t ask for necessarily, but that have come in. But then we see other aspects requiring change like the adoption of artificial intelligence in a thoughtful way.

So explaining the why and making sure that you’re doing that early and often, and leadership really understands the why and takes the time throughout the organization, not just at the highest level, because a lot of times where this falls down is kind of at that middle layer, you know, the manager/director level, do they really understand or are they are they a part of the formulation of the plan for how these things are going to be implemented?

You can’t just be doing [AI] as a labor of love. It’s got to be done for impact.

And so taking more time than you think you need to, usually turns out to be very, well spent time. To instantiate that and then to frequently check in because there’s always going to be a course correction. You’re not going to get it 100% right ahead of the implementation and so being able to course correct so that you keep those key stakeholders on board.

I mean, those are some general things with it. I think in the specific case of artificial intelligence, having a certain amount of expertise is really important. We made an acquisition of a company called Kalypso a few years back, and it brought in a tremendous amount of data scientists. It was further augmented by an acquisition of a company called Knowledge Lens after that because we needed to kind of jumpstart that internal capability. And we had people who understood these concepts, but we weren’t going to be able to scale as quickly as we needed to. And so as we are now entering a phase where these things are being deployed more broadly, we’ve got the right talent base in our own operations as well as what we’re talking to customers about.

Organizing Around the AI Opportunity

DB: That’s a great privilege to be able to bring in that talent at that scale.

BM: Yeah.

DB: And probably a lot of companies that can’t do that, particularly the small and medium sized manufacturers, it could be more of a challenge. But what you’ve been talking about has provoked in my mind a question about I often ask myself about AI and manufacturing companies, and it comes down to how best to organize around the opportunity. How should we do that? You know, do we appoint a team? Do the manufacturing companies need a chief AI officer? Do they need their HR departments, as you’re talking about, to have a specific campaign for AI talent? How best to organize around the opportunity?

BM: Everybody’s approaching it in a little different ways, but where we’ve seen certain measure of success is you do have some centralized centers of excellence, if you will. We have a center of excellence that’s concerned primarily with the use of AI in what we offer to customers based on the business that we’re in, hardware, software, and so on. And then we have within our IT organization, a clearinghouse for people looking to use business systems internally to be able to maximize, you know, the use of AI for efficiency.

But within each of the functions and businesses, we require a certain amount of internal expertise because these are the people who really understand the workflows particular to that area, whether it’s human resources or marketing, finance and so they’re expected to work together. We have a very large community of practice of people from both kind of the centralized and distributed areas of expertise. And they get together regularly to share best practices, to talk. It’s allowed us to move at pace.

And then back to my earlier comment about ownership. It’s got to show up in our productivity targets. It’s got to show up in terms of market share gains in terms of the products that we’re offering.

So you can’t just be doing this as a labor of love. It’s got to be done for impact.

DB: If they haven’t already, Wall Street will recognize it and build it into their valuations.

BM: Yeah.

DB: Right?

BM: Well, they’ll see it because it’ll show up in greater growth as well as profitability.

DB: Yeah that’s the end game for sure.

Approaching the Future

DB: Looking forward into the next five years, ten years, etc., what advice would you offer manufacturing operational leaders as they try to embrace a future that’s characterized by AI and autonomy, which many could feel is disruptive?

BM: I think you have to learn enough about it to understand what the potential is as well as, what you have to manage in terms of potential adverse impact.

But most succinctly, you have to be a learning organization.

DB: Yeah

BM: You have to be a learning organization.

DB: Yeah. Continuous learning.

BM: That’s right.

DB: Well, thank you very much. A most interesting conversation, I’m sure we’re going to do it again soon in the next year or so and we’ll see what has changed. And hopefully the industry makes some progress.

BM: Absolutely. It’s been a pleasure, David.

DB: Yeah. Thank you.

BM: Thank you. M

About the Author:

David R. Brousell is founder, vice president and executive director of the Manufacturing Leadership Council

Future-Proofing Business Amid Workforce Change

As experienced workers exit the industry, manufacturers must embed product and commercial expertise into scalable, digital processes.

TAKEAWAYS:

● The loss of experienced manufacturing talent creates a hidden commercial risk that impacts sales efficiency, accuracy and growth.

● Manufacturers can reduce dependency on tribal knowledge by embedding product and pricing expertise into standardized digital processes.

● Guided, system-driven selling approaches help both sellers and buyers navigate complexity as workforce demographics continue to shift.

Manufacturers are undergoing a pivotal workforce shift.

By 2030, 1 in 6 people in the world will be aged 60 years or over, according to the World Health Organization. In the U.S. alone, 10,000 people turn 65 each day. As the workforce ages and industry turnover continues, skilled labor and institutional knowledge are lost across technical roles, especially engineering.

While manufacturers have focused heavily on resilient production and supply chains, there’s an equally critical challenge: commercial and delivery processes still rely on the deep expertise of experienced engineering and product teams. As seasoned technical talent, including engineering and product specialists, retire or transition out of the workforce, manufacturers face knowledge gaps that slow product rollout, increase engineering interruptions, and limit the organization’s ability to scale consistently.

Addressing this challenge means codifying technical and product expertise into scalable, digital processes and rethinking how complex products move from design intent to commercial execution without increasing engineering workload. Manufacturers are navigating a major workforce transition at a time when innovation, customer expectations, and market pressures demand greater productivity to remain competitive.

The Workforce Shift Puts Profitability at Risk

Even as labor markets stabilize, manufacturers continue to struggle with workforce challenges. A survey of over 200 global manufacturers found that 30 percent of companies expect 16 percent or more of their sales and engineering talent to retire in the next five years. Only 32 percent are digitizing internal knowledge—the majority are simply rehiring or mentoring. But failing to capture and easily transfer knowledge across the business is a performance risk.

This can have an impact on both sales and engineering teams. A knowledge gap often results in:

- Slower onboarding and longer time to productivity for new hires

- More errors and costly rework in proposed solutions

- Hours lost waiting for technical validation

- Customers disengaging due to slow and inconsistent quoting processes

Lack of knowledge transfer can cost large businesses millions of dollars per year due to wasted time and missed opportunities.

Competitors that can scale and systematize knowledge are better positioned to capture opportunities with more agility. At the same time, buyer expectations are shifting. Today’s customers want conversations focused less on technical minutiae and more on how solutions support their broader business objectives.

Redefining How Manufacturers Sell Complex Products

For manufacturers with vast product portfolios and highly configurable products, sales has traditionally required deep technical expertise and heavy reliance on engineering for every configuration. This model is nearly impossible to sustain in the speed of today’s market.

New hires take longer to ramp up, engineering teams can get bogged down in creating imperfect solutions, and expecting every salesperson to be a technical expert slows the sales cycle.

By redefining how products are sold, manufacturers can shift from a knowledge-dependent model to one that emphasizes solution building. This shift includes:

- Emphasizing consultative skills over technical memorization

- Moving from feature-based selling to solution-oriented conversations

- Equipping sales teams with structured workflows that guide decision-making

- Driving value-based discussions that connect offerings to business outcomes

To make this shift scalable, manufacturers must embed product and pricing expertise directly into their sales processes, allowing teams to focus less on technical validation and more on customer engagement.

Using a Single Source of Truth in Commercial Processes

With traditional sales models heavily reliant on individual expertise, manufacturers must fundamentally rethink how knowledge flows through the organization.

Manufacturers are shifting from expert-dependent translation of engineering specifications to embedding that knowledge in standardized digital processes, like Configure, Price, Quote (CPQ) technology.

This transformation requires restructuring how product information is organized and accessed. A unified product definition helps bridge technical specifications and commercial logic, enabling teams to understand complex offerings without extensive specialized training—while still supporting millions of valid configurations.

For pricing, the challenge is similar. Highly individualized products make pricing difficult, particularly when new variants are introduced. Embedding pricing rules, margin logic and cost considerations directly into commercial workflows enables more consistent and confident pricing decisions without requiring constant expert intervention.

Creating Standardized Components for Mass Customization at Scale

Engineer-to-order models have long provided flexibility, but at the cost of scalability. Shifting toward a hybrid configure-to-order approach allows manufacturers to standardize common configurations while still accommodating unique customer requirements.

Engineering teams can break complex products into modular components and pre-validated options, allowing sales teams to assemble solutions without relying on engineering for every request. These standardized components can then be easily translated into rule-based logic for sales teams.

A key enabler of this shift is constraint-based configuration logic. Instead of rigid rules that limit flexibility, a constraint-based approach to CPQ defines how components can be combined based on shared properties, allowing new modules to be introduced without increasing complexity or sales risk. This equates for fewer rules to be maintained and updated as the portfolio grows.

The Move from Expert-Dependent Selling to Design-Governed Solution Guidance

Technical expertise will become harder to scale. Manufacturers are shifting from expert-dependent interactions to design-governed solution guidance. Guided workflows facilitate customer-focused conversations without requiring deep technical expertise in every interaction, while still enforcing engineering intent and product constraints.

Rather than relying on detailed technical knowledge or feature memorization, structured workflows guide conversations around application requirements, operating conditions and performance outcomes. These inputs are translated into valid, manufacturable solutions based on embedded engineering logic.

- Performance requirements

- Operating environment

- Space or regulatory constraints

- Expected throughput or output

This approach not only protects engineering teams from repeated validation requests, but also improves the customer experience by making complex offerings easier to understand, evaluate and confidently specify.

Buyers Are Losing Expertise Too

A new generation of buyers is entering decision-making committees with mixed technical backgrounds and higher expectations for transparency and guidance.

As customers lose their own internal experts, they increasingly rely on manufacturers to provide clarity earlier in the buying journey, across both traditional and self-service channels. This level of consistency and confidence depends on a single, digitized source of product knowledge that ensures every channel and interaction reflects the same validated information.

Providing intuitive, guided experiences enables buyers to explore options without waiting for human intervention. This ultimately reduces delays and accelerates buyer decision-making.

Scaling Across Products and Markets

Operational transformation takes time, but it pays off. Manufacturers build resilience by standardizing how technical and product knowledge flows from design through order fulfillment. When engineering rules, constraints and configuration logic are embedded directly into lifecycle processes, rather than living in people’s heads or disconnected documents, organizations launch new products and variants faster, limit ongoing engineering involvement in commercial requests, and expand into new markets without redesigning core offerings. This approach shortens time to market and creates more consistent and scalable execution across operations.

Managing Your Workforce for Change

Transitioning to scalable commercial models requires thoughtful change management. Veteran experts should be positioned as champions whose knowledge is being amplified rather than replaced. Phased rollouts, cross-functional alignment and clear communication help ensure adoption while preserving innovation and quality.

Become a Future-Ready Organization

When expertise is embedded into systems rather than tied to individuals, you create operations that can scale, adapt and perform well beyond today’s workforce constraints. M

About the author:

Brian Cuttica is Senior Vice President of Sales in North America at Tacton.

Third-Party Risk Management for Global Supply Chains

Manufacturing leaders can improve real-time supply chain visibility by using advanced technologies, real-time data monitoring, and cross-functional governance.

![]()

TAKEAWAYS:

● Companies should integrate risk management into their daily operations, rather than treating it as a standalone process.

● Advanced technologies allow manufacturers to map their supplier ecosystems with unprecedented depth and precision.

● Data organization and clear data governance are essential for modernizing third-party risk management processes.

The risk landscape for manufacturers is evolving so rapidly that traditional, one-dimensional risk management approaches are becoming obsolete. Supply chain disruptions—whether caused by natural disasters, pandemics, cyberattacks, or supplier insolvencies—are a primary concern for industry leaders. As supply chains become more complex and interconnected, managing third-party risks has never been more challenging. As a result, companies need to integrate risk management into everyday enterprise operations, rather than treating it as a standalone, periodic review process.

The renewed consideration of nearshoring and reshoring strategies adds further complexity as companies adapt their supply networks to shifting global market and regulatory dynamics. In this environment, relying on outdated third-party risk management processes can expose organizations to hidden vulnerabilities and blind spots across their global supplier base.

For C-suite manufacturing executives, the convergence of these factors underscores the need to revisit and reassess internal third-party risk management processes. This is crucial for unlocking data-driven insights that improve supply chain visibility and make the business more adaptable.

Where to Start? Mapping the Supplier Ecosystem

Reassessing third-party risk management processes and frameworks begins with a holistic understanding of the company’s supply network. The first step is to map the entire supplier ecosystem, from strategic Tier 1 partners to smaller, potentially overlooked vendors at the edges of the network, through Tier 2, Tier 3, and even Tier 4 suppliers and partners. This mapping should not be a static exercise. Instead, executives should rate each supplier based on its criticality to business continuity, connectivity to internal systems and data, and adherence to safety, quality, and regulatory compliance standards.

“Data organization and clear data governance are foundational for modernizing third-party risk management processes and achieving real-time supply chain visibility.”

While this task may seem daunting, advanced technologies enable organizations to map and monitor their supplier ecosystem with unprecedented depth, speed, and precision, including understanding downstream supplier dependencies and their impact on operations. Even manufacturers lacking the capacity to build this assessment and monitoring system internally can leverage external advisors to implement technology solutions to manage supply chains and inventory.

Once the ecosystem is mapped, next steps include the following:

- Segmenting and prioritizing suppliers and partners: Segmenting suppliers by risk profile and exposure should consider financial implications, regulatory oversight, and operational dependencies. Developing a comprehensive risk profile for each supplier can help manufacturers identify performance issues, quality concerns, and capacity constraints before they cause major disruptions.

- Updating sales and operations planning (S&OP) processes: Embedding supplier risk profiles into the organization’s S&OP processes reinforces risk awareness as a core element of strategic decision-making. Manufacturers can also integrate this information with broader enterprise risk management efforts for a more holistic approach to mitigating potential disruption.

- Implementing continuous monitoring and governance: Manufacturers need to assess suppliers beyond the onboarding phase. Risk monitoring must continue throughout the entire lifecycle of the supplier relationship, from initial due diligence to eventual offboarding or vendor retirement. Proactive risk identification and mitigation can strengthen existing supplier relationships and show commitment to long-term partnerships.

For effective third-party risk management processes, manufacturers need clear cross-functional ownership structures and defined escalation protocols for addressing issues. IT, compliance, procurement, and operations must collaborate to ensure that risk data is integrated, accurate, and actionable.

How Can Data Enable Real-Time Visibility?

Data organization and clear data governance are foundational for modernizing third-party risk management processes and achieving real-time supply chain visibility. Advanced technologies can help harness data to its fullest potential. Dashboards, Internet of Things-enabled devices, sensors, and connected equipment all feed critical data into centralized platforms that provide actionable insights across the organization. Advanced analytics and machine learning tools can sift through vast quantities of supplier data to flag anomalies, forecast potential disruptions, and recommend proactive mitigation strategies.

Data-driven insights are increasingly becoming essential for companies across all industries. According to a 2025 RSM US LLP report on supply chain issues, most of the 309 executives surveyed said their organizations “already have systems in place to harness data throughout their supply chains.”

On a scale of 1 to 5, respondents reported a surprisingly high level of digital maturity in their supply chains:

- 0% rated their digital maturity at Level 1 (data is gathered ad hoc and manually)

- 3% rated their digital maturity at Level 2 (data is available but inconsistently entered and maintained)

- 28% rated their digital maturity at Level 3 (the company has a big data solution and gathers data from critical inputs)

- 47% rated their digital maturity at Level 4 (data is gathered from every function and automatically analyzed by BI or another data stack)

- 21% rated their digital maturity at Level 5 (enterprise data is unified to a single source of truth)

To remain competitive, manufacturers need to prioritize data architecture and data governance practices. Architectural infrastructure investments, such as cloud-based platforms and integrated data lakes, enable seamless data sharing and real-time monitoring across functions. High-quality, reliable data is the foundation for these efforts; without it, even the most sophisticated technology solutions will fail.

Manufacturers should prioritize data quality initiatives, using advanced technologies to identify and resolve discrepancies and ensure that risk signals are based on accurate, current information. This approach strengthens third-party risk management and enhances overall operational agility.

“Reassessing third-party risk management processes and frameworks begins with a holistic understanding of the company’s supply network.”

Looking Ahead

For manufacturing C-suite executives, reassessing third-party risk management is a strategic imperative for building resilient, transparent, and responsive supply chains in an era of constant change. By embracing a technology-enabled approach anchored in real-time data, continuous monitoring, and cross-functional governance, manufacturers can mitigate risks, identify new opportunities, and deliver greater value to customers, partners, and other stakeholders. M

About the authors:

Katie Landy is a Principal at RSM US LLP.

Jake Winquist is a Principal at RSM US LLP.

Resilient IT/OT Architectures: Protecting Against Cyber and Operations Risk

Manufacturers can follow strategic steps to build resilience across IT and OT environments while advancing their business objectives.

![]()

TAKEAWAYS:

● Manufacturers must engineer resilience through secure-by-design, standards-based architectures that future-proof operations against connectivity failures.

● Edge AI ensures operational continuity by eliminating cloud dependency and preserving real-time decision support during disruptions.

● Lasting cyber resilience requires commitment from IT and OT teams to collaborate and maximize risk reduction.

In today’s rapidly evolving business landscape, manufacturers must accelerate digital adoption to maintain a competitive edge. Embracing advanced technologies drives measurable value by minimizing waste, maximizing uptime, and reducing labor costs. This is achieved through the continuous flow of data across the manufacturing stack, accelerating performance, and unlocking new operational efficiencies. However, increased connectivity between systems introduces increased—and often insufficiently quantified—cybersecurity risk. While manufacturers have always managed threats such as physical access control, and even natural disasters, accelerated digital adoption now exposes operations to more frequent and sophisticated cyber threats than ever before. As these risks intensify each year, the imperative for manufacturers remains urgent and clear: innovate and grow, or lose ground to the competition.

The resulting reality for manufacturers is a conundrum: ambitions to scale and improve operations can appear at odds with security goals to safeguard assets and data and to maintain control. However, manufacturers can balance these objectives by adopting a secure-by-design, standards-based architecture that delivers resilience against cyber and operational disruptions while allowing for seamless connectivity. Because there is no one universal architecture, manufacturing leaders must assess the unique risks connectivity poses to their operations and ensure targeted redundancy planning in the event of disruption. Ultimately, the critical question every manufacturing executive must answer is: can your operations continue when systems go down?

This article outlines the first steps leaders should take to build resilience across IT and OT environments while advancing their business objectives.

First: Business Continuity Planning for Connected Operations

Determining the specifications for the right secure-by-design architecture for your connected operation begins with a business impact analysis (BIA). A BIA analyzes operational functions and the potential effects of a disruption without interrupting or modifying any systems. Mapping assets, systems, and processes into a plant hierarchy helps leaders understand which disruptions would have the greatest operational impact. A separate cybersecurity risk assessment then evaluates threats, vulnerabilities, exploitability, and existing controls for the most critical functions and zones.

During a BIA, leaders must continually ask which parts of the operation are production-critical; that is, which areas must be made resilient to connectivity failure through segmentation and/or redundancy? This analysis provides a clear picture of each asset’s criticality, how failures propagate, and whether existing controls already mitigate the risk. When performed correctly, a BIA will establish the foundation for an architecture tailored to your operations, helping your organization avoid settling for a one-size-fits-all solution that demands costly process changes to function.

Then: Explore Edge AI Architecture for True Resilience

Organizations use BIAs to identify business-critical systems that must remain resilient during disruptions. This drives interest in edge-based intelligence, which, when explicitly designed and governed, can sustain monitoring, control, and safe shutdown functions even when cloud connectivity or other dependent systems are unavailable. By enabling AI at the edge, organizations can shield the “brain” of their operations from disconnection and protect against downtime. This resilience stems from the ability to run AI on-premises. While most AI tools today—especially generative AI—operate in the cloud and can be powerful solutions for tasks like reporting, they are not resilient enough for production-critical tasks because they depend on stable connectivity, external vendors, and infrastructure. Consequently, a failed cloud connection severs the intelligence governing operations.

Unlike larger, general cloud-based AI models, tailored small language models (SLMs) can run directly on industrial PCs, edge gateways, and controllers. This ensures that key decision-support capabilities remain available even without cloud access. Furthermore, SLMs can be tuned more precisely than larger, more general models, allowing them to specialize in specific tasks and provide more efficient real-time troubleshooting and decision support.

“A separate cybersecurity risk assessment then evaluates threats, vulnerabilities, exploitability, and existing controls for the most critical functions and zones.”

Consider this hypothetical scenario: a manufacturing operation, responsible for a significant share of global supply, experiences a connection outage due to an outdated architecture. Because of the nature of its production, any lapse in connectivity, operator visibility, control, or remote support triggers the dumping of all product for safety reasons—an extremely costly and environmentally impactful emergency measure. However, if edge-based intelligence were enabled, it could continue to guide operators by interpreting alarms, troubleshooting issues, and explaining failure modes and safe shutdown or recovery procedures, potentially averting unnecessary product loss.

The challenge with AI lies in selecting the right platform from the many available. Because most AI vendors are cloud-first and lack a deep understanding of industrial edge environments, carefully selecting a partner with operating experience at the edge is the best way to achieve a solution that supports the specific requirements of your operation.

Don’t Forget: Build a Culture of Cyber Resilience

For new approaches to succeed, they must be adopted and sustained by your employees and organizational culture. Leaders can guide their organization’s culture to evolve alongside new technologies by fostering a security-first mindset, treating security as a continuous practice rather than a one-time milestone. Teams should also shift away from a traditional ROI mindset—where investments are justified by direct financial return—and instead prioritize risk, making year-over-year investments to reduce the likelihood and impact of disruptions.

Much of this cultural shift centers on IT and OT teams, which traditionally have had divergent priorities: confidentiality and integrity (CIA) versus safety and availability (SAIC), respectively. True resilience lies at the intersection of IT and OT domains; resilience can only be achieved when these teams collaborate on architecture decisions, risk assessments, incident response planning, and governance. This achievement is a shared responsibility.

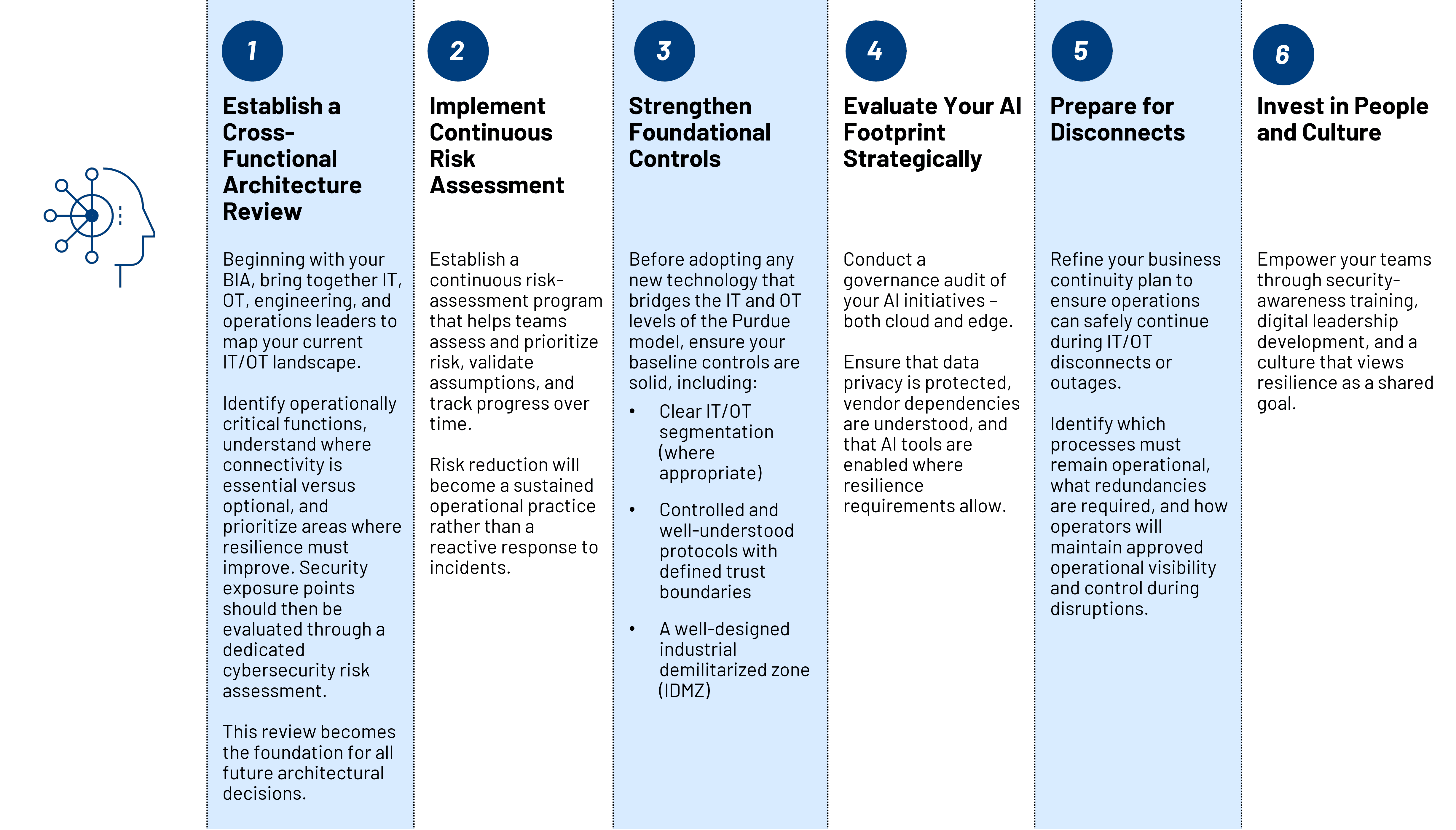

Step by Step: What Leaders Can Do Now

Figure 1: Steps Leaders Can Take Toward Resilience

Building resilience is not a one-time initiative but an ongoing commitment (Figure 1). It requires a secure-by-design architecture, edge-ready intelligence, and a culture that treats cybersecurity as foundational to operational excellence. As connectivity deepens and threats evolve, leaders who invest in continuity planning, adopt technologies purpose‑built for the industrial edge, and unite IT and OT teams around shared responsibility will position their organizations for success. Resilience is no longer achievable through a default defense posture. Manufacturers can only confidently operate, grow sustainably, and field emerging threats in an increasingly connected world through bold innovation and strategic thinking. M

About the authors:

Chris Hamilton is a Digital Consulting Sr. Manager & Cybersecurity Platform Lead at Rockwell Automation Digital.

Will Rosengarten is the Data Strategy & Architecture Lead at Rockwell Automation Digital.

Welcome New Members of the MLC February 2026

Introducing the latest new members to the Manufacturing Leadership Council

![]()

Learn more about MLC membership.

Sthitie Bom

VP Global Manufacturing IT

Seagate

https://www.seagate.com/

![]()

https://www.linkedin.com/in/sthitie/

Tim Brown

VP, Information Technology

RYAM

![]()

https://ryam.com/

![]()

https://www.linkedin.com/in/timothy-brown-ba894013/

Jeff Elkin

SVP Information Technology

Marvin

![]()

https://www.marvin.com/

![]()

https://www.linkedin.com/in/jeff-elkin-16382b4/

Ed Maier

President and CEO

G.W. Lisk

![]()

https://www.gwlisk.com/

![]()

https://www.linkedin.com/in/edward-maier-b2b3051a/

Kerry McQuone

CMO

GrayMatter Systems

![]()

https://graymattersystems.com/

![]()

https://www.linkedin.com/in/kerry-mcquone-995a406a/

Danny Seigle

VP, Partnerships and Alliances

MaintainX

![]()

https://www.getmaintainx.com/

![]()

https://www.linkedin.com/in/dannyseigle/

Lance Whitacre

Senior Vice President, Manufacturing and Logistics

Andersen Windows & Doors

![]()

https://www.andersenwindows.com/

![]()

https://www.linkedin.com/in/lance-whitacre/

Alex White

Vice President, Strategic Engagements

Infor

![]()

https://www.infor.com/

![]()

http://linkedin.com/in/alexanderleewhite/

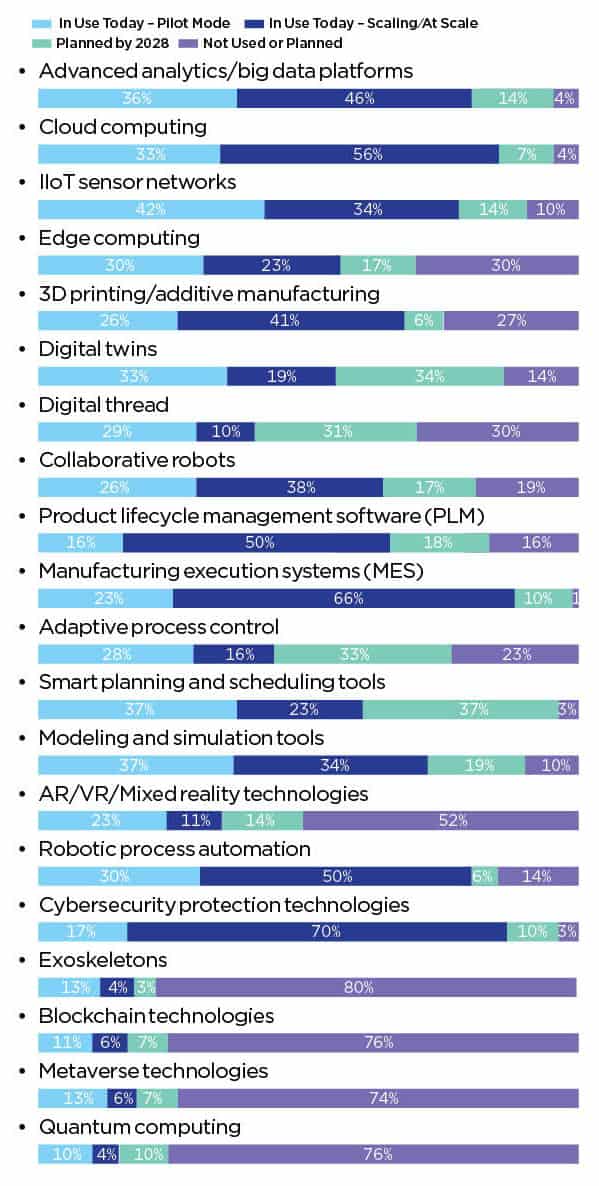

Survey: Smart Factories Enter the Execution Era

Manufacturers push deeper into execution as smart factory strategies mature, AI advances and digital transformation gains as a competitive advantage.

![]()

KEY TAKEAWAYS:

● Smart factories have entered the execution era with manufacturers now wrestling with how to scale digital transformation efforts

● AI is maturing beyond experiment into value-driven, smart factory deployments

● Digital transformation is shifting from table stakes to a game-changing advantage

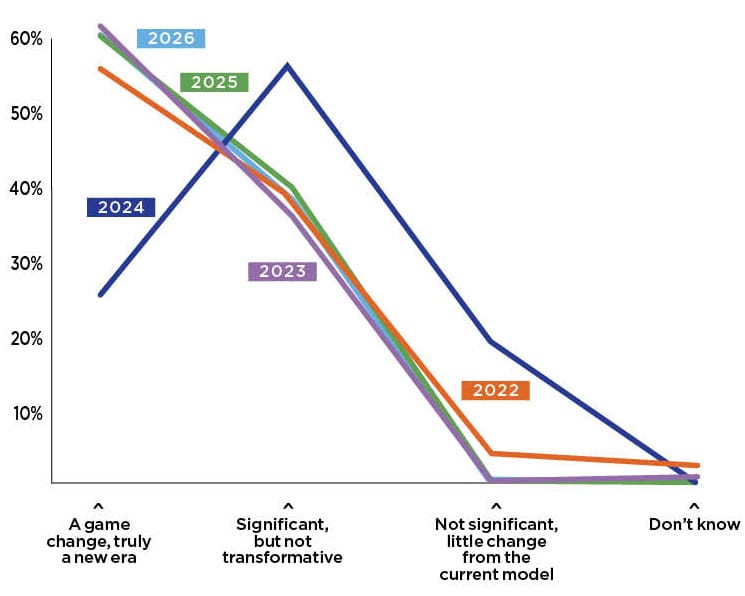

The Manufacturing Leadership Council’s 2026 Smart Factories and Digital Production Survey shows an industry that has moved beyond experimentation and into a more disciplined phase of execution, integration and operation. Manufacturers are increasingly committed to digital transformation and are now figuring out how to scale it.

While economic optimism and investment intent remain strong, the tone of this year’s survey reflects a more mature mindset. Expectations remain high for AI, automation and end-to-end digitization, but respondents also demonstrate a clearer understanding of the legacy, data and organizational challenges that accompany scale. Compared to 2025’s resurgence of momentum and 2024’s momentary hesitation, 2026 signals a new phase: steady progress, pragmatic confidence and a sharper focus on execution.

SECTION 1: Economic Outlook and Investment Trends

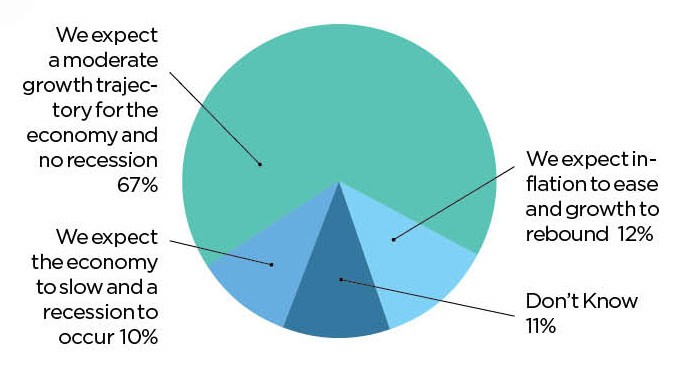

Manufacturers enter 2026 with cautious optimism about the broader economy. A strong majority (67%) expect moderate growth, while only 10% anticipate a significant downturn (Chart 1). These numbers remain similar to the 2025 survey results where 69% expected moderate growth while 8% expected an economic slowdown.

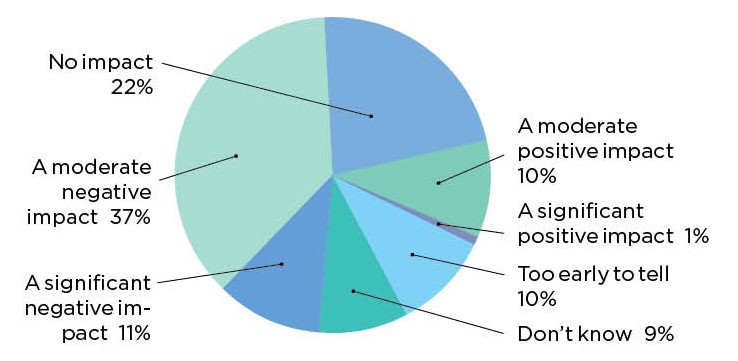

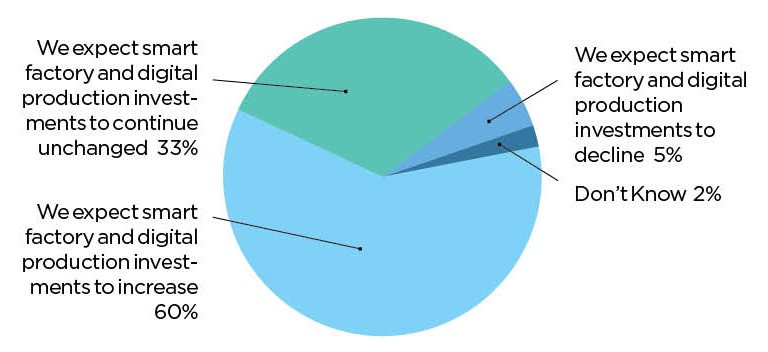

Meanwhile, nearly half of the respondents (48%) say U.S. tariffs are having a moderate or significant impact on their smart factory implementation (Chart 2). While those sentiments are worth watching going forward, the tariff negatives are not enough to undermine Manufacturing 4.0 digital investments. More than 90% of respondents say they expect to maintain or increase smart factory and production technology investments in 2026, with a sizable share planning increases rather than flat spending (Chart 3). The data suggests that digital investment has become embedded in long-term operating plans rather than driven by short-term economic sentiment.

1. Strong majority expect moderate economic growth ahead

Q: What is your company’s outlook for the economy in 2026? (Select one)

2. Nearly half experiencing negative impact from U.S. tariffs

Q: What impact are U.S. tariffs having on your company’s smart factory implementation? (Select one)

3. More than 90% plan to maintain or increase smart factory investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2026? (Select one)

SECTION 2: Smart Factory Maturity and Adoption