The Industrial Metaverse May Be Closer Than You Think

Nearly 80% of manufacturing executives seem confident that the metaverse will transform aspects of manufacturing in the next five years, a new Deloitte/MLC study reveals.

![]()

TAKEAWAYS:

● Executives say that the Industrial Metaverse offers new ways to solve a variety of pressing challenges they face in the near term.

● Attracting and retaining top talent and building resilience and visibility in supply chains are top goals.

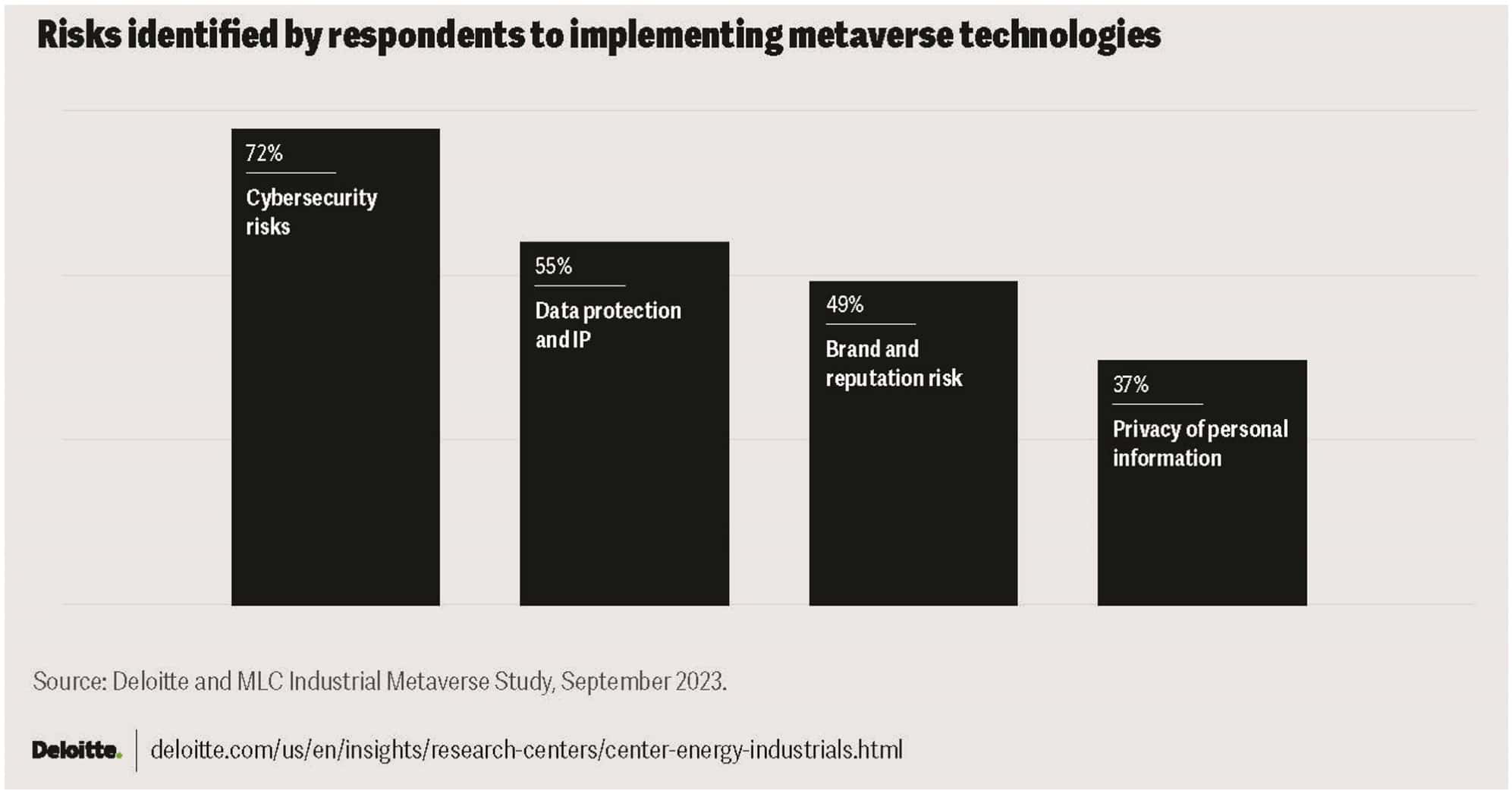

● Among the chief challenges with the Industrial Metaverse are cybersecurity, data protection and IP, brand, and safeguarding personal information.

In May 2023, Deloitte and the Manufacturing Leadership Council (MLC) embarked on a study to better understand the industrial metaverse and its applications in manufacturing. This article presents some of the key highlights from the resulting publication “Exploring the industrial metaverse” (referred to as “the study” in this article), including findings that the majority of manufacturers surveyed are already progressing on their industrial metaverse journey and are deriving benefits from even partial adoption.

A Paradigm Shift

The industrial metaverse is the convergence of individual technologies that, when used in combination, can create an immersive three-dimensional virtual or virtual/physical industrial environment. As technology evolves, the industrial metaverse will likely allow access to these immersive 3D environments from any internet-connected device, including virtual reality (VR) and augmented reality (AR) devices, as well as smartphones, tablets, laptops, and equipment, from anywhere in the world.

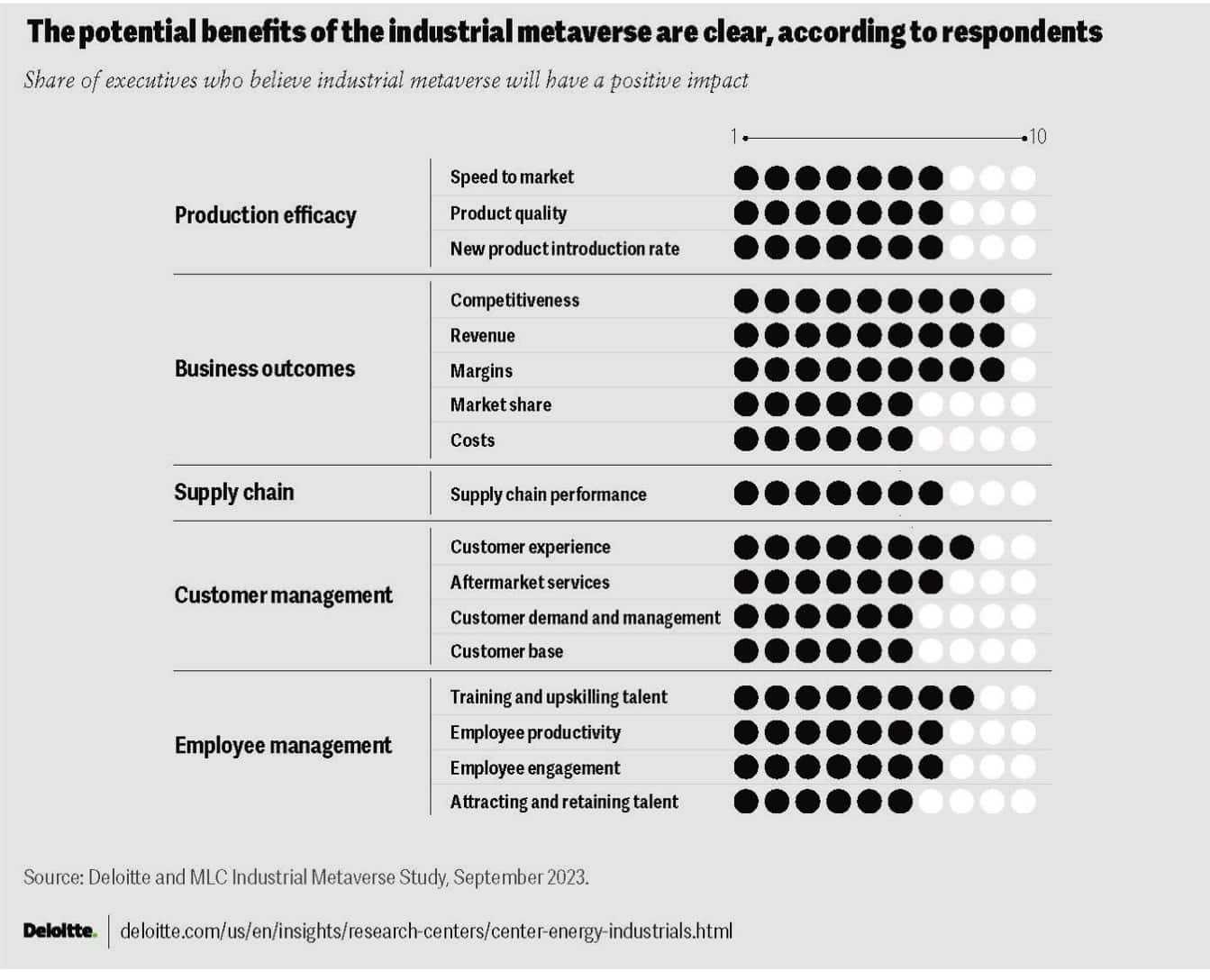

A majority of manufacturing executives surveyed[1] are bullish on the potential of the industrial metaverse in the near term. More than 70% of surveyed executives believe that in the next five years it will have a high rate of adoption in the manufacturing industry. Nearly 80% are confident that the metaverse will transform R&D, design, and innovation and enable new product strategies.[i]

Surveyed executives generally agreed that the industrial metaverse offers new ways to solve a variety of pressing challenges they face in the near term, such as attracting and retaining top talent, and building visibility and resilience into their supply chains (figure 1). They tend to view the industrial metaverse as a pathway to future value realization through improved new product introduction rates and new customer experiences and services. Respondents also expect a broad positive impact across the business and are confident that the industrial metaverse will improve key business outcomes such as competitiveness, market share, revenue, and costs, among others.

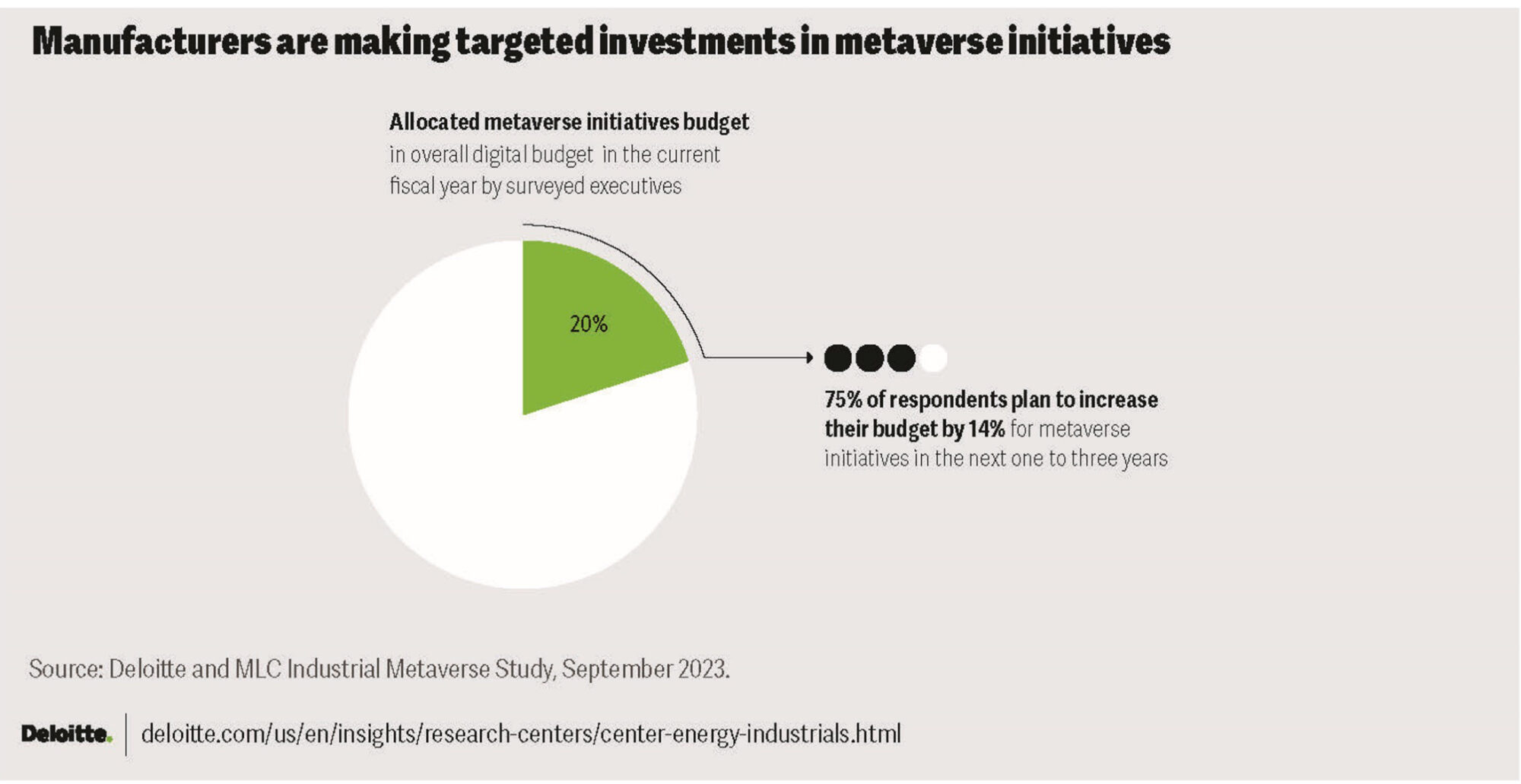

However, the study results indicate that manufacturers aren’t just betting on the future, they seem to be building it. Some respondents shared that they have already made significant investments in metaverse initiatives, and nearly three quarters plan to increase their investments over the next 1–3 years (figure 2).

Building on Smart Factory Momentum

Through digital transformation, smart factory solutions have generally allowed companies to collect important data from their processes, products, assets, and operators and perform advanced analyses to generate valuable insights, and then augment human intelligence with machine intelligence to implement significant and sustainable improvements. These advancements have resulted in greater asset efficiency, enhanced product quality, reduced costs, and increased safety and sustainability.[ii]

In a previous Deloitte paper that focused on how manufacturers can derive value from smart factory technologies,[iii] four primary ecosystems were introduced: production (quality sensing, factory asset intelligence, product development, etc.), supply chain (supply network mapping, digital warehousing, control towers, etc.), customer (aftermarket services, virtual product experiences, etc.), and talent (recruiting, training, etc.).[iv] Within the production ecosystem, a set of eight use cases were introduced, aptly named the “Great 8,” as the most prevalent use cases for smart factory technologies that manufacturers are operationalizing. Because of the scope of what the industrial metaverse can offer—connection to data-rich, immersive 3D environments from anywhere there is a broadband internet connection—its potential value stretches far beyond just the production ecosystem and the Great 8 use cases.

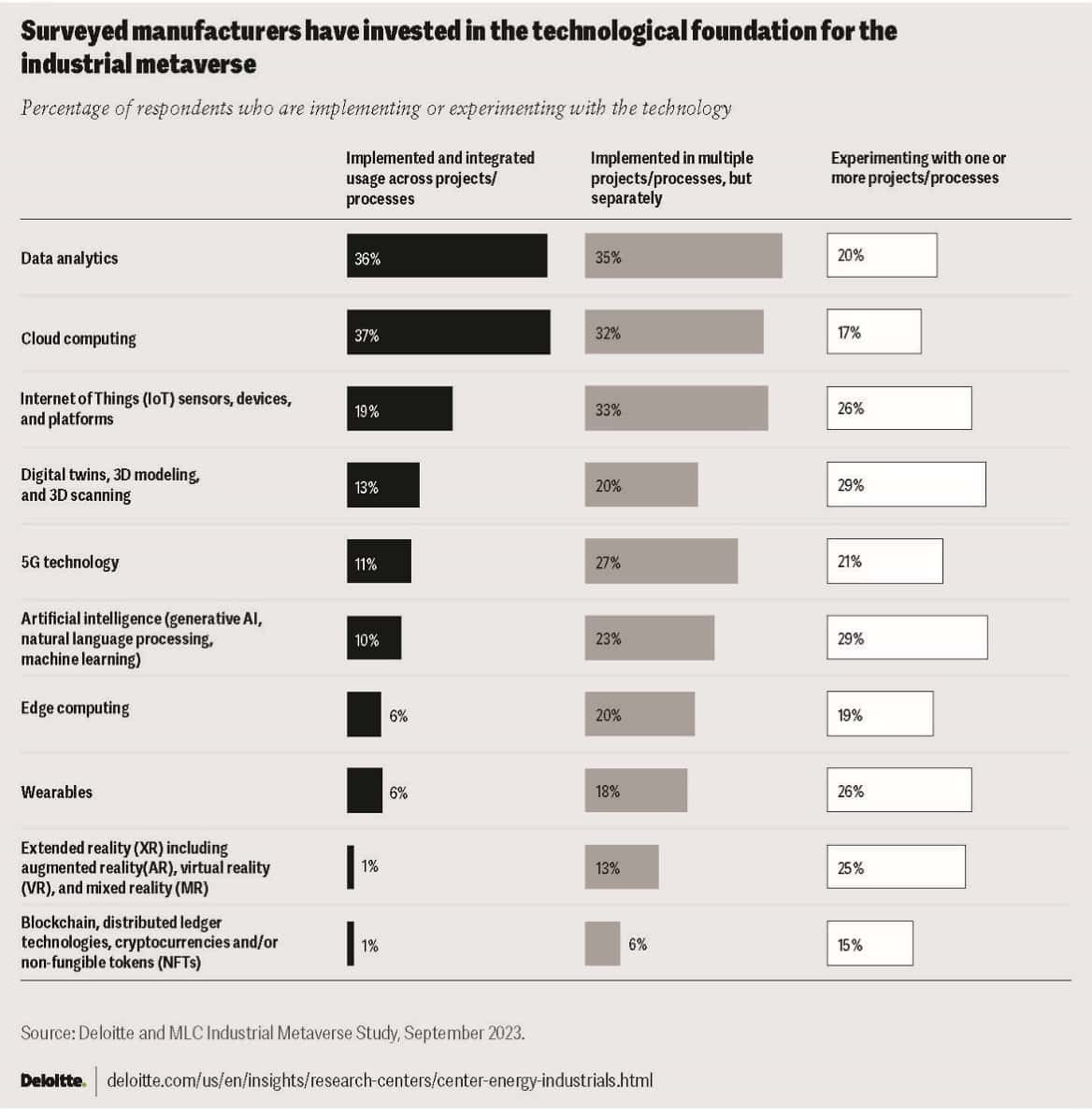

The manufacturing industry appears well-positioned for the adoption of the industrial metaverse. Given their continued focus on digital transformation and their journey toward the smart factory, the majority of companies surveyed have made significant investments and are already using the foundational technologies that power the industrial metaverse. Companies are generally either implementing technologies like data analytics, cloud computing, AI, 5G, and Internet of Things technologies across multiple projects and processes, or they are currently experimenting with one-off projects (figure 3). The same is true for digital twins, 3D modeling, and 3D scanning, which can all serve as building blocks for the immersive 3D environments of the industrial metaverse.

The study shows that not only do most manufacturers seem to have a strong technology foundation in place, many of the surveyed respondents are already combining and leveraging these technologies today to implement industrial metaverse use cases and create value.

Manufacturers Appear to be Driving Toward Adoption

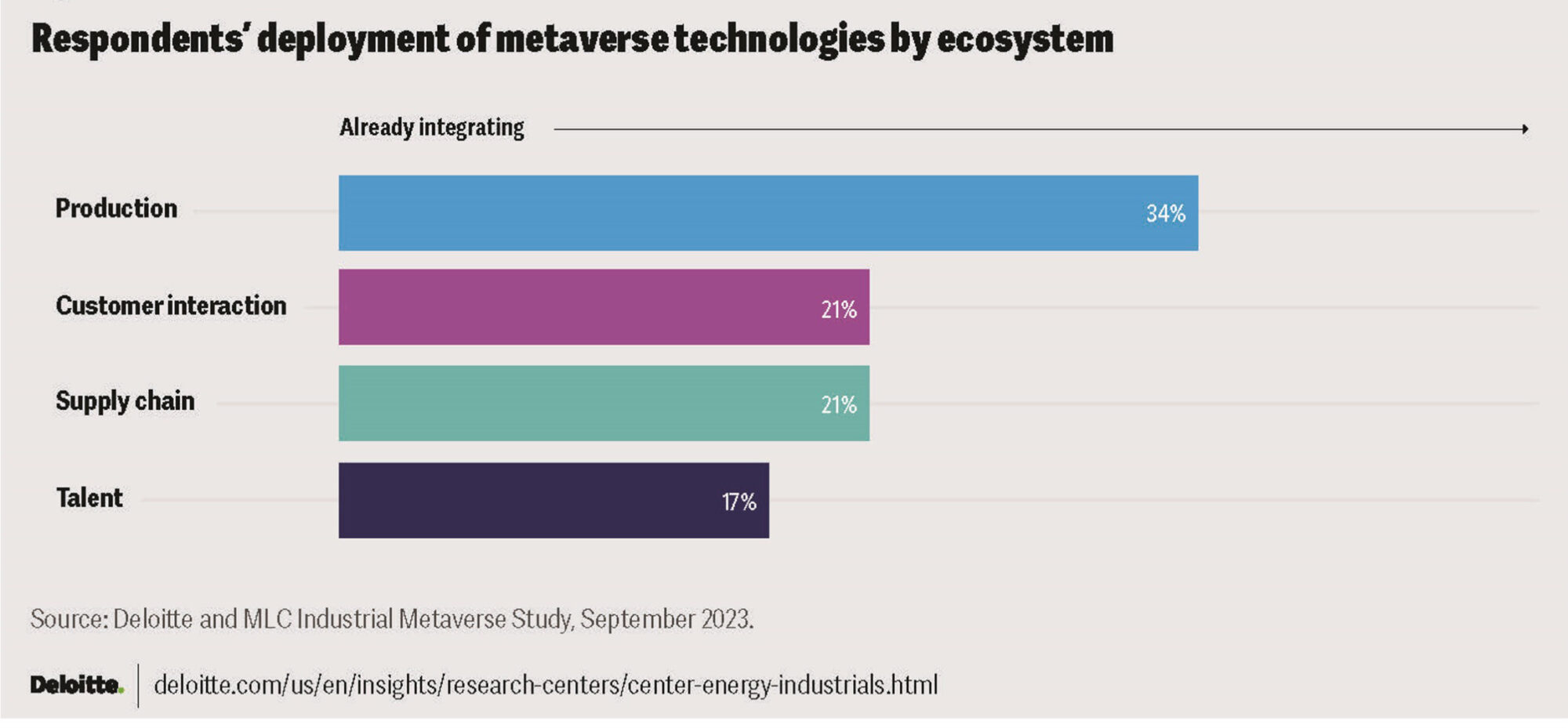

Nearly all (92%) of surveyed executives said that their company is experimenting with or implementing at least one metaverse-related use case and, on average, they are currently running more than six. Building on their smart factory efforts and leveraging the foundational technologies already in place, the production ecosystem was the most common for use case implementation, with more than one-third of respondents already integrating metaverse technologies, followed by the customer, supply chain, and talent ecosystems (figure 4).

Respondents then shared the primary use cases they are implementing using metaverse technologies. The study provides the complete details about these use cases, including their definitions, prevalence of implementation amongst surveyed respondents, the primary benefits derived, and some examples of use cases in action. Process simulation and real-time monitoring/digital twin were the two most common use cases overall, and the remaining production-focused use cases were also prevalent. Immersive training ranked third, followed by supply chain management and immersive customer experiences, demonstrating a healthy distribution of use cases across the talent, supply chain, and customer ecosystems.

The use cases and case examples that companies have reported seem to demonstrate that manufacturers are deriving value today from implementing industrial metaverse initiatives. However, they may still feel that there are challenges and risks to overcome to move toward its full adoption.

Cyber, Data Protection Are Important Risks

Cyberthreats are pervasive and can have a disastrous effect on a company if not properly mitigated. Implementing the industrial metaverse will likely bring new challenges since it derives its unique power from making proprietary 3D data about parts, products, facilities, etc., available to a variety of internal users, customers, and suppliers. It does this by allowing users to access the data through a myriad of interaction technologies over the internet, such as AR/VR devices, tablets, and phones.

One executive mentioned that because the metaverse will require significant data management; data protection, privacy, and security is a concern.[v] In fact, more than 70% of the respondents agree that cybersecurity is one of the greatest risks associated with implementing metaverse-enabling technologies (figure 5). Rounding out the top four are respondents’ concerns about protecting data and IP, brand, and personal information, all of which can be compromised in a cyberattack.

Digitalization has required manufacturers to drive collaboration between informational technology and operational technology to create an effective cybersecurity approach.[vi] Companies should develop capabilities to identify and address risk in an information technology (IT)–operational technology (OT)–interaction technology (ET) environment. One executive explained that his company is working to establish OT security capabilities and standards for how to review equipment efficiently, following the company’s IT policies, so that the operations and engineering teams can more quickly pilot and implement new equipment. This includes ET, especially since they are typically low cost (<$5,000) and don’t rise to the same level of review priority for IT as, say, a muti-million-dollar software package.[vii]

While cybersecurity risk may increase with the industrial metaverse, the study suggests that manufacturers generally believe the value it will deliver outweighs the risk, especially with the right mitigation strategies in place.

Unleashing the Power of the Industrial Metaverse

The 2023 Deloitte and MLC Industrial Metaverse study indicates that manufacturing executives seem not only confident that the industrial metaverse may hold great promise for the industry – some are already taking what’s next and transforming it into what’s now. In many cases, they are driving forward with metaverse use cases and appear to be deriving significant value across the organization. The study identifies a three-pronged approach that can be used by a broad spectrum of companies to identify, initiate, and scale industrial metaverse initiatives.

About the authors:

Paul Wellener is a Principal within the US Industrial Products & Construction practice with Deloitte Consulting LLP. He has more than three decades of experience in the industrial products and automotive sectors and has focused on helping organizations address major transformations.

John Coykendall is a vice chair, Deloitte LLP, and the leader of the US Industrial Products & Construction practice. John has more than 25 years of consulting experience focusing on global companies with highly-engineered products in the A&D, Industrial Products and Automotive industries.

Kate Hardin, executive director of Deloitte’s Research Center for Energy and Industrials, has worked in the energy industry for 25 years. She leads Deloitte’s research team covering the implications of the energy transition for the industrial, oil, gas, and power sectors.

John Morehouse is the research leader for industrial products manufacturing in the Deloitte Research Center for Energy & Industrials. He has over 25 years of experience in manufacturing-related roles in industry, academia, and government.

David R. Brousell is the founder, vice president and executive director the MLC.

[1] On behalf of Deloitte and the MLC, an independent research company conducted an online survey of over 350 senior executives in the US manufacturing industry in May 2023. The survey findings were supplemented by a series of executive interviews with technology leaders in the industry conducted in June 2023.

[i] Deloitte analysis of the Deloitte and Manufacturing Leadership Council (MLC) Industrial Metaverse survey, 2023.

[ii] Deloitte, “Smart Factory for Smart Manufacturing,” accessed August 18, 2023.

[iii] Paul Wellener et al., Accelerating smart manufacturing, Deloitte Insights, 2020, p. 6.

[iv] Ibid

[v] Insights gleaned from manufacturing executives’ interviews conducted in June 2023.

[vi] Ibid

[vii] Ibid

Scaling in the Fourth Industrial Revolution

How U.S. manufacturers can become technological front-runners.

![]()

TAKEAWAYS:

● The future of manufacturing is digital, yet despite the influx of capital investment in U.S. manufacturing recently, many U.S. manufacturers still struggle with breaking through the performance ceiling of analog operations to achieve industry-leading operational performance.

● One big barrier for U.S. advanced manufacturing is limited operational scale. For U.S. companies to compete, they need to begin with scale in mind.

● There’s much U.S. manufacturers can learn from how “Lighthouses” are deploying transformative technologies to transform their own factories into Lighthouse-level powerhouses — including network-level thinking that must be called for by CxO leaders.

Adopting and scaling digital technology in manufacturing has become increasingly urgent in today’s dynamic and highly competitive manufacturing landscape. Five years ago, the struggle for factories scaling digital lay in getting out of the gate. In 2019, 70% of manufacturing companies we surveyed named “pilot purgatory” as their biggest barrier to realizing the benefits of digital. Today, the Global Lighthouse Network — a World Economic Forum initiative co-founded with McKinsey & Company — has identified 132 global factories, representing 80 companies, that have escaped pilot purgatory and achieved industry-leading operational performance.

These plants, in industries ranging from aerospace and medical devices to food and car manufacturing, show us that at least 80 companies have figured out the “lean + digital” blueprint needed to break through the performance ceiling of analog operations. On average, site-level improvements achieved by these Lighthouses include 10-25% reductions in production cost, 20-50% increases in productivity, and 30-70% reductions in lead time. Now, these same 80 companies are well underway in scaling these benefits across their full production networks.

With such levels of savings and productivity gains on offer, and as more manufacturers see peers like those in the Global Lighthouse Network accelerating digital transformation efforts, it’s no surprise that 89% of respondents to the NAM’s 2022 transformative technologies survey expected their company’s rate of adoption of M4.0 technologies to increase over the following two years.

Five years ago, the challenge was in getting from pilot to factory. Today, the goalposts have moved: companies across the globe, including many within the Global Lighthouse Network, are focused on scaling transformative technologies from factory to network.

U.S. Manufacturers Need Advanced Manufacturing

The U.S. is experiencing an unprecedented manufacturing boom on the back of favorable domestic policy incentives and geopolitical trends. In the past year alone more than 100 new factories have been announced in the U.S., including more than 50 semiconductor and electric vehicle factories and more than 60 greenfield announcements across other clean technology verticals. Together, these represent a doubling in planned capital investments since 2022, including $166 billion in announced investment in semiconductor and electronics manufacturing. Often, policy incentives are a core part of the business case for these new factories.

“Five years ago, the challenge was in getting from pilot to factory. Today companies across the globe are focused on scaling transformative technologies from factory to network.”

Policy incentives won’t last forever. According to McKinsey analysis, for U.S. manufacturers to be competitive in the long term across new or near-shored goods, manufacturing cost reductions of 30-40% will be needed, likely through strategic deployment of advanced manufacturing technologies. And with such technology critical to the long-term competitiveness of the U.S. manufacturing base, it’s concerning that only 11 out of the 132 sites in the Global Lighthouse Network are in the U.S.—a number which underrepresents U.S. contribution to global manufacturing GDP by a factor of two.

Why Are so Few Among the Technological Elite?

First, talent — and especially digital talent — is expensive. The most talented technologists are those likely to be capable of the biggest and most transformative impact, and they are also likely to be well aware of their skills’ market value. Against big-city tech and finance companies able to offer high pay, rapid advancement, and flexible working models, manufacturers will need creative solutions. Their traditional hiring approaches, evolved in a different talent environment, often require in-person work in smaller towns — with unclear career paths because the existing base of digital roles has been so small.

Furthermore, upskilling workers for the challenges and opportunities offered by digital transformation is a muscle few manufacturers now have. Building it will be increasingly critical as more U.S. manufacturers find themselves without enough — or the right — skills to grow or digitalize. This will only be amplified by 2030, as manufacturers face:

- An increasing shortage of workers. As of January 2023, there were 803,000 openings for manufacturing roles – a number projected to swell to more than 2 million + by 2030.

- A rapid loss of industry knowledge. Over a quarter of the U.S. manufacturing labor base is composed of workers over the age of 55, and attrition rates remain as high as 40%.

- An accelerating skills shift. Digital manufacturing requires a different set of skills than analog approaches. According to analysis by the McKinsey Global Institute, by 2030 the U.S. manufacturing sector will require 259,000 more engineers, but 479,000 fewer production workers—resulting in transitions for around 1 million workers, or roughly 8% of the workforce.

Finally, the deployment of U.S. advanced manufacturing is limited by operational scale. US factories tend to be smaller, both in physical and workforce size, than at comparable sites in China, for example, with far fewer employees per U.S. factory. Digitalizing a facility carries several one-time costs that are incurred whether a facility is large or small, such as setting up cloud infrastructure. In the U.S., there are smaller economies of scale to overcome these fixed costs of site-specific digitalization programs — it is less economical to embed the tech teams needed to support transformation at smaller, more numerous sites.

“We can learn from how Lighthouses are deploying transformative technologies, which primarily focus on business needs.”

Together, these points help to explain why the U.S. has comparatively few manufacturing Lighthouses. At the same time, we can learn from how Lighthouses are deploying transformative technologies, which primarily focus on business needs such as productivity via workforce augmentation, matrix manufacturing via cross-site scheduling, and throughput maximization via digital twins and predictive maintenance.

Focus on Network-Level Strategy

If scale is part of the challenge for transformative technologies in U.S. manufacturing, then the solution must be to start with scale in mind. Siemens Digital Industries provides a good example of the possibilities. Its two Lighthouse factories serve as anchors for a network-level digital implementation strategy. Like every other factory in the Siemens network, each of these two sites maintains its own strategic posture for digital innovation. That allows some sites to prioritize factory operations improvements, for example, while others can focus on end-to-end connectivity.

Yet at the same time, common resources mean that use cases, once proven, can be rapidly deployed across the network. All sites use a modular reference architecture that lets use cases plug in easily, with central digital teams providing expertise for local implementation. This approach to scale can make the economics more palatable than the one-factory-at-a-time transformation model — which in the U.S. too often simply can’t be done.

A Role for Leaders

CEOs and their CXO colleagues are the ones who can elevate the vision to network levels, rather than dwelling on site-specific plans, delivering real-world benefits of better customer experiences, lower costs, and accelerated innovation. And they have the playbooks to help them do it, built from evidence, data, and analysis from hundreds of digital transformations. They are the ones to get the board on board with such long-term, capital-intensive journeys, and to dedicate time and resources to making the necessary talent and capability upgrades.

“CEOs and their CXO colleagues are the ones who can elevate the vision to network levels, rather than dwelling on site-specific plans.”

- Invest in capabilities with a longer time horizon. Our analysis finds that the best-performing digital manufacturing sites are those that “go slow to scale fast,” spending a year or two strategically building a data and technology foundation for deploying use cases and training analytics models. Once established, some Lighthouses deploy a dozen or more use cases in weeks, not months or years. Four years into its digital transformation, one Lighthouse company deployed a standard operating procedures (SOP)-interfacing chatbot for workers in just 1.5 weeks.

- Cultivate a tech-forward workspace for eager technologists. Attracting and keeping the right profiles will require innovative workspace models that exemplify the tech-forward future of work — providing fast-paced, problem-solving heavy environments with significant real-world impact and clear pathways to learn and advance. Because this talent can be expensive, the economics may work only by keeping network scale in mind.

- Build scale into the business case from day one. Though most use cases will need to be piloted within a specific site, this is just the first step in a plan to achieve end-to-end value. Such solutions are most effective when they address critical bottlenecks across the production network, such as cross-site production scheduling for matrix manufacturing. Likewise, factory-specific use cases, such as vision systems, can be designed to address business needs that a majority of the production network also faces. Think too small, and the ROI dwindles.

The future of manufacturing is digital. To compete, U.S. manufacturers can start with scale in mind. This requires network-level thinking that must be called for by CxO leaders. M

About the authors:

Rahul Shahani co-leads McKinsey’s Industry 4.0 efforts in North America including the Innovation & Learning Centers and focuses on digital manufacturing transformation design and execution. He is a partner in McKinsey’s Operations Practice, based in New York.

Dan Swan co-leads McKinsey’s Operations Practice globally, and helps manufacturing and service companies transform their operations performance and capabilities.

Henry Bristol focuses on Industry 4.0 technology adoption strategies for industrials, electronics, and new energy manufacturers. He is a Fellow with the World Economic Forum and an Engagement Manager in McKinsey’s Operations practice.

How a Private Equity Approach Can Drive Auto Suppliers’ EV Transition

By adopting a PE lens, companies can transition more smoothly from legacy internal combustion engine business to the EV market.

![]()

TAKEAWAYS:

● The $1.9 trillion global auto supply sector will experience a shakeout in the changeover to EVs, and the slowest movers risk losing opportunities or bankruptcy.

● Companies that have hesitated to initiate change can benefit by assessing future options using the relentless, enterprise-value based approach of private equity firms.

● Lessons from early movers highlight the value of planning the funding, rigorous execution and governance, and workforce transformation.

The global automotive industry is undergoing existential disruption as the world market embraces electric vehicles (EV) over internal combustion vehicles and hybrids. At this point—in the early stages of the transition and with a long way still to go—some challenges facing the diverse auto parts supplier industry are becoming clearer; however, many companies are still figuring out how quickly to embrace those changes.

The market transition to EVs is gaining momentum due to advances in technologies such as batteries and charging stations, and growing buyer interest thanks to the success of Tesla and other electric models. The U.S. and other governments are doubling down on commitments to transition to EVs. Recently proposed federal emissions limits in the U.S. would effectively require two-thirds of cars sold in the country to be electric by 2032; California will require that all new vehicles sold in the state after 2035 be zero-emission vehicles.

Parts suppliers—from gas tanks to fuel injectors—for traditional cars are already seeing their market shrink, and the decline will only worsen. This $1.9 trillion industry will see a painful slowing of growth in coming years as internal combustion engine (ICE)-based product lines are phased out. About one quarter of profits currently generated from legacy ICE components will be the most adversely affected, resulting in a 50 percent decline from current levels by 2030. For some suppliers, the market will eventually resemble a game of musical chairs, with fewer and fewer safe economic places to land—and the slowest movers losing the game.

Segments of the ICE market will remain, such as parts for existing vehicles, and suppliers can continue to earn some revenue in this area long after production of new ICE models is phased out. Also, commercial vehicles have lagged passenger cars in the EV transition, so far, and are likely to offer another “long tail” of continuing opportunity for parts makers.

“About one quarter of profits currently generated from legacy ICE components will be the most adversely affected, resulting in a 50 percent decline from current levels by 2030.”

The impacts are hitting auto suppliers in different ways and at different velocities, depending on the parts they make and the size of the company. For example, many larger makers of powertrains and other ICE components, whose production lines require long development lead times to transition, have embraced the need to change. They are developing transformation strategies and making operational changes, announcing new manufacturing strategies, new partnerships, and new product lines. Public companies also benefit from the involvement of boards of directors and stockholders that push them to adopt transformation strategies earlier while balancing risks.

In contrast, small, medium and privately held companies, with traditional, risk-averse management styles and fewer resources tend to lag. Companies that continue to delay adoption of an operational transition strategy may soon find themselves at risk.

Julie Fream, president and CEO of the Motor & Equipment Manufacturers Association – Original Equipment Suppliers (MEMA), says that one of the biggest challenges companies face is estimating when the growing market for EV products will overtake the ICE components they are replacing. This uncertainty is causing many executives to hesitate as they plan their company’s operational transition from ICE to EV.

“Suppliers know they need to be able to do both, but they are asking, ‘How do I know the volumes?’” Fream says. “How do they manage the crossover point, knowing that you can’t accurately predict at this point where the two lines will cross—where EV becomes dominant, and ICE becomes a secondary product line. That’s the question they are all asking.”

Companies that invest in EV too early could end up financially overextended, with excess capacity and a market that is not ready for their new products. Late arrivals could lose opportunities completely if faster competitors beat them to the punch.

Companies seeking ways to exit ICE businesses also face challenges as certain, carved-out legacy ICE assets will become steadily less attractive to buyers. Without successful consolidation or divestiture, many will be forced to shut down, particularly if cost cuts and efficiency improvements cannot keep pace with commercial declines. At the same time, suppliers wishing to embrace new technologies must invest heavily in new product and service innovations targeted at EVs. Often, these competing priorities absorb cash while also preventing the bold action that is needed in today’s market.

The Private Equity Mindset as Transformation Catalyst

Many auto suppliers, especially those that are small or mid-sized and often privately owned, have relied successfully on a traditional management approach of incremental improvement and risk management. This approach, however, is ill-suited for the current market upheaval. Tomorrow’s winners will innovate and reinvent their whole business, embracing their initial entrepreneurial spirit.

Fortunately, a ready model for bold decision-making exists that can serve as a model for the aggressive approach these companies will require—that of the private equity (PE) investor. Two aspects of the PE mindset stand out as the essential, outside-investor viewpoints that many ICE suppliers urgently need:

- The ability to make bold decisions, without attachment to unprofitable “sacred cows”; and

- A relentless focus on enterprise value.

For companies accustomed to incremental change that need to become unstuck, the PE lens can be a catalyst for the swift cultural makeover needed to get moving.

“The PE mindset is something many suppliers should consider,” says Fream. “There’s a lot of money on the sidelines right now that could eventually come in. This would create some opportunities if you accurately analyze your business and understand what needs to be done.”

“For companies accustomed to incremental change that need to become unstuck, the PE lens can be a catalyst for the swift cultural makeover needed to get moving.”

This is not easy, she notes: “Suppliers need the skill set to assess what’s happening in the marketplace. The PE firm is ultimately trying to drive the company to be more focused on the marketplace. Generally, they don’t tolerate anything outside of that. But this can be very difficult for some suppliers, especially smaller, privately-held companies.”

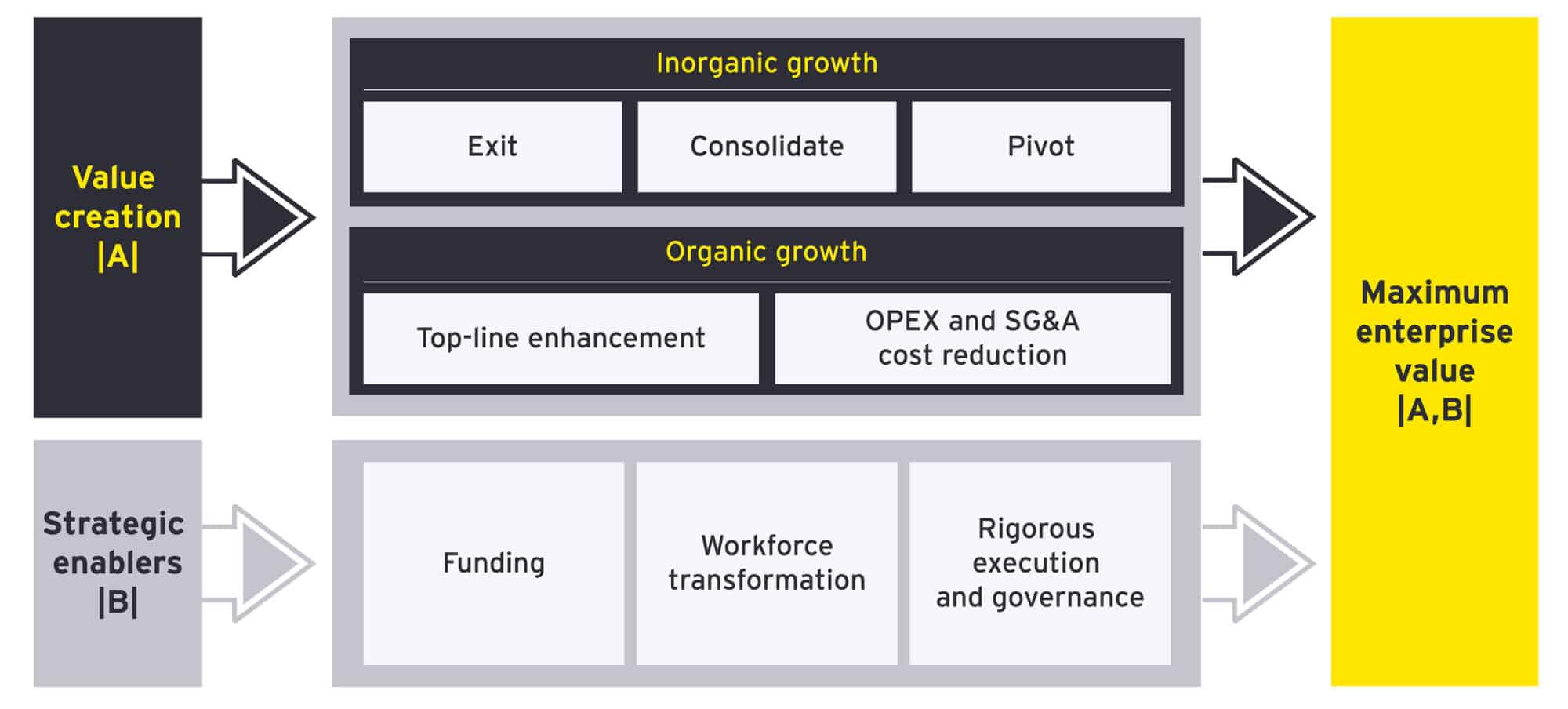

Typically, PE has a variety of strategic approaches to generate profits from companies in either fading industries or startups in new technology fields. PE investors can improve enterprise value and prepare an asset for profitable sale through organic upsides—topline growth and bottom-line improvements—as well as inorganically, through a potential portfolio play (Figure 1).

Figure 1: Private equity value creation approach

Leadership can use the PE agenda to conduct a data-based assessment of how their business creates value today and its potential future role in the developing EV ecosystem. Based on this deeper understanding, leaders can adopt and implement a transformation strategy that aims to maximize enterprise value, as highlighted in the 2022 EY article “How auto suppliers can navigate EV technology disruption in four steps.”

Identify the Appropriate Operational Strategy Using the PE Approach

Not all traditional product components are expected to decline in the near term. Many product lines can be suitable candidates to pivot to other markets, and some can continue as sources for income that can be invested in new EV product development. Strategic approaches for how companies are managing their existing ICE businesses can be grouped in three broad categories:

- Exit (cash out and focus): One clear option is for suppliers to wind down or sell their ICE products businesses to a buyer that can squeeze value from them, for longer, than the original owners can. The spin-off strategy can reduce exposure to the declining demand for ICE products and can raise capital for reinvestment in new market opportunities.

- Consolidate (double down): Suppliers can prepare for the coming shakeout by consolidating existing ICE-only businesses to create synergies and scale so they can continue to derive value from their operations for as long as possible, with the option to continue to operate them alongside new EV businesses.

- Pivot (parallel pursuit): Companies can wind down their ICE businesses according to a clear step-down plan, while pivoting product lines to new EV products. This may require massive investment in R&D, innovation, and digitization to develop new EV products and services. It could include acquiring EV startups or niche players to expand product portfolios and acquire new skills or technologies.

The Transformation Journey So Far: Signs of Success and Warnings

Quite a few original equipment (OE) suppliers have identified enterprise EV transformation strategies and begun to execute them. Based on these OE suppliers’ track records, other suppliers can ascertain the challenges of redesigning value chains or operating models.

Example: A Supplier Divests ICE Divisions and Invests the Proceeds in EV Partnerships

A German powertrain company with ICE and EV products that was spun off in 2021 is following a two-part strategy of divesting its remaining internal combustion divisions to help fund its growing EV business, which is focused on EV innovation and growth through investments and partnerships.

“Companies must take care to minimize the impact on employees. . . . Employees should have the option of transitioning to new business roles, where possible. Companies should develop and activate a clear engagement strategy for unions early in the process.”

The company is selling its catalyst and filters operation and intends to divest its ICE division, which has been profitable since 2021 after years of losses. Meanwhile, it is bolstering its EV business through partnerships with automakers to jointly develop power electronics and electronics companies for access to semiconductors. The company’s electronic mobility business has significant orders from Hyundai and is expected to break even in 2024.

Enablers of Transformation: Risks and Opportunities

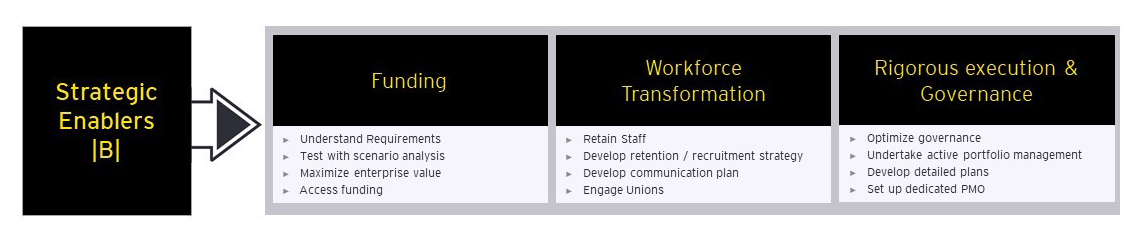

Once organizations have determined the strategic way forward, they will face significant challenges in executing the agreed-upon roadmap. The experiences of companies that are already making progress, coupled with recent EY work with automotive supplier clients, can make it easier to identify which strategic enablers companies will need to carry out the transition, as well as useful observations and lessons (Figure 2).

Figure 2: Strategic enablers

Rigorous Execution and Governance

Companies will need to review and adjust their governance so they can manage a rapidly growing, subscale new business and another business in slow decline. Many larger companies are opting to carve out their legacy EV business into a separate division.

Cash flow must be tightly monitored as, given the likely scale of costs, budgeting can be extremely sensitive to small changes in assumptions. Companies should implement robust short- and medium-term forecasting processes during the transition period where cash flow may be tight.

Active portfolio management is equally critical, so that only products with profit potential continue to receive investment. Companies should tier their governance to match the investment and uncertainty levels and to ensure they maintain appropriate controls. They should also take care to avoid excessive reporting and bureaucracy, which can steal oxygen from innovative new ventures.

Workforce Transformation

Staff who will be transferred to new products will need retraining. In cases where companies require new skills that are hard to find within the sector, they can recruit from adjacent industries where employees have transferable skills. In addition, companies will require creative solutions to retain key staff from the legacy business, for as long as is required, to ensure a smooth transition.

Companies must take care to minimize the impact on employees. Open and transparent communication and change management are important, as communication vacuums tend to be swiftly filled with rumors and uncertainty and that can raise stress levels and harm operations. Employees should have the option of transitioning to new business roles, where possible. Companies should develop and activate a clear engagement strategy for unions early in the process.

Funding

Once a company sets its strategy, it needs to fund it, and change can be costly. New products will require expensive capital equipment purchases, and the new business is likely to lose money at first. Companies will need to write down legacy machinery and obsolete stock and take special care to avoid large customer and supplier claims.

Cost control will also be critical during this period, particularly given the long timeframes involved. It is important that companies understand the combined costs of legacy products being ramped down and new products being ramped up. They should do sensitivity analysis to stress-test this requirement, identify budgets, and fund them appropriately. Companies should establish and implement their strategy soon to avoid facing simultaneous closure and setup costs. M

About the authors:

Joern Buss is an EY-Parthenon Partner, Advanced Manufacturing and Mobility, Ernst & Young LLP. Focused on strategic growth, product technology, transformation, and turnaround, he supports manufacturing and mobility companies, alongside private equity and investors.

Jon Slatkin is an EY-Parthenon Partner, Turnaround and Restructuring Strategy, Ernst & Young LLP. He is an Ernst & Young – United Kingdom Strategy and Transactions Partner.

James Nicholson is an EY-Parthenon Partner, Advanced Manufacturing & Mobility, Ernst & Young LLP. He is one of the leaders in the EY UK&I Strategy practice. He helps clients plot successful paths to growth, adopt new business models and evolve their core capabilities and global footprints.

Kevin Rebbereh is Director, Automotive Strategy, EY-Parthenon GmbH. He is a director with EY-Parthenon in Hamburg, Germany and is in the leadership team of the automotive strategy practice in Europe West.

Lloyd McRitchie is EY-Parthenon Partner, Turnaround and Restructuring Strategy, Ernst & Young LLP. He is a partner on the Turnaround and Restructuring Strategy team.

Dialogue: M4.0 Leadership from a Digital Champion

Johnson & Johnson’s Bart Talloen shares his thoughts on meeting and exceeding customer expectations, supply chain as a competitive differentiator, and why manufacturing leaders need to focus on curiosity, continuous learning, and shaping the ecosystem of the future.

Recently named the Manufacturing Leadership Awards’ Manufacturing Leader of the Year, Bart Talloen Vice President, Operational Services and Standards for Johnson & Johnson, has been instrumental in leading an innovation-driven shift in J&J’s supply chain. He has had a significant impact on J&J’s standing as a global leader, as demonstrated by the company’s record 11 lighthouse designations from the World Economic Forum.

In this interview he discusses how technology plays an essential role in exceeding customer expectations, the importance of upskilling and training the leaders of the future, and why it’s necessary for every leader to build and leverage a diverse, far-reaching network of internal and external collaborators.

Q: You have been with Johnson & Johnson for 27 years. How has your role evolved during your career there?

A: For 19 years I had different operational supply chain roles with increasing responsibility in our J&J pharmaceutical, over the counter and consumer businesses. This included engineering, planning, manufacturing operations and general end-to-end supply chain management in Europe, Asia, and North America. I have also acquired and divested business operations, built five and closed three manufacturing facilities and was also responsible for the supply chain during the successful execution of a consent decree for McNeil Consumer Healthcare, J&J’s U.S. over-the-counter business.

For the past eight years I have been responsible for J&J supply chain strategy, driving innovation and overseeing large-scale transformation programs encompassing all three of J&J’s business sectors. The overarching evolution of our supply chain is going from a focus on cost and operational excellence to making supply chain a business enabler and competitive advantage. My role has evolved accordingly, from initially building and deploying supply chain strategies that were centered around foundational improvement capabilities such as lean, Six Sigma, and operating systems to bolder strategies built on major capability transformation programs. This includes technology, go-to-market models and channels for access to care, such as supporting outpatient clinic-based settings and telemedicine, as well as customer centricity and personalization.

In the last couple of years I have also been focused on technology and digital innovation, next-generation customer enablement solutions to drive differentiating experiences and outcomes as well as the whole value chain from suppliers to customers.

Q: What most excites you about the role you are in now?

A: It is really about the difference we make as supply chain for our customers, which is twofold:

One is that we are building and deploying cutting edge customer strategies and solutions that transform the experiences and outcomes for the customers and patients that we serve every day. One example is a solution called Advanced Case Management, which uses case schedules and patient data to manage inventory at the point of consumption – ensuring we have the right orthopedic implants for the right patient at exactly the right time. Another example is an autonomous order fulfilment and inventory management system deployed in hospitals, which is supported by an AI engine that suggests operating room improvement opportunities, simplifies and automates healthcare practitioner work, and helps reduce inventory and logistics costs. Connecting that to our supply chain planning enables real-time alignment of the supply to the demand from hospitals.

Second, risks are no longer an isolated event, they are interconnected. That is why we are moving toward multidimensional and proactive approaches to resilience. We are making significant advancements in supply chain resilience, enabling us to always provide our customers with the products and solutions they need whenever, wherever and however they are needed and expected, through whatever disruptions may happen. It strengthens our ability to consistently deliver products, providing confidence and assurance through times of uncertainty. And that is what our customers expect.

“We are strengthening our ability to consistently deliver products, providing confidence and assurance through times of uncertainty.”

Our proactive resilience capability is centered around a resilience engine that leverages data science and analytics for multi-dimensional risk evaluation. Combined with network and product-specific data, it enables improved velocity and quality of trade-off decisions at supply chain, product and network levels. This results in proactive risk identification and mitigation while ensuring continuity of our product supply.

Q: Beyond innovation, what are some of the other main supply chain initiatives underway at J&J?

A: Currently there is a strategic focus on customer anticipation, resilience, and end-to-end supply chain orchestration. This translates into new supply chain capabilities we’ve been building and deploying such as advanced customer enablement solutions, smart operations with the adoption of advanced I4.0 technology innovation, end-to-end supply chain control towers to give us real-time visibility and tracking across the supply chain, and digital connectivity with our customers and suppliers. There is also a focus on proactive supply chain resilience and how we leverage digital capabilities.

At J&J, we’re also heavily investing in the development of our workforce. Some examples: We are enabling a digitally connected and augmented workforce program, developed with a worker-centric mindset, built around four capability components: worker assistive applications, immersive and wearable solutions, intelligent automation, and hybrid ERP + cloud-based technology platforms.

Also, we’re upskilling our people using a high-touch model of leadership training that includes our Global Operations Leadership Development program, our Compass Executive Quality Leadership Development program, our Plant Leader Development Program, our STAR programs to provide action-learning experiences for emerging supply chain leaders, and an entry-level program for recent graduates. We extended the program to include a well-being component. Last year alone, 600 new participants were enrolled in leadership development programs, with 30 participants in GOLD and more than 25,000 participants in other training programs.

Additionally, we’re partnering across Johnson & Johnson with schools, universities, and external partners through sponsorship of our Women in STEM program, which aims to ignite the power of women inside and outside of our company. By 2025, we want half of our global management positions to be occupied by women; we have already achieved this goal in Europe, the Middle East, Africa, and Latin America and are on track for the same in other markets.

Q: J&J is the recipient of 11 lighthouse designations from the World Economic Forum for advanced manufacturing, the most of any company in the world. What are the essential components to becoming this type of global leader?

A: First, it is important to have a digital strategy, driven from the top and supported by senior management, with laser-sharp focus on execution and implementation driving tangible business impact. This strategy needs to be driven by the customer and business needs, not based on what I call a “tech push,” meaning you are just pushing deployment of technology solutions and tools into the business vs. pulling tech solutions that help address customer and business needs or pain points.

“It is important to have a digital strategy with a laser-sharp focus on execution and implementation driving tangible business impact.”

Second, data availability and visibility are critical, but for many companies still a challenge given the complexity of operational infrastructure with a lot of legacy systems that don’t talk to each other. We have a thoughtful data strategy, IoT systems and a defined digital stack – a combination of digital products and platforms that help us scale digital solutions faster. We have created a data lake where the data from different operational systems is ingested and made available for the digital stack and ML/AI algorithms and apps to “work their magic.” This infrastructure has been very helpful and a critical component of our digital strategy and its successful implementation.

Third, an important enabler and differentiator is leveraging external partnerships to complement the internal J&J capabilities. Over the past few years, we have established a broad external collaboration ecosystem with academia, consortia, startups, other industry companies, suppliers, etc. We are leveraging these ecosystems to advance capabilities in tech innovation, influence the global Industry 4.0 agenda and drive tech progress across industries. These partnerships were built and came to fruition in our innovation hubs, which are based in global tech hotspots, and technology capability centers that are focused on specific Industry 4.0 technologies such as 3D printing, smart sensors and vision systems, advanced materials, advanced robotics and so on.

Q: Additionally, you were just named the 2023 Manufacturing Leader of the Year at this year’s Manufacturing Leadership Awards Gala. What are the leadership skills and attributes you believe to be most important in the era of Manufacturing 4.0?

A: It is of course important that leaders have a good understanding of Manufacturing 4.0 technologies, how they can be applied and the value and impact they can bring for your business. But in my opinion, there are three leadership characteristics, and differentiators, that are the most important:

First, supply chain leaders of the future will be more like “ecosystem orchestrators” vs. “managing a supply chain in a particular company.” To do this, you first need an understanding of the customers and markets you serve – an outside-in perspective that you can use to shape your strategy. Additionally, it’s about realizing that no one person or company can or should do it alone. If I take maintaining business continuity as an example, it takes a network of suppliers, governmental agencies, companies, third-party logistics providers and so on all working together. It’s about building those networks, internally and externally, and doing it with a focus on where the expectations of your customers are evolving.

Second, it is also critical for leaders to be creative and curious. Seek continuous learning and think about new ways to work together across functions and reach out to business partners to learn more about how you can work together.

“Supply chain leaders of the future will be more like “ecosystem orchestrators” vs. “managing a supply chain in a particular company.””

Third, keep seeking connections not just within your organization, but externally as well. We have to be intentional about cultivating professional relationships. This could include attending forums and conferences, joining industry associations and consortia, or creating collaborations with other companies inside or outside of your sector and/or suppliers. All these relationships and connections invite diverse perspectives and encourage thought sharing. For J&J, this offers better insight into what patients and customers want and need from us, but also provides insight into other industries and how they’re enhancing operations, innovating and engaging with their customers and deploying advanced tech solutions and innovation. It is important to approach collaboration broadly and holistically to get the most out of it – and it is dynamic; you are never done.

Q: What do you feel is the most important lesson you’ve learned in your career so far?

A: Phenomenal things can be achieved via technology, but in the end it is all about the people. We can have the right process, the right technology and systems, but it is the people that are the differentiator. You need the right leadership – bosses that trust and believe in you. You need the right employees to get the job done, and you need the right peers and collaborators because you cannot do it on your own. I have seen this play out in my career time and time again.

Q: What do you foresee as manufacturing’s greatest challenges and opportunities in the years ahead?

A: I believe there will be three great challenges:

One, making manufacturing an interesting place to work and a magnet for current and future talent will be key. So, we need to continue to enable and develop our workforce with regards to future capabilities and skills, talent acquisition, retention, employee engagement and development, culture, and so on. In the current dynamic environment and competitive labor market this will need strong attention and will be a critical success factor for manufacturers.

Two, having a robust data strategy, data availability and visibility isn’t easy for most companies given their complex system infrastructures and legacy systems. But it is critical to crack this nut to be successful in the digital era.

Three, supply chain resilience. The unpredictable and volatile world of today requires that we evolve from the traditional supply chain risk management and isolated risk approach to a holistic multi-dimensional and pro-active resilience approach.

The greatest opportunity I see is for manufacturing leaders to become end-to-end orchestrators vs. just leading the operations within the four walls. The differentiator to accelerate your value creation and impact is through holistic collaboration and by leveraging an ecosystem of partners. Manufacturing leaders need to own, shape, and drive this ecosystem. M

![]()

FACT FILE: Johnson & Johnson

Headquarters: New Brunswick, New Jersey

Industry Sector: Diversified healthcare products

Annual Revenue (2022): $94.9 billion

Employees (2022): 155,800

Production: 97 manufacturing sites worldwide

EXECUTIVE PROFILE: Bart Talloen

Title: Vice President, Operational Services and Standards for Johnson & Johnson Services Inc.

Education: Katholieke Universiteit Leuven, Belgium; B.S. and M.B.A.

Previous Roles:

– Vice President, Strategy Innovation and Deployment, J&J Supply Chain

– Vice President, Supply Chain North America OTC, J&J Consumer

– Vice President, Supply Chain WW Nutritionals, NA OTC, Franchise Strategic Operations, J&J Consumer

– Vice President Consumer Supply Chain Asia Pacific, J&J Consumer

About the author:

Penelope Brown is Senior Content Director of the NAM’s Manufacturing Leadership Council.

AI’s Outcomes Rely On Its Rollout

If done right, AI will revolutionize everything from safety and quality to efficiency and maintenance

![]()

TAKEAWAYS:

● AI represents a unique opportunity to improve the efficiency of production, especially when it comes to preventative maintenance.

● Integrating AI into production can increase cyber risk by creating new potential access points for bad actors.

● More extensive training is required for AI to accomplish complex tasks, while repetitive tasks require less training.

For centuries, manufacturers have faced the challenge of addressing safety hazards in factories while boosting efficiency and controlling costs. Now, many manufacturers are learning that artificial intelligence (AI) can help them make new strides when addressing protracted worker safety and efficiency challenges. Consequently, it is no surprise that 36% of manufacturers say they will pursue Industry 4.0 investments according to the 2023 BDO Manufacturing CFO Outlook Survey. As more manufacturers explore AI’s future and how it can help them improve safety and efficiency, it is critical that they set themselves up for success by securing employee buy-in and preparing factory infrastructure to take full advantage of AI-based systems.

Today, much of the public has become aware of generative AI, such as OpenAI’s ChatGPT, with its ability to quickly answer complex problems with written prompts. Generative AI is exciting to the general public, but many plant managers are passionate about AI systems that are specifically designed to operate in a manufacturing setting. Rather than only using written prompts, AI systems used by manufacturers leverage inputs from computer vision, lasers, and other sensors to predict when a safety issue may occur, which robot caused a manufacturing defect, and how machines should be calibrated to minimize downtime.

Leveraging Technology to Combat Safety Hazards

Despite decades of regulations and improved protocols, safety issues persist in modern manufacturing. Updated safety codes and maintenance plans cannot always prevent worker injuries that result from negligence or unpredictable hazards in a manufacturing facility. While strong employee training programs remain one of the best ways manufacturers can improve safety in settings from chemical plants to automobile factories, even the most dedicated employees are not constantly vigilant to workplace dangers. This is why many manufacturers are investing in AI-powered safety systems, which can predict when and where a safety violation could happen, allowing plant managers, and sometimes the AI itself, to remedy the situation before it becomes irreparable.

However, to work successfully with AI, workers need to be trained to interact with these new systems. The latest advancements in augmented reality (AR) and virtual reality (VR) technologies enable companies to make training programs for employees who interact with AI-powered safety systems even more effective, further empowering workers to keep themselves safe. AR or VR simulations can give employees a sense of what it is like to work with potentially dangerous machinery in preparation for operating the real equipment. Workers can also practice carrying out the necessary safety procedures before entering a secure area or shutting down a robot in need of repairs on the factory line. These AR- or VR-enabled training exercises can reduce the likelihood of mistakes, which could result in worker injury or damage to machinery.

“Many manufacturers are investing in AI-powered safety systems, which can predict when and where a safety violation could happen”

While AR and VR training can help workers keep themselves safe, these simulations can also teach factory employees about AI systems designed to improve safety. Many workers have never interacted with AI systems tasked with actively reinforcing safety guidelines before and may be inclined to ignore or distrust safety alerts that do not come from a person. AR and VR training can incorporate scenarios where a machine breaks down, or a co-worker fails to follow safety protocols to teach employees about which hazards an AI safety system can detect and how they should respond.

Detect Issues with Computer Vision

One of the main methods AI safety systems detect potential hazards is through computer vision. This technology lets AI “see” the factory floor through cameras, allowing the AI to raise safety alerts in real-time if, for example, it observes employees who might not be wearing the proper personal protective equipment (PPE). In geofenced safety zones, a computer vision-enabled AI can shut down equipment, restrict access to certain areas, and alert employees if it sees or anticipates a safety concern. It is important to note that AI-based safety systems are not a replacement for traditional training. Rather, AI-enabled computer vision is an important tool that factory managers can use to make their plants even safer.

AI can also help manufacturers improve safety on an individual employee level with the help of data analytics. An AI system can keep tabs on the number of safety incidents an employee is involved with, like warnings or violations. Then, AI can take this data and factor it in with individual employee information to construct a holistic view on a worker’s safety record. This record can be informed by data like years of experience, hours worked, and metrics collected from a wearable device like body temperature, muscle strain, and the amount of weight lifted per shift by the employee. Manufacturers can use this to better understand if their employees are under too much strain to sustain a safe working environment. Not only can manufacturers use AI-powered data analytics to determine which employees would benefit from additional safety training, plant managers can also use this information to better match employees to tasks based on their skills and physical abilities.

For decades, manufacturers have tapped robots to take over tasks that have a high risk of causing worker injury. Keeping humans away from heavy, moving machinery, toxic chemicals, and other risky environments has allowed manufacturers to place people in safer roles where specific skills and dexterity are highly valued. For example, even the most capable human workers possess a limited field of view. A forklift crash in a warehouse caused by a worker who failed to pay attention or missed a small hazard in their way could be devastating. However, an AI-powered forklift can use computer vision to monitor for hazards across the warehouse, reducing the risk it could bump into an employee or be crushed by a stack of pallets it crashed into. The former forklift operator could be reskilled into an oversight or maintenance role where they could provide even greater value.

Manufacturers can also assign dangerous inspection tasks to AI. Drones equipped with AI can inspect products stacked up to the high ceiling of a warehouse and determine the stability of the inventory. In plants where noxious fumes or dangerous chemicals are present, AI-powered robots can limit human exposure to potential hazards by performing regular maintenance and monitoring tasks. When humans must be involved in chemical plant turnarounds and total cleanouts, AI can monitor for safety compliance and environmental hazards.

Embracing the New Efficiency Paradigm

AI also represents a unique opportunity to improve the efficiency of production, especially when it comes to preventative maintenance. Currently, most factories use pre-scheduled maintenance plans to help prevent manufacturing errors that could stymie production. While maintenance schedules have undoubtedly prevented production disasters, pre-scheduled maintenance plans can be inefficient because they are not always informed by actual repair needs.

“Publicly available generative AI systems can hallucinate, including making up facts, citing nonexistent sources, or other false information”

On the other hand, a predictive maintenance plan powered by AI can allow plant managers to perform maintenance exactly when and where it is needed. By gathering information from transducers and other sensors, AI can monitor equipment temperatures, current power draw, and the status of different machine parts. This can help an AI system predict and prevent failures. When the technology detects an impending problem, a predictive maintenance system can further limit downtime by scheduling repairs when they will be least disruptive to factory operations.

AI can also support quality assurance (QA) and quality control (QC) by using laser distance sensors to perpetually scan for errors across a vast and fast-moving production line. In addition to keeping tabs on the quality of manufactured goods, AI can help plant managers keep machines properly calibrated by monitoring tolerances. Because many QA and QC tasks are highly repetitive, an AI system that has been taught which defects to look for can perform these tasks, allowing employees to focus on higher-value tasks within the plant.

In addition to preventing production problems, AI can also be used to address manufacturing defects and prevent similar ones going forward. In the event a customer returns a product, a plant manager can use a serial number to quickly determine when the production error occurred, and even which machine caused the error. Traditionally, diagnosing and solving the issue which caused the production error can be time consuming. However, an AI system with laser distance sensors can scan the product to determine the exact nature of the error and then ascertain which machine caused the error and how the equipment can be recalibrated to both fix and prevent the issue. This allows a factory to reduce both downtime related to diagnostics and inventory lost to production errors.

AI’s Risks

AI is not without risks. Integrating AI into production can increase cyber risk by creating new potential access points for bad actors. Manufacturers pursuing AI must consider the risks related to cybersecurity and take measures to mitigate potential issues. Additionally, publicly available generative AI systems can hallucinate, including making up facts, citing nonexistent sources, or other false information. Businesses that do not put safeguards in place to check these outputs could make decisions based on inaccurate information. Finally, if a company enters proprietary data into a publicly available generative AI, it does not have control over how that data is stored or used by the AI. This means it could be hacked or used to inform answers the AI provides to other users.

Approach to Adoption

While the future of AI in manufacturing could involve a revolution in production efficiency, it is important to understand where this technology might not be a fruitful investment. The less repetitive and homogeneous the task, the more extensively an AI needs to be trained by humans to properly execute it. Jobs which require greater dexterity, creativity, and experience may simply be better for a human to perform from both a cost and quality standpoint. For example, a local furniture factory may find that a worker assigned to evaluate fit and finish may only be able to flag 90% of errors. Even if an AI equipped with computer vision and laser distance sensors could flag 99% of defects, the cost and complexity of training an AI to correctly spot miniscule flaws may make a digital QA/QC improvement strategy untenable.

“The cost and complexity of training an AI to correctly spot miniscule flaws may make a digital QA/QC improvement strategy untenable”

When it has been determined that AI-based systems are feasible tools, manufacturers should carefully evaluate the potential ROI by clearly outlining which capabilities their plant actually needs. For example, a plant that produces dangerous chemicals may need the infrastructure to support a robust network of air quality sensors across an entire plant. On the other hand, a large candle factory might only need to support air quality sensors in specific rooms, and thus has smaller infrastructure requirements. Finally, given worker concerns over the efficacy of AI-powered safety systems, plant managers must also help employees overcome their skepticism with a transparent dialogue.

Preparing to Adopt AI Systems in Manufacturing Facilities

Tools like computer vision, sensors, and drones require adequate networking capabilities to be effectively used by an AI system in a manufacturing setting. While networking is an additional expense, the barrier to entry for powering AI-powered systems is lower than many manufacturers may think. In most cases, 5G wireless networking is not cost-prohibitive and is more than sufficient to provide fast, reliable connectivity.

A third-party vendor can be tapped to install the 5G networking equipment and software, as well as provide regular maintenance, software updates, and technical support. AI systems which rely on 5G-connected inputs can also be provided by third-party vendors, who may charge a monthly subscription to use their software or hardware. For most manufacturers, using a third-party vendor to supply and manage AI systems and networking equipment can help save money while allowing them to stay up to date with the latest technologies.

Enabling Employee Adoption

While the infrastructure for AI-based systems can be paid for with a monthly subscription, securing buy-in from factory workers being instructed to adopt AI systems is more complicated. Manufacturers can employ a variety of strategies to help employees understand that AI can make their jobs safer — not render them obsolete.

To overcome skepticism, manufacturers should start by demonstrating success via small pilot projects that illustrate the value of AI systems to workers. Tapping an influential employee to serve as an AI ambassador can help make pilot success stories more personal and authentic during discussions with skeptical employees and stakeholders. Demonstrating that workers’ safety is a priority and providing a platform for their concerns to be heard can also build faith that AI systems are there to support them in the workplace.

Depictions in popular culture often characterize AI as a risky unknown, or as a tool that executives use to automate away manufacturing jobs. Manufacturers should reiterate to workers that their industry faces a labor shortage, and rather than replacing jobs, AI can help factories fill some of the roles for which companies are struggling to hire. AI can also open doors for current employees to move into more productive, less repetitive roles. This could allow many workers to deploy their skills in a more valuable way while also working in a safer environment.

The Future of AI in Manufacturing

AI has the potential to transform worker safety and boost efficiency — but not in a vacuum. Manufacturers should take care to determine that investments in AI, including employee training, infrastructure development, and buy-in campaigns, will likely lead to tangible improvements to worker safety and generate cost savings from efficiency gains. For example, manufacturers won’t realize the benefits of sensors and cameras tasked with helping an AI system prevent manufacturing defects if the networking equipment that connects them to an AI system is unreliable or inadequate.

“Tapping an influential employee to serve as an AI ambassador can help make pilot success stories more personal and authentic”

Even with the most meticulously planned AI systems, manufacturers who are serious about AI success must train and educate workers to make them feel more confident in AI. Highlighting AI success stories, especially those that emphasize collaborative roles with employees, can help earn the support of factory or warehouse staff. Without employee buy-in, manufacturers may struggle to improve worker safety or boost efficiency with the power of AI.

Over the coming decades, new technologies are likely to help manufacturers achieve ever greater improvements to worker safety and factory. As companies grapple with the implementation of today’s AI technology, plant managers should remember that even the most exciting technologies can change little on their own. Manufacturers who learn to quickly secure employee buy-in and source a strong infrastructure of supportive technology will find themselves leading innovation rather than following other innovators. M

About the author:

Maurice Liddell is Principal and Senior Market Leader at BDO Digital

Welcome New Members of the MLC October 2023

Introducing the latest new members to the Manufacturing Leadership Council

![]()

Sudhir Arni

Senior Vice President, Customer Success

Sight Machine

sightmachine.com

![]()

https://www.linkedin.com/in/sudhirarni

Steve Boyd

Vice President, Manufacturing Strategy

Dover Corporation

![]()

dovercorporation.com

![]()

https://www.linkedin.com/in/steven-boyd-60786936

Gustavo Chohfi

Vice President, Quality Assurance and Continuous Improvement

Cornerstone Building Brands

![]()

cornerstonebuildingbrands.com

![]()

https://www.linkedin.com/in/gustavochohfi

Eric Murray

Vice President, IT/Digital

Cretex Companies

![]()

www.cretex.com

![]()

https://www.linkedin.com/in/eric-murray-mn

Jim O’Connor

Director of Enterprise Architecture

Graham Packaging

![]()

grahampackaging.com

![]()

https://www.linkedin.com/in/jim-o-connor-11022b10

Regina Salazar

CIO

Novelis Inc.

![]()

novelis.com

![]()

https://www.linkedin.com/in/regina-salazar

Sema Tekinay

Practice Partner – Transformation & Continuous Improvement

Messer

![]()

https://www.linkedin.com/in/tekinay

Matt Townsend

Vice President, Digital Transformation

Medtronic

![]()

https://www.linkedin.com/in/matt-townsend-05004319a

Dave Wingard

Global Leader Manufacturing Excellence

Westrock

Getting the Most Value from AI Investments

To capitalize on AI, manufacturers must learn how to prepare and analyze their data.

![]()

TAKEAWAYS:

● Manufacturers need to develop a thorough understanding of their data and the proper protocols for using that data.

● Manufacturers can use advanced technologies like AI to become more nimble, deliver better operational insights, and gain a more nuanced understanding of customer needs and relationships.

● To take full advantage of their data, manufacturers need to focus on data and system architecture, data governance, and data analytics.

The manufacturing sector historically has been a slow adopter when it comes to investments in artificial intelligence (AI) and other transformative technologies that require a solid foundation of data and clear practices around data use. It’s common for organizations to have vast amounts of data but lack insight from that data for several reasons, including the persistence of manual data collection, information existing in silos, and failure to segment customers in meaningful ways.

There has been significant hype around generative AI in 2023, but feeding the appropriate data into such AI tools is critical if companies want to benefit from the technology. Manufacturers looking to exploit advanced technologies to their fullest extent need to develop a thorough understanding of what data they have and proper protocols for using that data. Companies must capture, curate, and cleanse the data they have before they can determine how best to monetize them.

By first preparing the data properly, teams will then be able to use data not just for day-to-day operational tasks or metrics—such as how much product shipped on a given day or how inventory levels have changed in recent months—but to think more creatively about what else they can learn from data sets.

“Manufacturers that foster curiosity among their leadership and employees about AI will better position themselves to creating a factory of the future.”

Manufacturers that foster curiosity among their leadership and employees will better position themselves to create a factory of the future. Being a leader in AI will be necessary to remain competitive. According to a June 2023 Manufacturing Leadership Council survey about AI in 2030, “while many manufacturers may only just be starting to leverage the possibilities of AI, they also have clear plans to accelerate that adoption significantly in the years ahead, with AI investment levels expected to rise in a substantial 96% of all the companies responding to the survey.”

Think Bigger: Developing a Research Agenda

The use of AI in a manufacturing setting goes well beyond the shop floor. Companies can harness AI to improve quote-to-cash and order-to-cash processes, identify revenue leakage in business models, and assess whether the business has effective contract procedures in place, for instance. Many of these applications come down to figuring out where the business lacks key processes, or where processes aren’t being followed.

For companies setting out to explore how AI can improve their business—whether via process mining, robotic process automation, or machine learning—developing a research agenda can help. That agenda should examine these key elements:

- Data outputs: Does the organization fully understand the key outputs/outcomes it is measuring? Are there other outputs that would be useful to capture?

- Correlations: How do various outcomes compare to each other, and are there indications that they may have a significant relationship?

- Explanatory variables: Which relationships between data outputs might be especially useful or informative going forward?

- Dimensions of analysis: What are the various ways teams can analyze data points to understand customer behaviors better? Are there seasonal or geographic implications?

Using internal and external data to support this research agenda can help companies identify new opportunities and reduce the amount of uncertainty they face in both the short term and long term.

Becoming a nimbler organization and delivering better operational insights to leadership are two important ripple effects of honing this agenda and reducing uncertainty. Perhaps even more critical is the ability to gain a more precise understanding of customer needs and relationships. Manufacturers can use AI to ferret out relationship patterns, meaningfully segment customers, and determine costs associated with various relationships. These insights can ultimately enable companies to develop more tailored approaches to their customers, partners, and vendors.

“Manufacturers can use AI to ferret out relationship patterns, meaningfully segment customers, and determine costs associated with various relationships.”

Optimizing supply chains, improving quality control, and making the shift from reactive maintenance to proactive, predictive maintenance are specific areas where manufacturers stand to benefit most from AI. Predictive maintenance, for instance, uses AI algorithms to analyze real-time data from sensors and other equipment to anticipate equipment maintenance needs and failures. By continuously monitoring data from the factory floor and comparing that data against key performance indicators, AI can detect anomalies or early signs of equipment malfunction. This allows for proactive measures to avoid costly, unplanned downtime and improve the life span of the equipment.[1]

Performing maintenance prior to failure leads to cost savings and minimizes costly repairs or replacements. By leveraging data analysis, pattern recognition, and predictive modeling capabilities, industrial organizations can optimize equipment performance, increase operational efficiency, reduce costs, and enhance overall productivity.[2]

Improving Your Data: Where to Start?

Manufacturers don’t always know where to begin to improve their ability to harness, filter, and analyze data. Connectivity among machines, products, employees, suppliers, customers, and processes across the value chain is critical to gaining actionable insights, but enabling that connectivity with Industry 4.0 technologies must be intentional.

To be able to take full advantage of the enormous amount of data they generate and collect, manufacturers need to focus on three foundational areas:

- Data and system architecture: Understand how to balance traditional system architecture with newer architecture such as cloud-based storage and Internet of Things devices.

- Data governance: Implement clear standards around the collection and use of information.

- Data analytics: Harness advanced analytics to go beyond pattern identification and develop truly predictive capabilities.

Manufacturers also need to make sure that teams throughout the organization have the same baseline level of data literacy, and provide training as needed to align that literacy. Data literacy makes it easier for teams to adhere to the same data processes, policies, and standards around information protection and security.

“Once manufacturers have created a solid data foundation and fostered a sense of curiosity among employees, they can determine how AI tools may benefit their business in the future.”