Survey: Smart Factories Are Still a Work in Progress

Manufacturers are moving ahead with creating smarter factories as they grapple with cultural resistance and integrating new technologies.

![]()

TAKEAWAYS:

● A majority of manufacturers say their investments in M4.0 technologies to create smart factories will continue unchanged this year.

● Most manufacturers are at an intermediate stage with M4.0 adoption.

● The most significant roadblock to implementing a smart factory strategy is an organizational structure or culture that resists change.

Tracking the evolution of factories and plants to become so-called smart facilities is a bit like trying to discern the movement of a glacier. You can watch intently but it is hard to detect change. And when change does occur, it is measured in inches. But like a glacier, over time the movement to smart factories and plants will encompass all a production facility does and in a profound way.

The manufacturing industry is inexorably marching toward a day when smart factories and plants, powered by intelligent, sensor-based networks that generate vast volumes of data that are analyzed by artificial intelligence systems, will operate with less human intervention. Highly automated, increasingly intelligent and flexible, the smart factory of the future beckons.

As we head toward that promised land, we look for markers along the way, indications that may tell us where we are making progress and where the obstacles to that progress may lie. The Manufacturing Leadership Council’s new Smart Factories and Digital Production survey sheds light on those markers.

Section 1: STATUS OF DIGITAL INVESTMENT AND ADOPTION

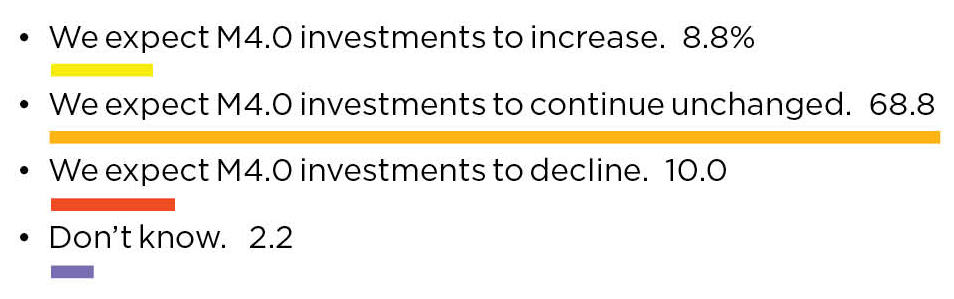

At the highest level, the industry’s posture with regards to investing in Manufacturing 4.0 technologies to create smart factories appears to be on solid footing. In the new survey, nearly 69% of respondents indicated that their M4.0 investments this year would continue unchanged from last year. Nearly 19% said they would increase investments and only 10% said their investments would decline (Chart 1). Concerns about a recession have evidently eased.

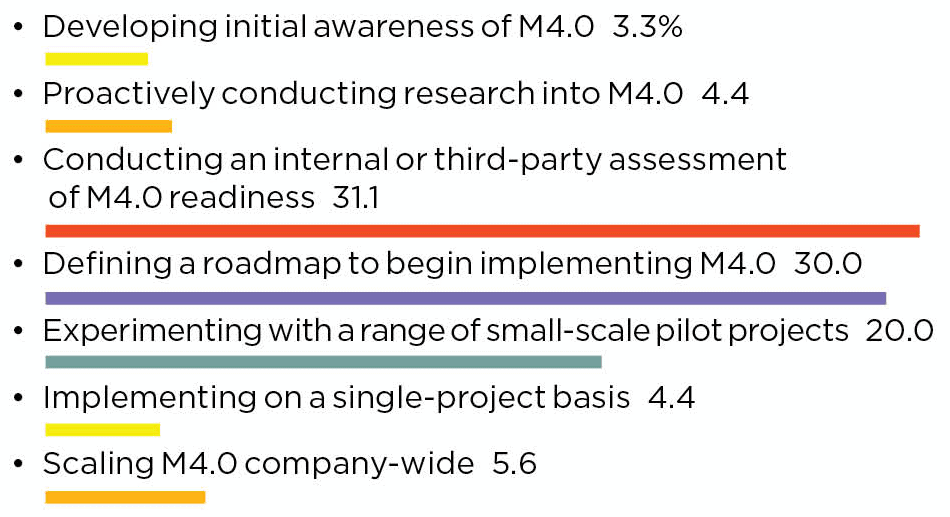

As manufacturers continue to invest in digitalization, they have moved from the initial stages of developing awareness and conducting research into M4.0 to action. Thirty percent of the respondents to the survey say they implementing small-scale pilots, experimenting with a range of projects, or scaling M4.0 companywide. Interestingly, about 31% report they are at the stage of conducting M4.0 readiness assessments, which, when completed, should spawn many pilots and projects (Chart 3).

“The manufacturing industry is inexorably moving toward a day when smart factories and plants …will operate with less human intervention.”

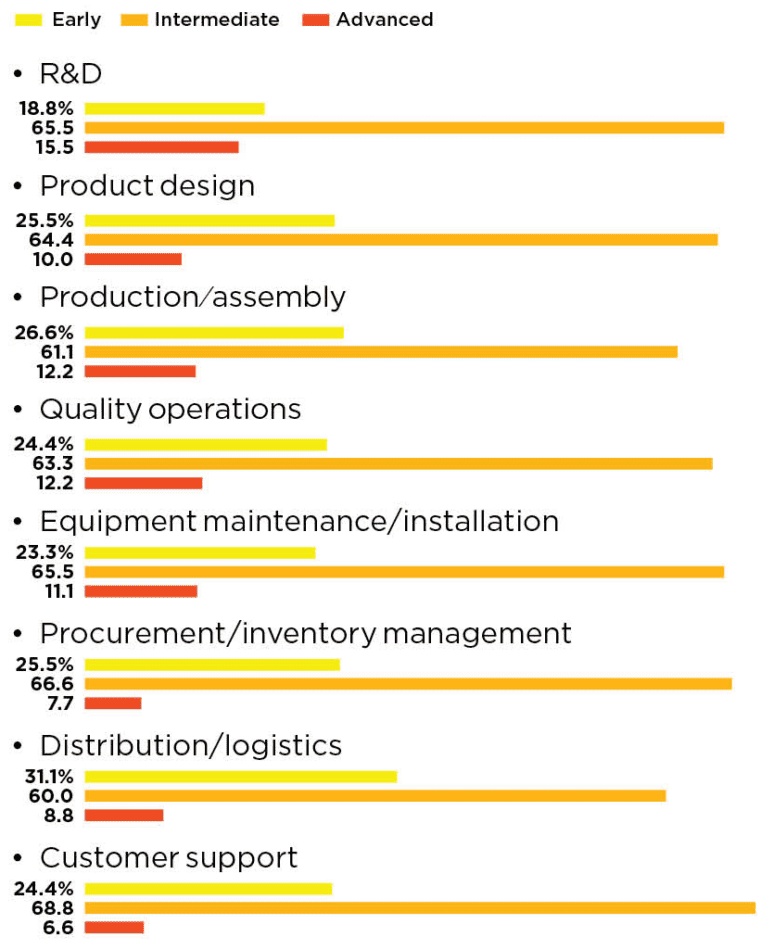

When looked at the stage of adoption functionally – in R&D, product design, and in production and assembly, for example – a strong majority of respondents say they are at an “intermediate stage” with M4.0. Those at an “advanced” stage represent only single-digit or low double-digit constituencies (Chart 4).

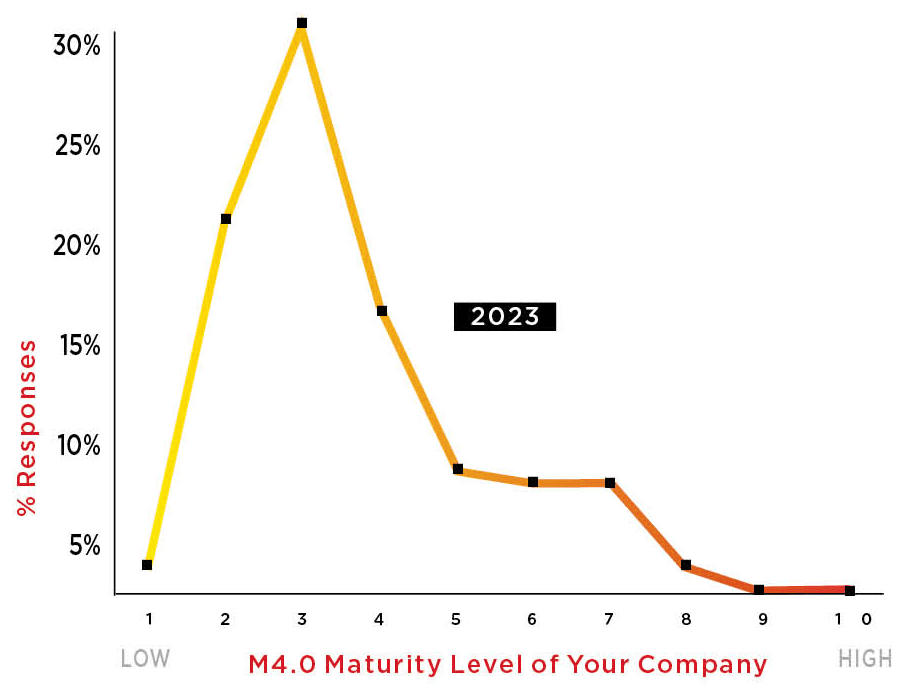

Overall, when respondents were asked to assess the digital maturity level of their manufacturing operations, about 58% said that, on a scale of one to 10, they are in the three to five range, which supports the view that the industry has moved beyond the initial stages of M4.0 and is approaching an early majority of those embracing the digital model (Chart 2).

1. Economy Notwithstanding, Strong Majority Sees No Change to M4.0 Investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2024?

2. Nearly Half Are in Early Stage of Digital Maturity

Q: How would you assess the digital maturity level of your manufacturing operations?

3. Readiness Assessments, Roadmaps Dominate Stage of M4.0 Efforts

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today?

4. Functionally, Most Firms Are in the Middle Stage of Digital Adoption

Q: At what stage of digital adoption are the following functions in your company?

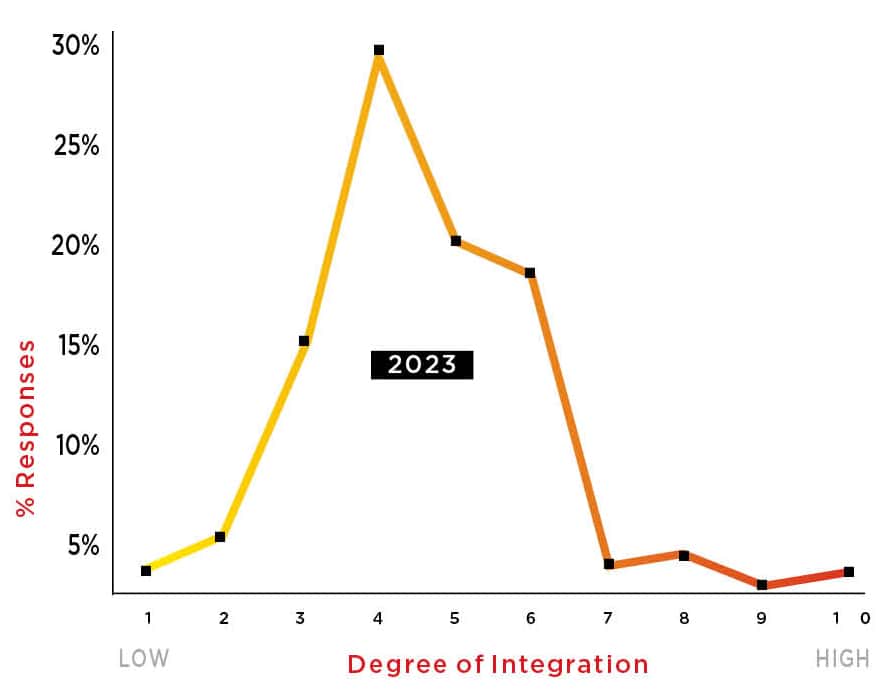

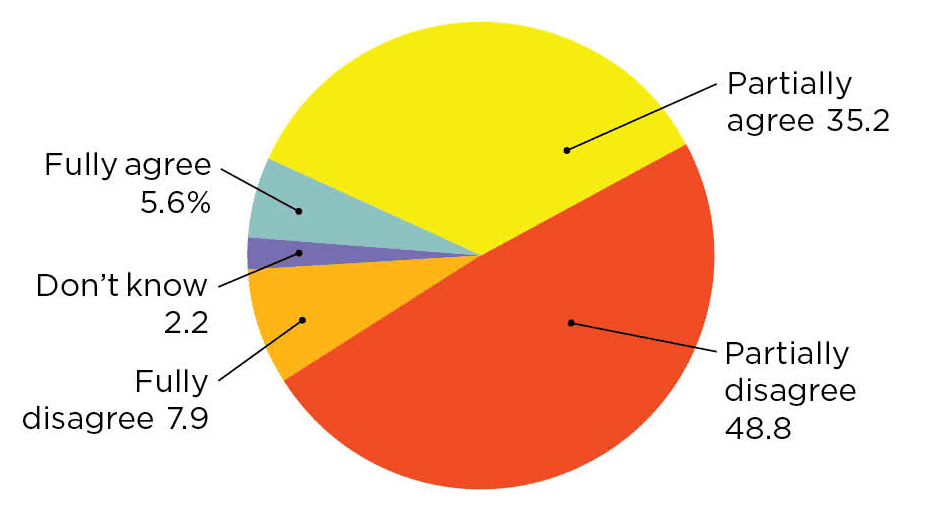

5. Few Have Fully Integrated Smart Factory Strategies With Business Strategies

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy?

Section 2: MEASURING DIGITIZATION

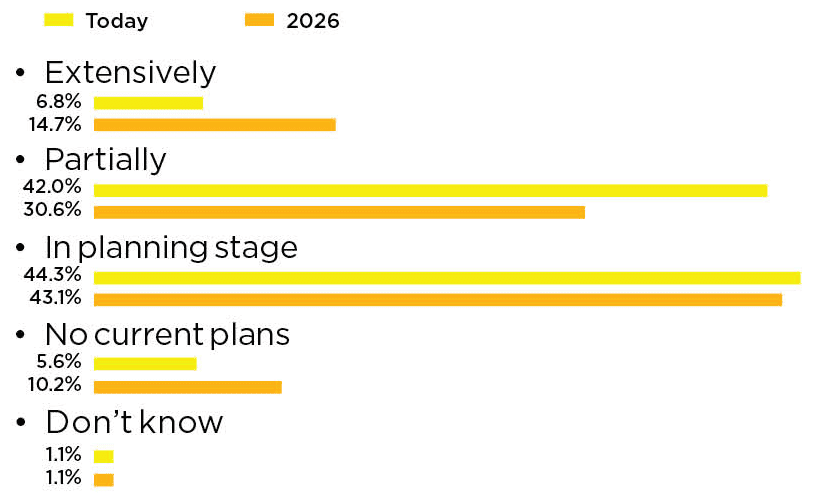

Not surprisingly, only a fraction of manufacturers, 6.8%, report that they have “extensively” digitized their factory operations today. Most have either partially digitized or are in the planning stages of doing so. But when asked to anticipate the extent of digitization by 2026, 14.7% said they expect to be extensively digitized on an end-to-end basis in that timeframe (Chart 6).

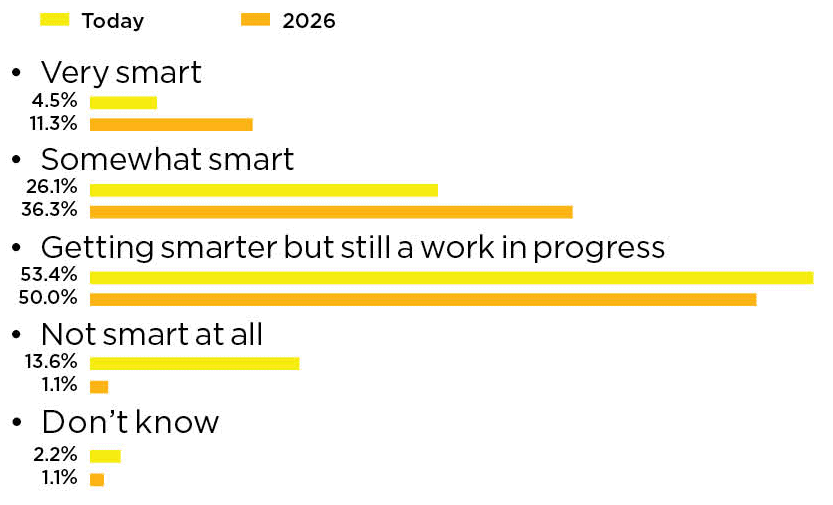

Correspondingly, only a fraction of respondents, 4.5%, would be ready to say their factories are “very smart” today, but, once again, aspirations are high. By 2026, 11.3% expect to be able to affix that label to their operations. But for the moment, a majority of respondents, 53.4%, say their factories and plants are getting smarter but are still a work in progress (Chart 7).

6. More Fully Digitized Operations on the Horizon

Q: To what extent are your factory operations fully digitized end to end today, and what do you anticipate they will be by 2026?

7. “Smart” Factories Still a Work in Progress

Q: How “smart” do you consider your factory and plant operations to be today?

Section 3: FACTORY ORGANIZATION AND MANAGEMENT

So where is all this digital work heading? What do manufacturers expect their factory models to look like in the years ahead?

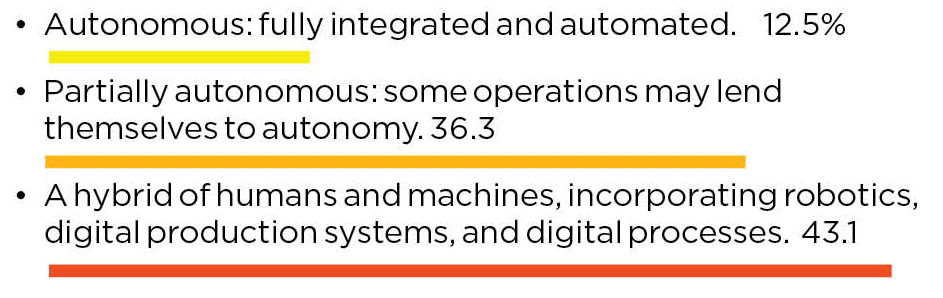

The idea and prospect of some level of autonomous operation is clearly on radar screens. Nearly half of the respondents, 48.8%, expect their future factory models to be autonomous, defined as fully integrated and automated, or partially autonomous, defined as some operations or processes conducted autonomously (Chart 8).

8. Autonomous Operations is on the Radar Screen

Q: What is the expected future state of your factory model?

9. A Majority Does Not See Self-Learning Factories in the Future

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.”

Section 4: TECHNOLOGY USAGE

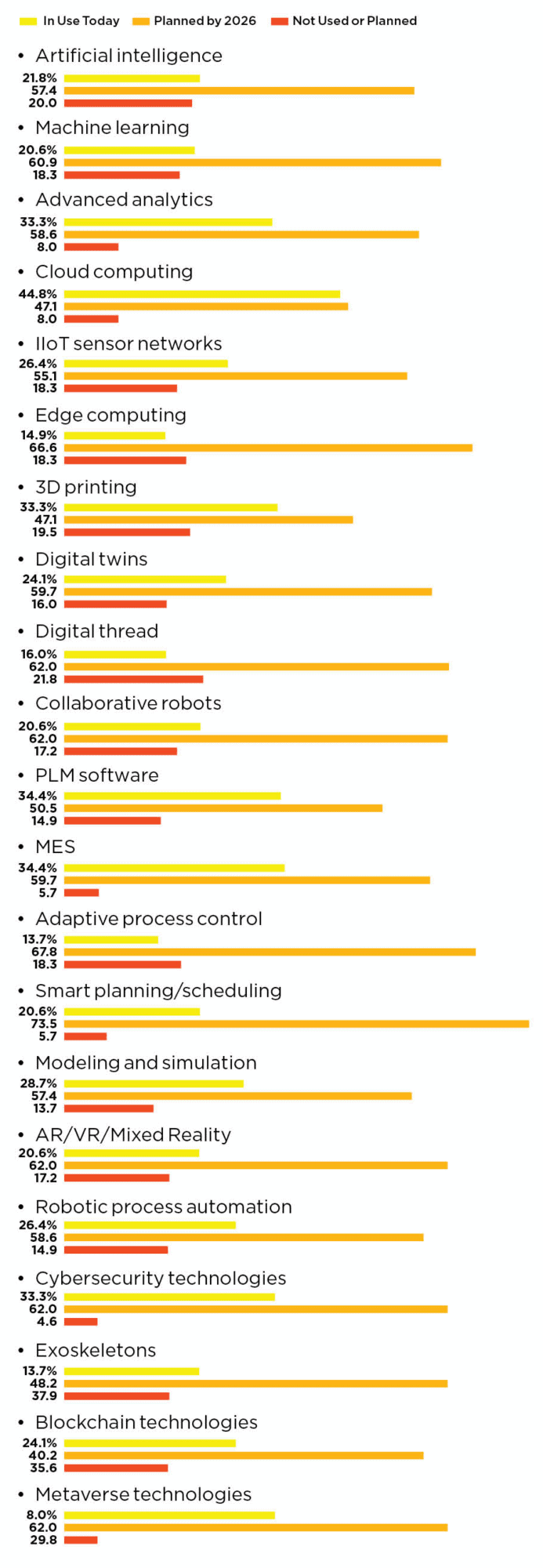

There is an expanding basket of advanced technologies manufacturers will be using to create their smart factories and plants.

When asked about adoption status on 21 technologies, the most striking thing was how strong planned adoption was by 2026. Eight of the technologies surveyed – for example, machine learning, edge computing, digital threads, AR/VR, and Metaverse technologies – all received 60% or higher planned adoption responses. Eight others garnered 50% or higher responses (Chart 10).

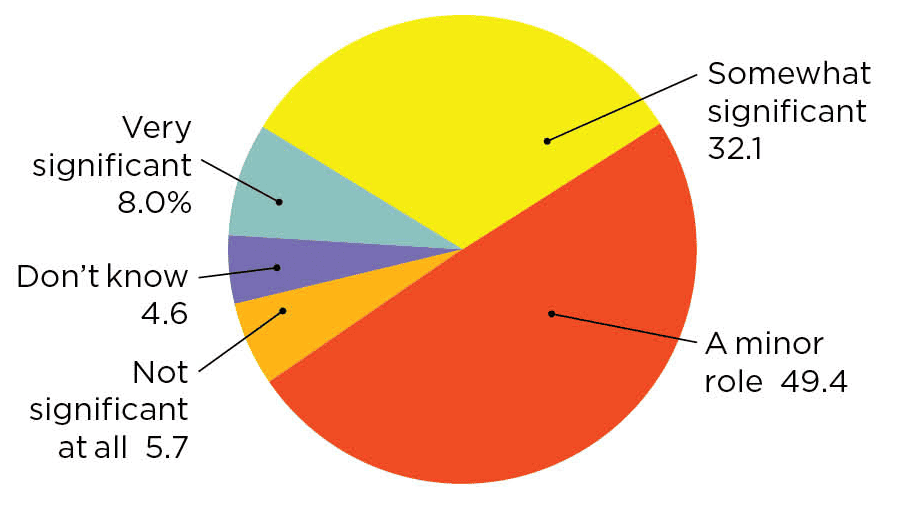

Interestingly, there is a split within the respondent base as to how significant an impact AI will have in operations, perhaps reflecting the still early stage of usage in many companies. Only 40% say that AI will be either very significant or somewhat significant, while nearly half, 49.4%, see AI as playing a minor role in the next few years (Chart 11)..

While it may be obvious that it takes a multitude of technologies to create a smart factory, the underlying message is that real power of being smart will only be realized when these technologies are integrated within the factory. That’s a whole new level of work ahead for manufacturers.

10. Strong Aspirations for a Basket of Technologies by 2026

Q: Where does your company stand in regard to the following technologies in its production operations?

11. Views on AI Significance Diverge

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations?

Section 5: M4.0 OPPORTUNITIES AND CHALLENGES

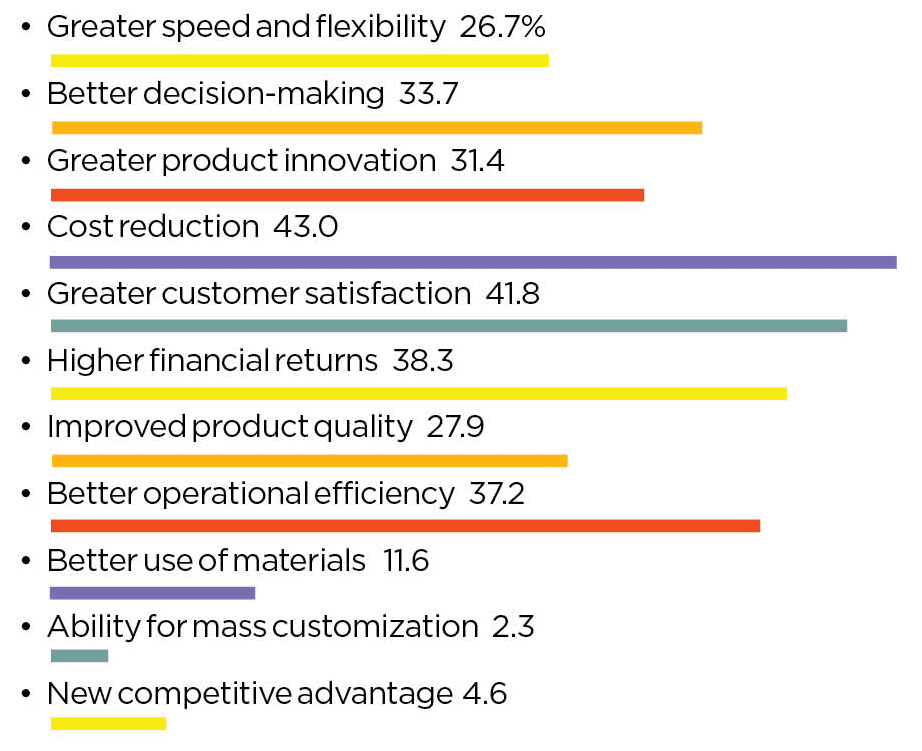

Manufacturers also expect a basketful of benefits from creating smart factories and plants. Although there is no breakout factor, cost reduction, greater customer satisfaction, and higher financial returns top the list of expected benefits.

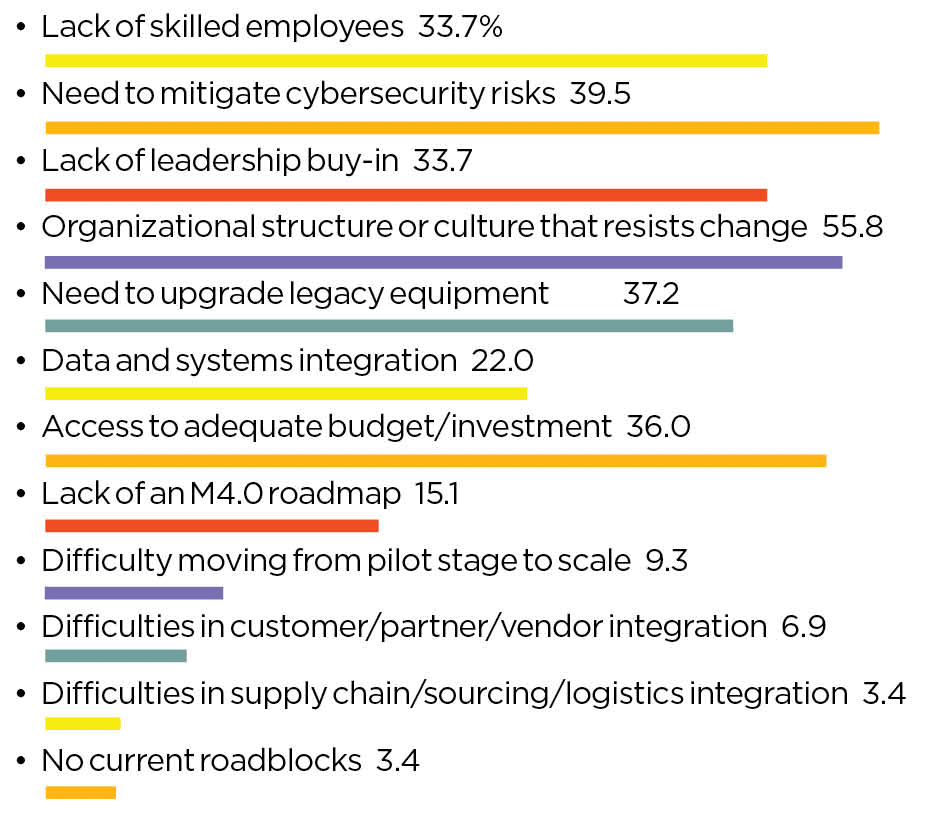

But when it comes to roadblocks in implementing a smart factory strategy, there is clearly a breakthrough factor – organizational structure or culture that resists change. More than 55% of respondents cited this factor as the primary issue in realizing their smart factory vision, considerably higher than a lack of skilled employees, cybersecurity issues, or the need to upgrade legacy equipment (Chart 12).

This may be why, when asked how well their smart factory strategies have been integrated with their company’s business strategy, very few respondents indicated that these two things were fully integrated (Chart 5).

As the famed management consultant Peter Drucker once said: “Culture eats strategy for breakfast.”

Is that glacier moving? M

12. Culture is Biggest Roadblock to Smart Factories

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top 3)

13. Cost Reduction, Customer Satisfaction Chief Desired Benefits

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top 3)

About the author:

David R. Brousell is Founder, Vice President, and Executive Director at the NAM’s Manufacturing Leadership Council.