SURVEY: Choppy Supply Chain Seas Making Skilled Sailors

MLC’s latest survey reveals continued disruptions and challenges but big shifts in digital technology deployments and supply network geography.

![]()

Franklin D. Roosevelt is credited with saying, “A smooth sea never made a skilled sailor.”

As we move another year away from the COVID-19 pandemic that set off a wave of supply chain disruptions, we continue to see how those initial ripples have been amplified and compounded by component and material shortages, inflation and transportation cost increases, worker shortages, military conflict, political tensions, and other complexities that have tested supply chain resiliency.

In the face of these stormy seas, the manufacturing world continues to implement technologies and solutions to help overcome ongoing disruptions while girding supply chains for a more resilient future.

The MLC’s latest Resilient M4.0 Supply Chain survey reveals manufacturing leaders’ expectations and insights related to supply chain challenges, digital technologies, partnerships, and resiliency. It is clear that disruption still abounds, and respondents expect this to continue for at least the next 12-24 months.

At the same time, this year’s survey indicates that supply chains may be less resilient than our 2022 survey found. Nearly 23% of respondents now say their supply chain is not resilient – up from 12% last year. Perhaps, this sentiment is driven by the necessary rapid digital transformation and geographic shift that many supply networks have undergone.

If the supply chain waters remain choppy, manufacturers’ efforts to implement technology, transform their supply networks, and create better partner collaboration will lead to skilled sailors who can navigate future disruptions or calm seas – whenever those arrive.

Part 1: Supply Chain Disruptions

What started with a single cause for disruption is now a mixing bowl of many disruptive factors that continue to cause issues for manufacturers. Supply chain disruptions that were initially rooted in the COVID-19 pandemic have expanded to include the Ukrainian War, tensions with China, and more.

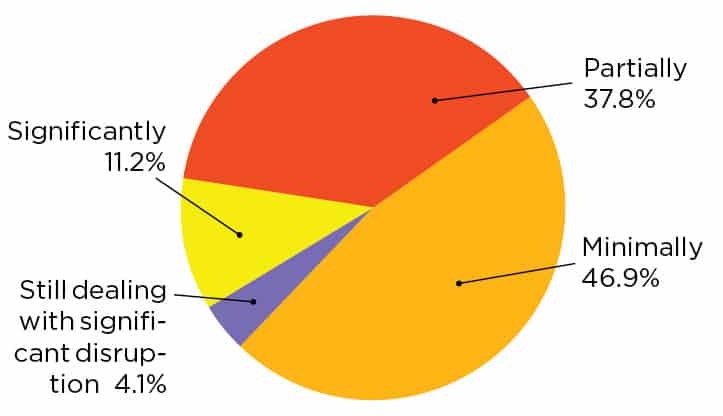

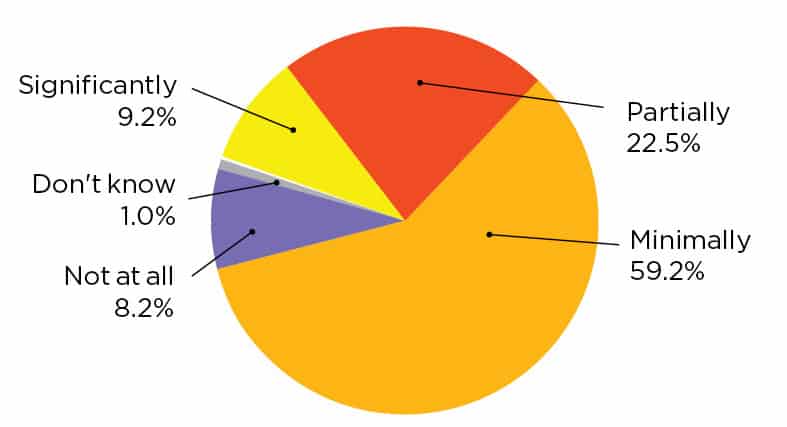

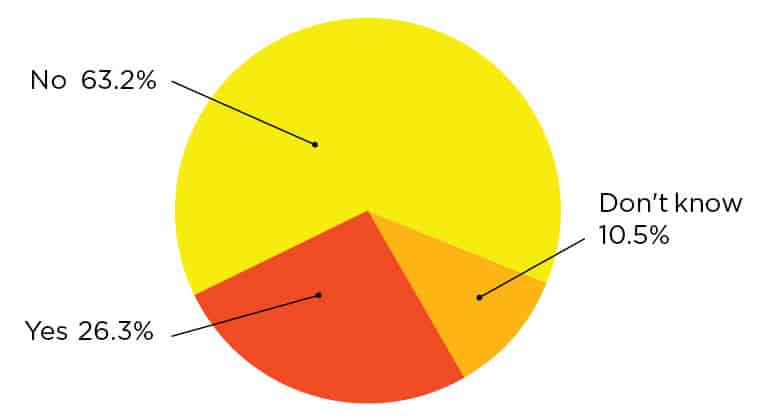

Still, survey respondents report that pandemic-induced disruptions have eased some. About half say they have eased significantly or partially while 47% say they have only eased minimally. [CHART 1] Meanwhile, other high-visibility supply chain disruptions from the Ukraine War and China tensions are not causing significant disruptions at this time, with nearly 67% of respondents reporting minimal or no disruptions from these catalysts. [CHART 2]

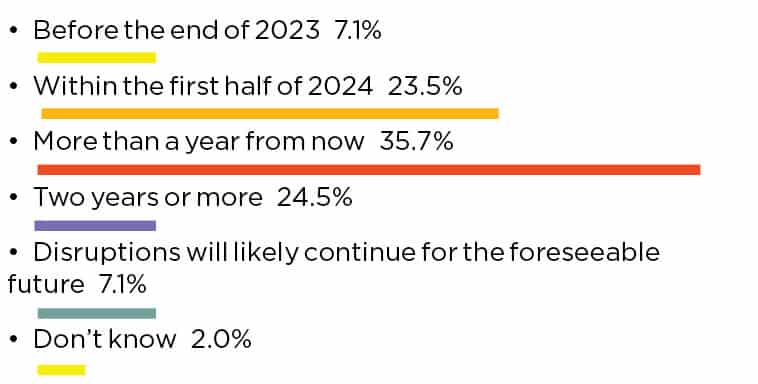

Despite the easing of disruptions from the pandemic and the reported low impact from Ukraine and China, respondents still see supply chain disruptions lingering for some time. In fact, nearly 36% believe disruptions will last for more than a year and nearly a quarter more believe the disruptions could stretch into 2025. [CHART 3]

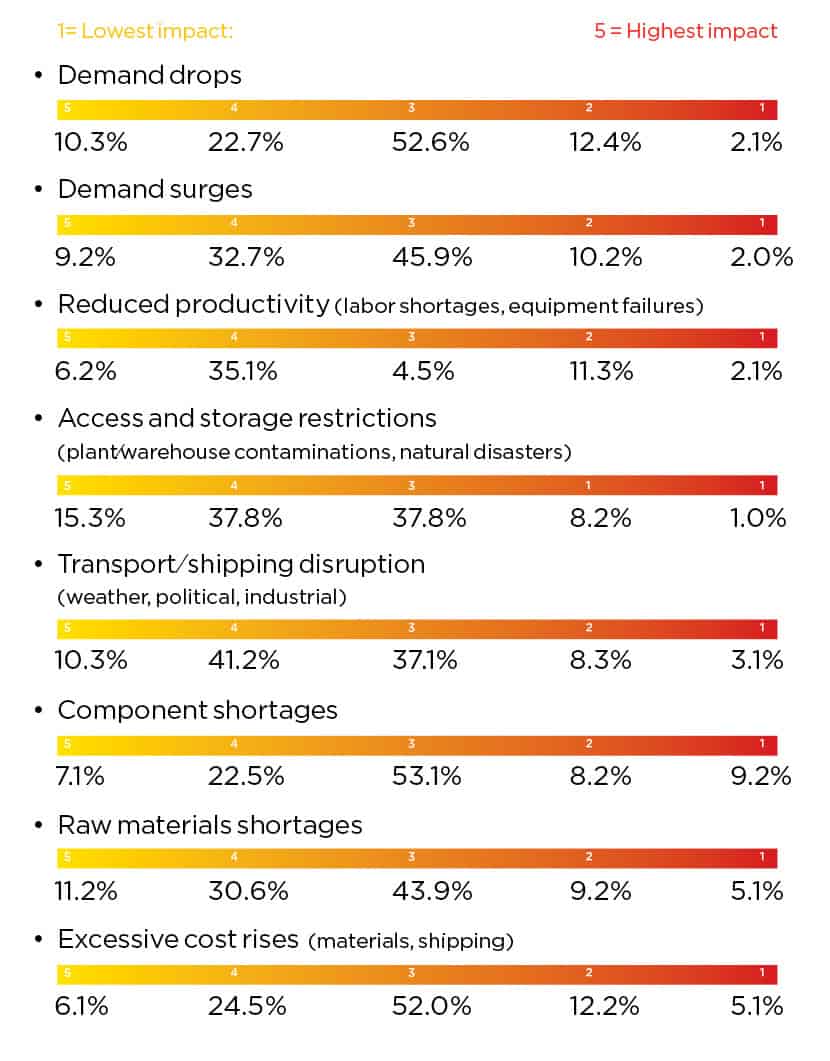

Perhaps the lingering supply chain issues stem from several disruptive forces and a synergistic effect as several supply disruptions combine to become causes for further disruption. We asked about eight different types of disruptions that manufacturers have experienced in recent years and their impact. Leading the charge, component shortages and excessive cost rises for materials and shipping both ranked as a four or five (highest level of impact) for 17% of respondents, while demand drops, raw materials shortages and reduced productivity from labor shortages and equipment failures round out the top five disruptions with the highest impact. [CHART 4]

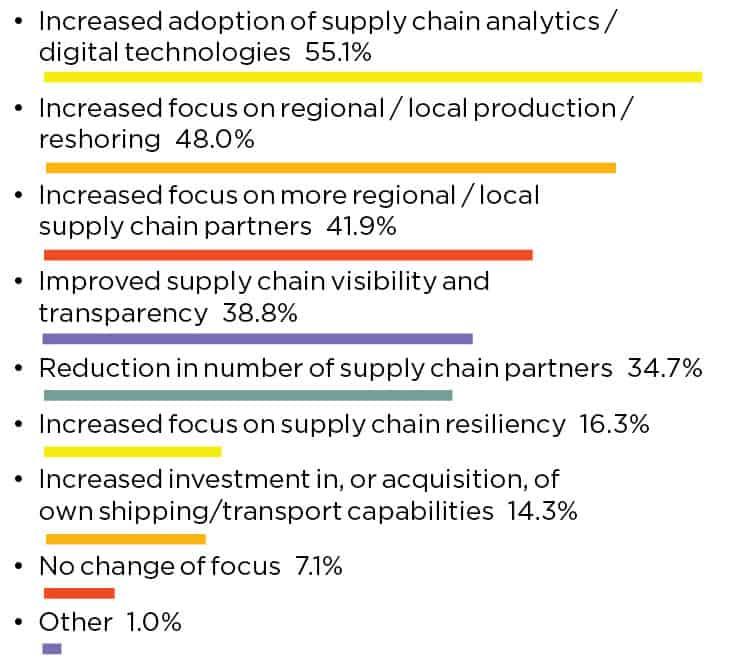

But from adversity, innovation arises, and manufactures report they are taking steps to mitigate future supply chain disruption. Among the leading new strategies, 55% say they are adopting supply chain analytics and digital technologies; 48% are increasing their focus on regional or local production and reshoring; 42% are focusing on regional and local supply chain partners; and 39% are improving their supply chain visibility and transparency. [CHART 5]

1. Pandemic-related Disruptions Persist

Q: To what extent have pandemic-induced supply chain disruptions eased for your company? (select one)

2. Global Unrest and Tension Causing Minimal Supply Chain Disruption

Q: To what extent have the Ukraine War and tensions with China affected your supply chain? (select one)

3. Most Expect Disruptions to Subside in Next 12-24 Months

Q: If you are still experiencing supply chain disruptions, when do you expect the disruptions to subside? (select one)

4. Components, Raw Materials, and Costs Causing Biggest Supply Chain Impact

Q: Over the last several years, what have been the most impactful types of supply chain disruptions you have encountered? (scale 1-5, where 5 is highest level of impact)

5. Analytics/Digital Tech and Supply Chain Geography are Biggest Strategies to Avoid Disruption

Q: What strategies are you adopting to mitigate future supply chain disruption? (select all that apply)

Part 2: Improving Resiliency

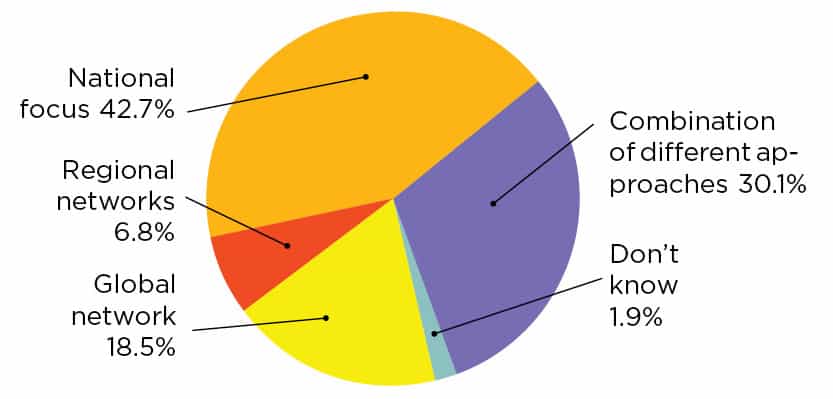

Building off these new strategies, manufacturers report a dramatic shift in their supply chain network’s geography. In MLC’s 2022 supply chain survey, 51% reported a global supply chain network. Now, just 18% of respondents report a global network. This shift has led to a significant increase in those with a national focus (43% in 2023 compared to 12% in 2022) and a combination of different approaches (30% in 2023 compared to 19% in 2022). [CHART 6]

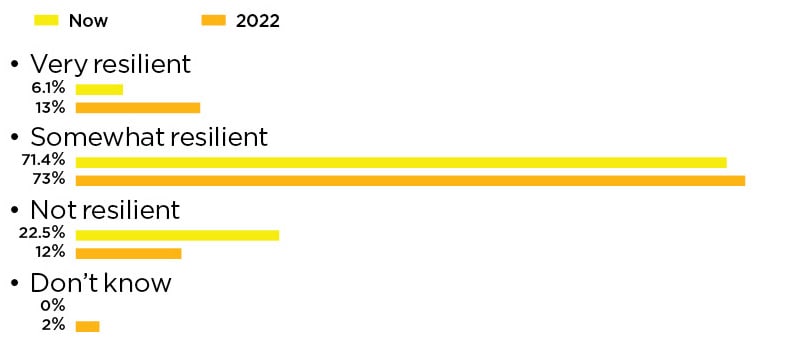

The rapid nature of this shift may be responsible for a less resilient supply chain in the short-term. While most respondents still report their supply chain is somewhat resilient (71% in 2023 compared to 73% in 2022), there has been an increase in those reporting that their supply chain is not resilient. For 2023, that number stands at nearly 23% while it was 12% in April 2022. [CHART 7] Time will tell if this is, in fact, a temporary regression as supply networks realign geographically.

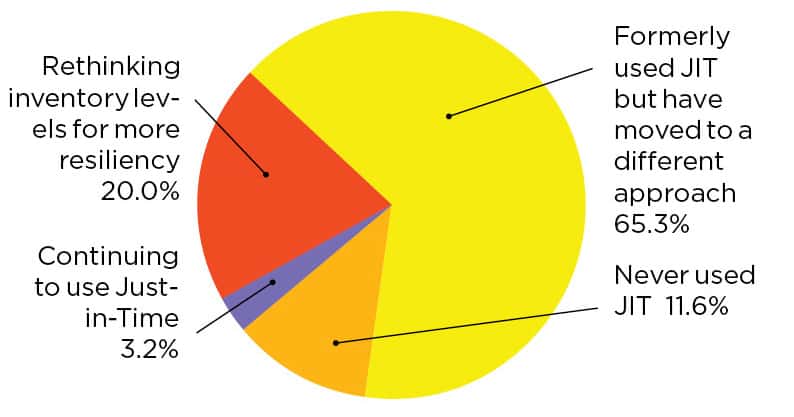

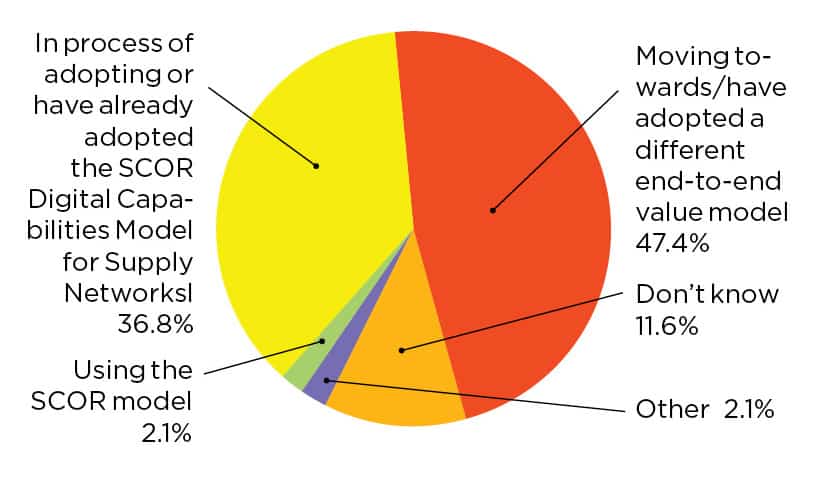

One way manufacturers may be bolstering their resiliency is reexamining traditional supply chain strategies. There is a clear move away from the Just-in-Time (JIT) approach. In 2022, 12% reported that they were continuing to use JIT, while just 3% continue to use it according to the latest survey data. Now, 65% of respondents report that they formerly used JIT, but have moved to a different approach. [CHART 8] Additionally, just under half of respondents (47%) report they are moving towards or have adopted an end-to-end value model other than SCOR. That leaves 2% that are using SCOR and nearly 37% that are adopting or have adopted the SCOR Digital Capabilities Model for Supply Networks. [CHART 9]

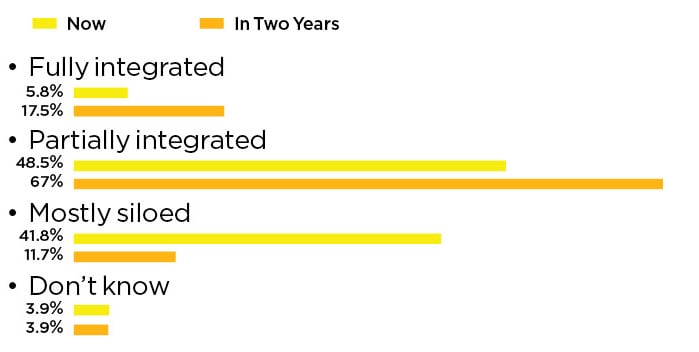

As these shifts take place, there is some optimism that the efforts will pay off in the next two years. Forty-one percent of respondents report that their supply chain functions are mostly siloed today, but that number is predicted to drop to just under 12% in 2025. At the same time, partially integrated supply chains are predicted to grow from 49% to 67% while those with a fully integrated supply chain are forecasted to increase from 6% to 18%. [CHART 10]

6. Companies Shift Away from Global Supply Chain Network

Q: Geographically, how is your supply chain network structured? (select one)

7. Still, resilient supply chains remain an issue

Q: How would you rate your current supply chain’s resiliency? (select one)

8. Just-in-Time’s Usage Continues to Fade

Q: How would you describe your company’s use of the Just-in-Time approach? (select one)

9. End-to-End Value Models Moving Toward Majority Adoption

Q: Does your company use SCOR as its basic supply chain model or are you using or moving toward a different end-to-end value model? (select one)

10. Siloed Supply Chain Functions Begin to Disappear

Q: To what extent are your supply chain functions integrated today and do you expect them to be integrated in two years’ time? (select one)

Part 3: Digital Supply Chains

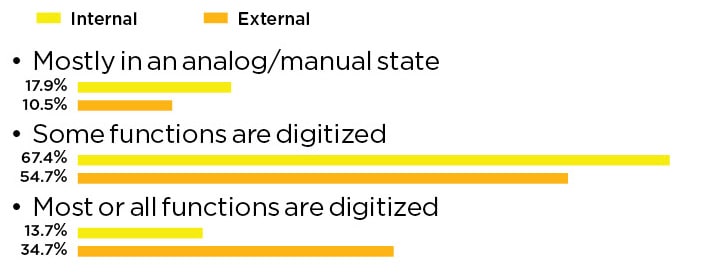

For respondents, their digital maturity for external supply chain functions is slightly outpacing their internal supply chain functions’ digital maturity. Just under 90% say some, most or all their external functions are digitized, while 81% say some, most or all their internal functions are digitized. This means that about 18% of respondents characterize their internal supply chain functions as mostly in an analog or manual state, while about 11% of respondents say the same about their external functions. [CHART 11]

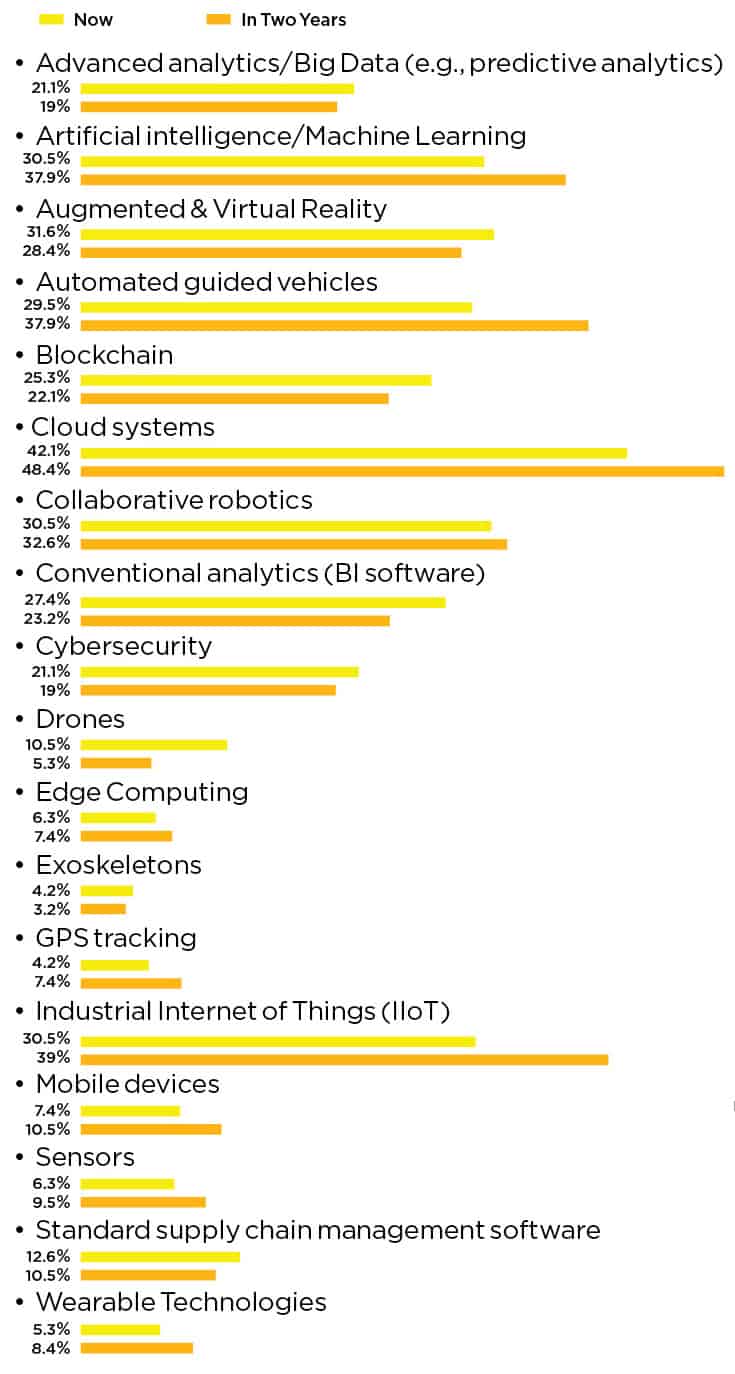

Many technologies are now in use to help digitize manufacturers’ supply chains. Currently leading the pack are cloud systems (in use for 42% of respondents) and augmented and virtual reality (32%). Rounding out the current top five, are artificial intelligence/machine learning, collaborative robotics, and Industrial Internet of Things (IIoT), all of which are being used to digitize just under 31% of respondents’ supply chains. Looking ahead to 2025, use of these technologies will most likely increase. Cloud systems are expected to be in use for 48% of respondents; IIoT is expected to be employed by 39% of respondents; cobot deployments will grow slightly and be in use in 33% of respondents’ supply chains; and AI/ML is expected to be in use for 38% of respondents. Our respondents also expect automated guided vehicle usage to grow from 30% now to 38% in 2025, while augmented and virtual reality usage will slip to 28% in two years’ time. [CHART 12]

As digital technology adoption grows, companies are no longer taking the opportunity to also redesign their supply chain processes. This may be because so many reported that they were redesigning their processes in the 2022 survey. At that time, 72% said they were redesigning their processes as they adopted more digital technologies. In the most recent survey, however, that number has dropped to just 26%. [CHART 13] If AI adoption grows as expected by 2025, it will be interesting to keep an eye on supply chain process redesigns to see if there is a corresponding increase.

11. Digital Maturation Continues

Q: Which description best characterizes the digital maturity of your internal and external supply chain functions today (plan, source, make, deliver)? (select one)

12. Cloud Systems, AI/ML and AGVs are the Present and Future of Digital Supply Chains

Q: What technologies are you currently using and do you expect to be using in two years to digitize your supply chain? (select all that apply)

13. Digital Adoption Not Driving Supply Chain Redesigns

Q: As you adopt more digital technologies across your supply chain, are you also taking the opportunity to redesign your supply chain processes? (select one)

Part 4: Supply Chain Partners

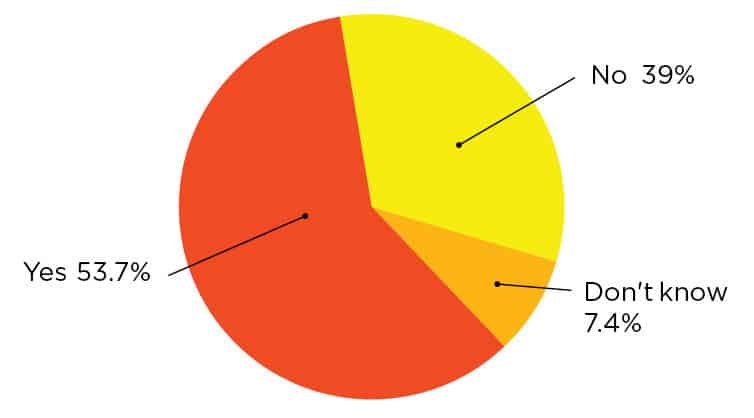

Perhaps driven by more localized supply networks, companies are making an effort to help their supply partners accelerate their digitization efforts. In 2023, 54% of respondents say they are helping their supply partners. This is up significantly from 2022 when just 19% reported they were supporting this effort. [CHART 14] Eventually, these efforts may ensure a more effective end-to-end digital supply network including multiple supplier tiers.

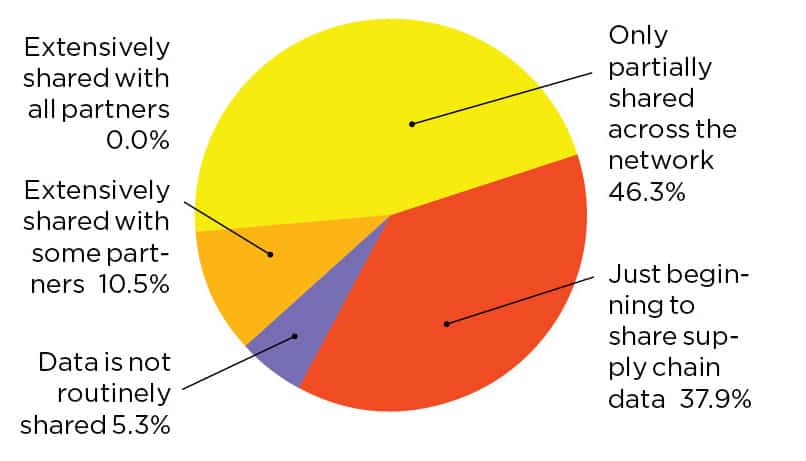

A potential area for growth with partner collaboration is data sharing. Just under 11% of respondents say they share data extensively with some partners while 5% say data is not routinely shared. But there is a light at the end of the tunnel: 38% say they are beginning to share supply chain data among partners and another 46% say they are partially sharing data across their networks already. [CHART 15]

14. More than Half Aid Supply Chain Partners’ Digital Maturity

Q: Has your company made any specific efforts to help support your supply chain partners accelerate the maturity of their digitization efforts to ensure a more effective end-to-end digital supply network? (select one)

15. Nearly All Respondents Share Some Data Between Supply Chain Partners

Q: To what extent is data routinely shared between any or all of your supply chain partners? (select one)

Part 5: Challenges, Goals and Outcomes

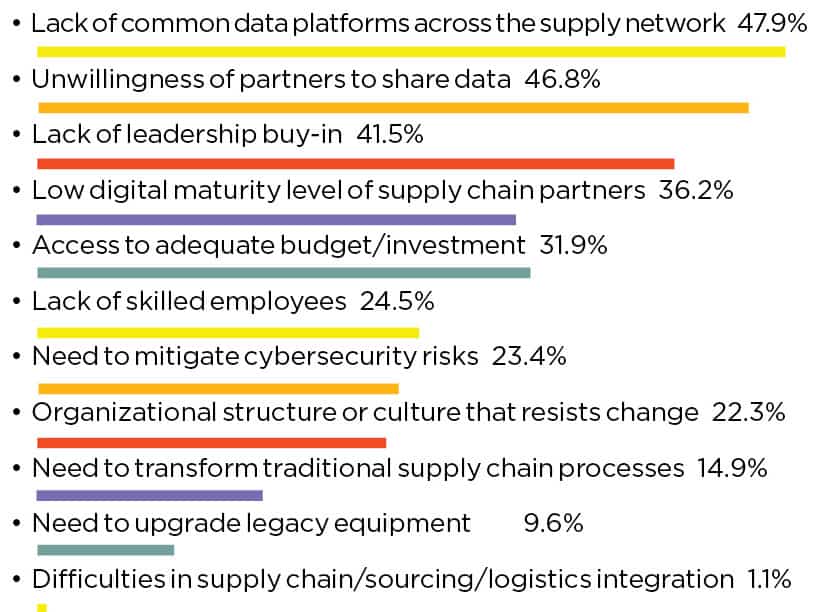

To implement an end-to-end digital supply chain strategy, significant challenges exist that must be addressed with organizational and people changes or new technologies. Respondents were asked to identify their top three challenges. Lack of common data platforms across the supply network led the way in the 2023 survey with 48% of respondents identifying this challenge. This is down slightly from 2022 when it appeared in 53% of respondents’ top three. Trailing just behind, 47% of respondents labeled the unwillingness of partners to share data as one of their biggest challenges. Beyond data hurdles, 42% say a lack of leadership buy-in and 36% say low digital maturity of supply chain partners are holding back their digital supply chain strategy. Meanwhile, 32% say that access to an adequate budget or investment is one of their top three challenges. [CHART 16]

Survey respondents are seeking several business goals related to their digital supply chain transformation. Increased supply chain resiliency, improved customer experience, and new business model/competitive advantage rank as the top three most important goals. These were identified as high importance on 43%, 33%, and 31% of the surveys, respectively. [CHART 17]

16. Data Issues Pose Biggest Challenge to End-to-End Digital Supply Chain Strategy

Q: What are your company’s primary challenges in implementing an end-to-end digital supply chain strategy? (select top three)

17. Customer Experience, Resilience Biggest Goals of Digital Supply Chain Transformation

Q: How important are the following business goals associated with your digital supply chain transformation? (rate as low, moderate or high importance)

About the author:

Jeff Puma is Content Director for the Manufacturing Leadership Council

Survey development was led by the MLC editorial team with input from the MLC’s Board of Governors.