Survey: Smart Factories Enter the Execution Era

Manufacturers push deeper into execution as smart factory strategies mature, AI advances and digital transformation gains as a competitive advantage.

![]()

KEY TAKEAWAYS:

● Smart factories have entered the execution era with manufacturers now wrestling with how to scale digital transformation efforts

● AI is maturing beyond experiment into value-driven, smart factory deployments

● Digital transformation is shifting from table stakes to a game-changing advantage

The Manufacturing Leadership Council’s 2026 Smart Factories and Digital Production Survey shows an industry that has moved beyond experimentation and into a more disciplined phase of execution, integration and operation. Manufacturers are increasingly committed to digital transformation and are now figuring out how to scale it.

While economic optimism and investment intent remain strong, the tone of this year’s survey reflects a more mature mindset. Expectations remain high for AI, automation and end-to-end digitization, but respondents also demonstrate a clearer understanding of the legacy, data and organizational challenges that accompany scale. Compared to 2025’s resurgence of momentum and 2024’s momentary hesitation, 2026 signals a new phase: steady progress, pragmatic confidence and a sharper focus on execution.

SECTION 1: Economic Outlook and Investment Trends

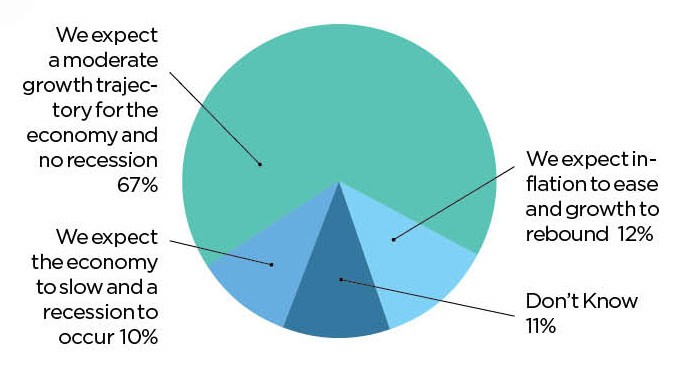

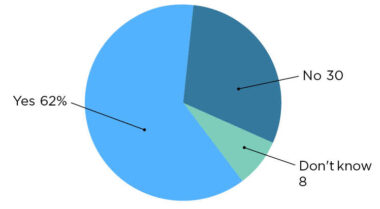

Manufacturers enter 2026 with cautious optimism about the broader economy. A strong majority (67%) expect moderate growth, while only 10% anticipate a significant downturn (Chart 1). These numbers remain similar to the 2025 survey results where 69% expected moderate growth while 8% expected an economic slowdown.

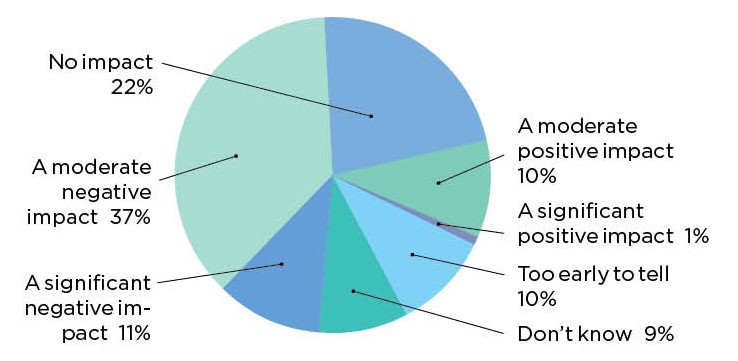

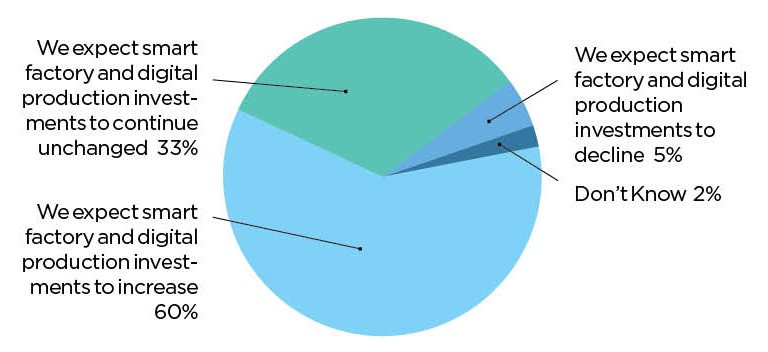

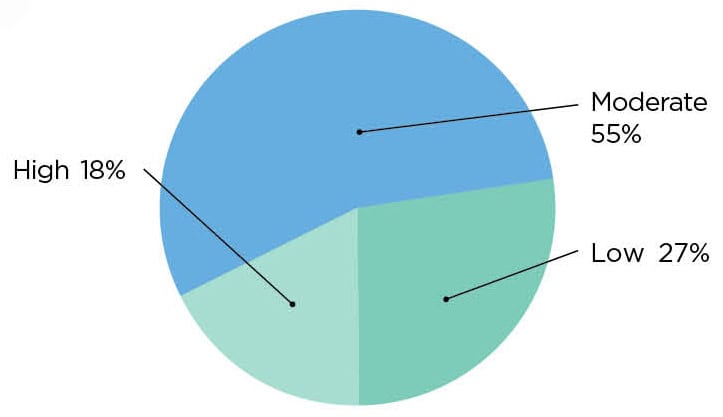

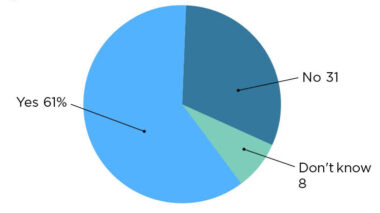

Meanwhile, nearly half of the respondents (48%) say U.S. tariffs are having a moderate or significant impact on their smart factory implementation (Chart 2). While those sentiments are worth watching going forward, the tariff negatives are not enough to undermine Manufacturing 4.0 digital investments. More than 90% of respondents say they expect to maintain or increase smart factory and production technology investments in 2026, with a sizable share planning increases rather than flat spending (Chart 3). The data suggests that digital investment has become embedded in long-term operating plans rather than driven by short-term economic sentiment.

1. Strong majority expect moderate economic growth ahead

Q: What is your company’s outlook for the economy in 2026? (Select one)

2. Nearly half experiencing negative impact from U.S. tariffs

Q: What impact are U.S. tariffs having on your company’s smart factory implementation? (Select one)

3. More than 90% plan to maintain or increase smart factory investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2026? (Select one)

SECTION 2: Smart Factory Maturity and Adoption

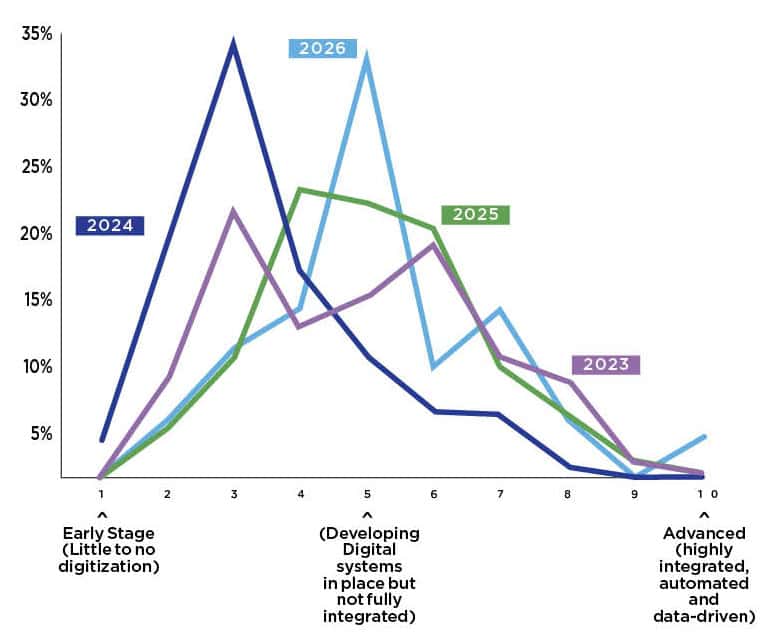

Smart factory maturity is a moving target. When new transformative technologies, like generative AI in 2022 and 2023, find their way into factories, it is natural for manufacturers to reassess how mature they truly are. This is one possible cause for the dip in maturity that our 2024 survey unveiled. As manufacturers have gotten more comfortable with GenAI and other emerging technologies, they’ve been able to find their footing and move forward on the maturity scale, and our survey saw a strong rebound in 2025 that remains consistent in 2026.

The vast majority still place themselves at a mid-level maturity (72% in 2026 vs. 75% in 2025), but our survey shows that those placing themselves firmly at the middle level, or a 5, has hit a high-water mark. This year, more than one-third of respondents say they are at a 5, compared to 22%, 11% and 16%, in 2025, 2024 and 2023, respectively. Growth at the highest maturity levels (8-10) remains incremental—rising from 9% in 2025 to 10% in 2026—reinforcing that advanced smart factories are still the exception rather than the rule. (Chart 4)

This pattern is echoed in how manufacturers describe their digital activities. Fewer than 10% of respondents report being in the learning stage. Meanwhile, a nearly equal number report that their company is scaling at either a single factory or rolling out initiatives across multiple sites (49%) compared to those in the learning or experimental stages (51%). (Chart 5)

Looking ahead, confidence in future progress remains strong. While only a minority (28%) consider their factories very or somewhat smart today, a substantial majority (88%) expect to reach those levels by 2028. (Chart 6)

The data suggests that manufacturers believe the foundation is now in place, and they are heading toward the destination. Diving into the digital adoption of specific functions bears this out. It is clear that digital efforts are still a work in progress. Only product design, production/assembly and R&D rise above 15% of respondents reporting that these functions are at an advanced level for their company. The good news is that more than 40% of respondents say they are at least at an intermediate level for every single function we asked about in our survey. (Chart 7)

4. Smart factory maturity continues to advance

Q: How would you assess the maturity level of your smart factory journey? (Scale of 1–10, with 10 being the highest level of digital maturity)

5. Those scaling nearly equal to those in the experimentation and learning stages

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today? (Select one)

6. Manufacturers expect smarter factories ahead

Q: How “smart” do you consider your factory and plant operations to be today, and what do you anticipate they will be by 2028?

7. Advanced digital adoption remains a work in progress across functions

Q: At what stage of digital adoption are the following functions in your company? (Rate as early, intermediate, or advanced)

SECTION 3: Digitization and Automation Growth

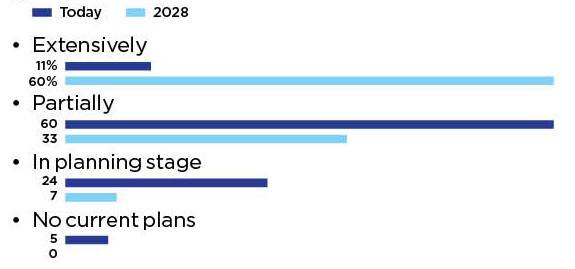

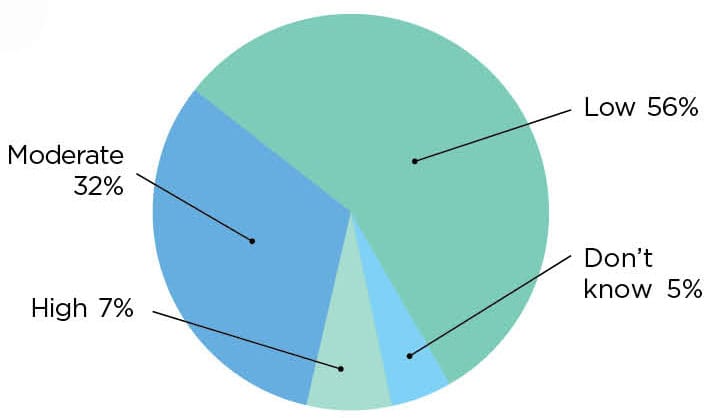

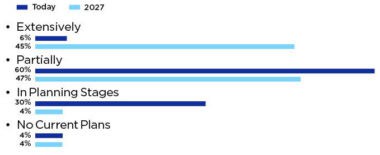

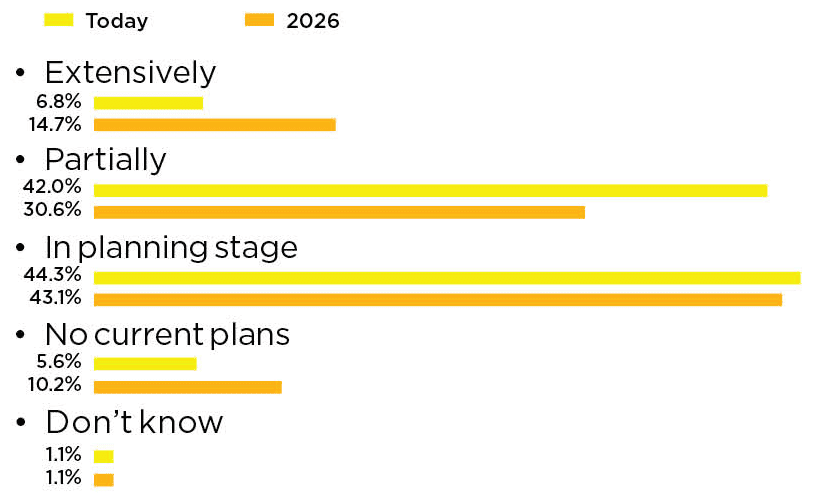

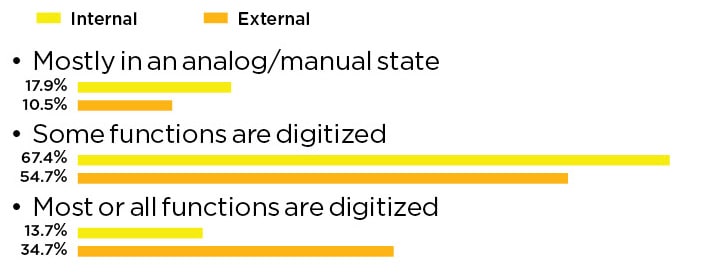

Digitization across factory operations is currently mixed. When considering production, maintenance, quality, planning scheduling and support functions, an equal number of respondents report partial end-to-end digitization or that end-to-end digitization is in the planning stage (45% each). At the extreme ends of the spectrum, 5% say they are extensively digitized or have no plans to digitize. But there are reasons for optimism, with 98% saying that their factory operations will be extensively or partially digitized end-to-end by 2028. (Chart 8)

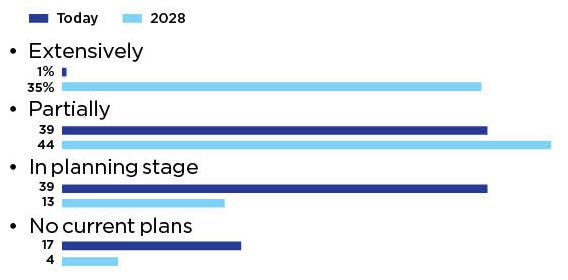

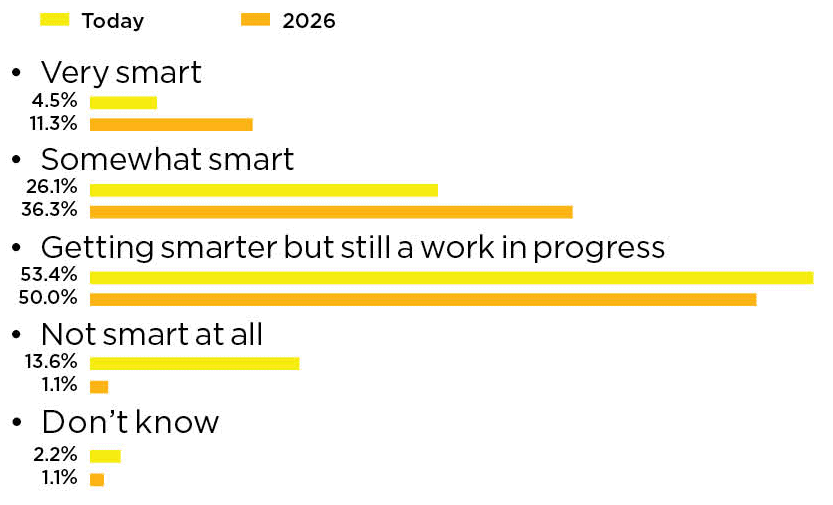

Production and assembly processes remain the focal point of digital efforts today. While extensive digitization is still limited to 11% today, expectations for the future are strikingly high, with most respondents anticipating at least partial digitization by 2028. (Chart 9)

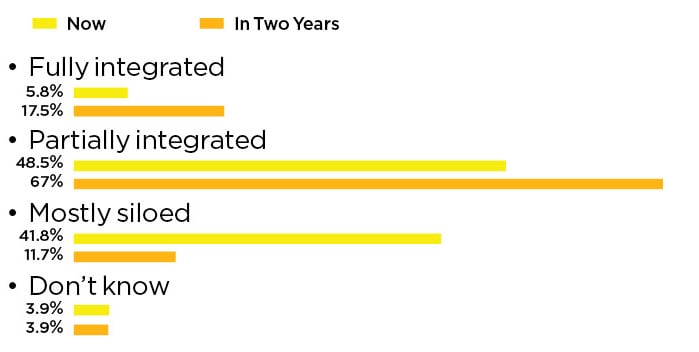

Integration beyond the factory, however, continues to lag. Digital integration with suppliers and customers shows improvement but remains well behind internal digitization efforts. This gap highlights both the complexity of ecosystem integration and a major opportunity for future value creation. (Chart 10)

8. End-to-end factory digitization expected to accelerate

Q: Thinking about your overall factory operations (production, maintenance, quality, planning, scheduling, support functions, etc.), to what extent are they fully digitized end-to-end today, and to what extent do you anticipate they will be by 2028? (Select one for today and one for 2028)?

9. Assembly process digitization on the horizon

Q: Focusing specifically on your core production and assembly processes (activities taking place on the manufacturing line), to what extent are these processes digitized today, and to what extent do you anticipate they will be by 2028? (Select one for today and one for 2028)

10. Customer and supplier digital integration lags behind other functions

Q: To what extent are your production functions digitally integrated with customers and suppliers today, and what do you anticipate they will be by 2028? (Select one for today and one for 2028)

SECTION 4: Future Factory Models and AI-Driven Operations

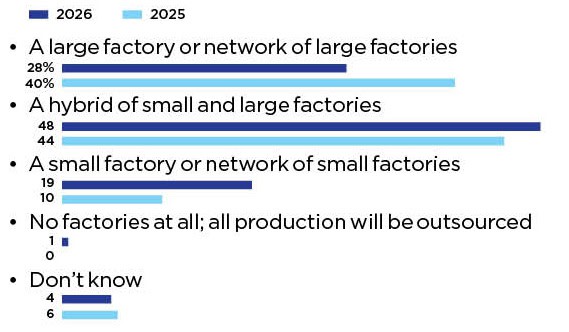

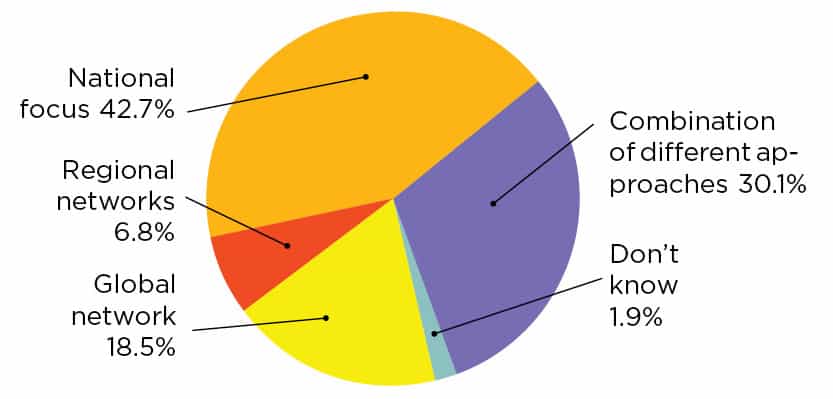

Manufacturers continue to envision a hybrid future for their factory networks. Most expect a mix of large-scale facilities and smaller, more specialized sites, balancing efficiency with flexibility. Compared to 2025, the biggest shifts occurred around the size of the future factory footprint. In 2025, 40% expected their future factory model would be a large factory or network of large factories, compared to just 28% in 2026. Meanwhile, the expectation to have a small factory or network of small factories grew from 10% in 2025 to 19% in 2026. (Chart 11)

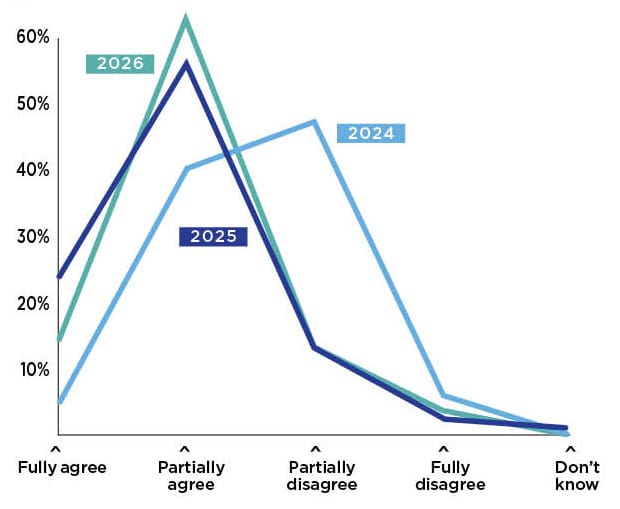

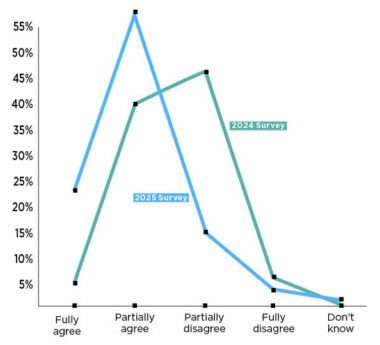

Confidence in AI-driven operations has remained steady. In 2026, 79% of respondents tell us they fully or partially agree that factories will evolve into self-managing, self-learning facilities. This aligns closely with last year’s survey where 80% fully or partially agreed. In both years, it’s important to note that those who partially agree far outweigh those who fully agree. This outlook has increased significantly since 2024, reflecting a more informed outlook that is, perhaps, shaped by leaders’ early experiences with AI technologies. (Chart 12)

11. Hybrid factory model remains dominant future strategy

Q: As you think about your factory footprint in the future, what is the expected future state of your factory model? (Select one)

12. Most partially or fully agree that tomorrow’s factories will be self-managing/learning

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.” (Select one)

SECTION 5: Technology Adoption and Priorities

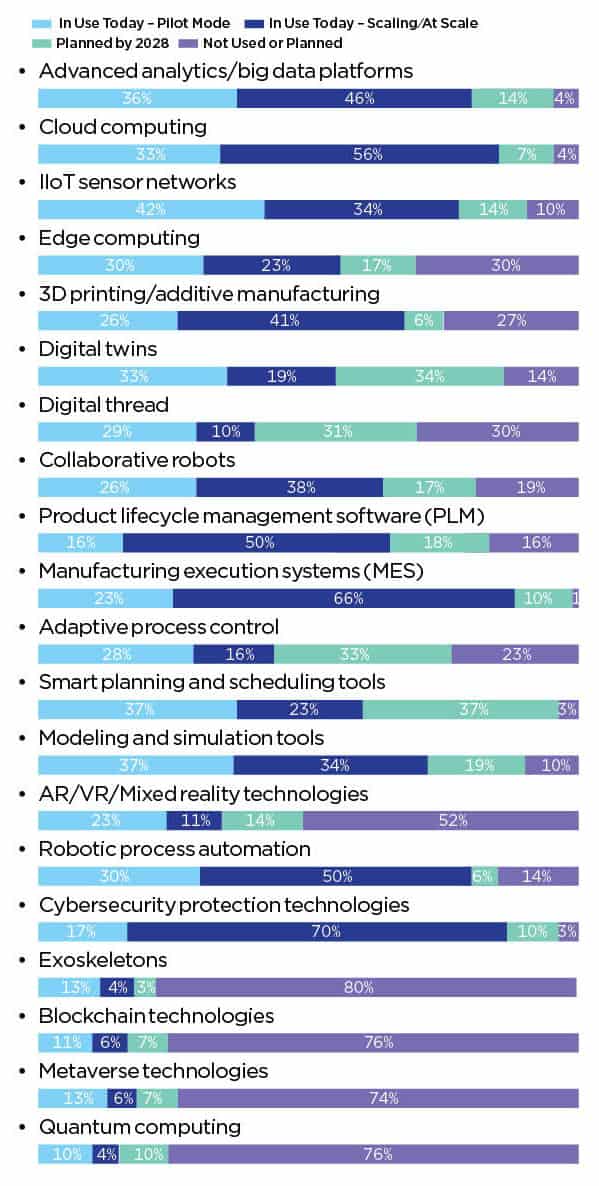

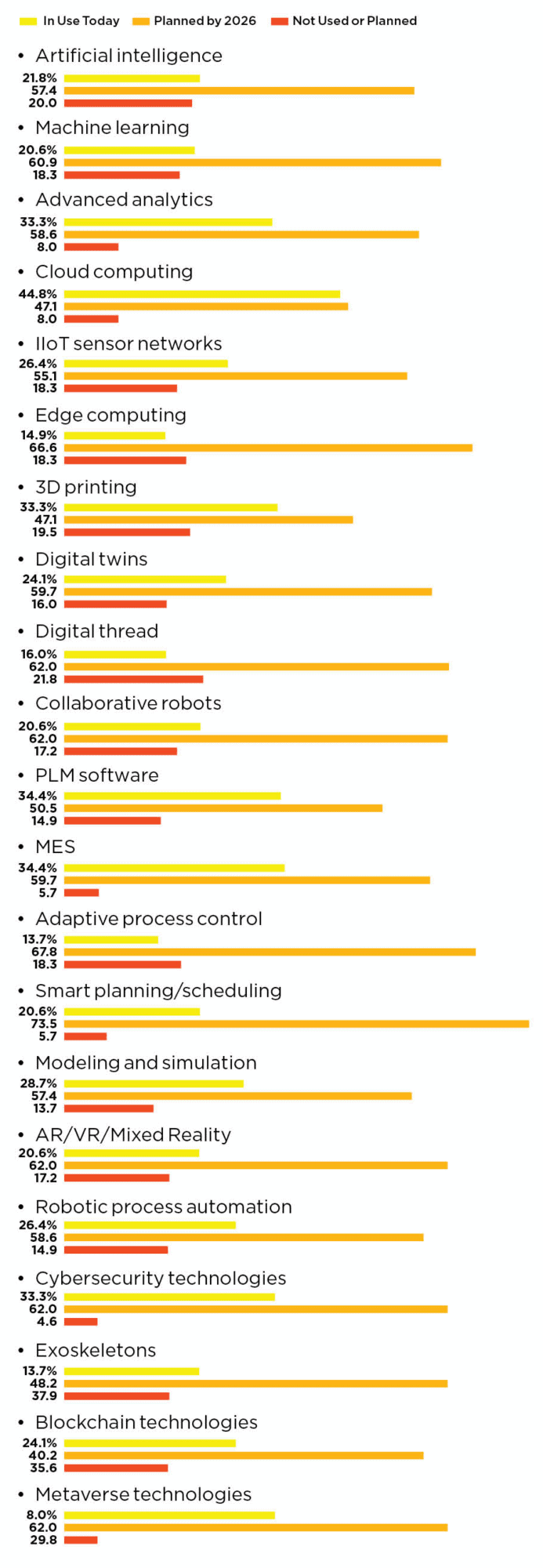

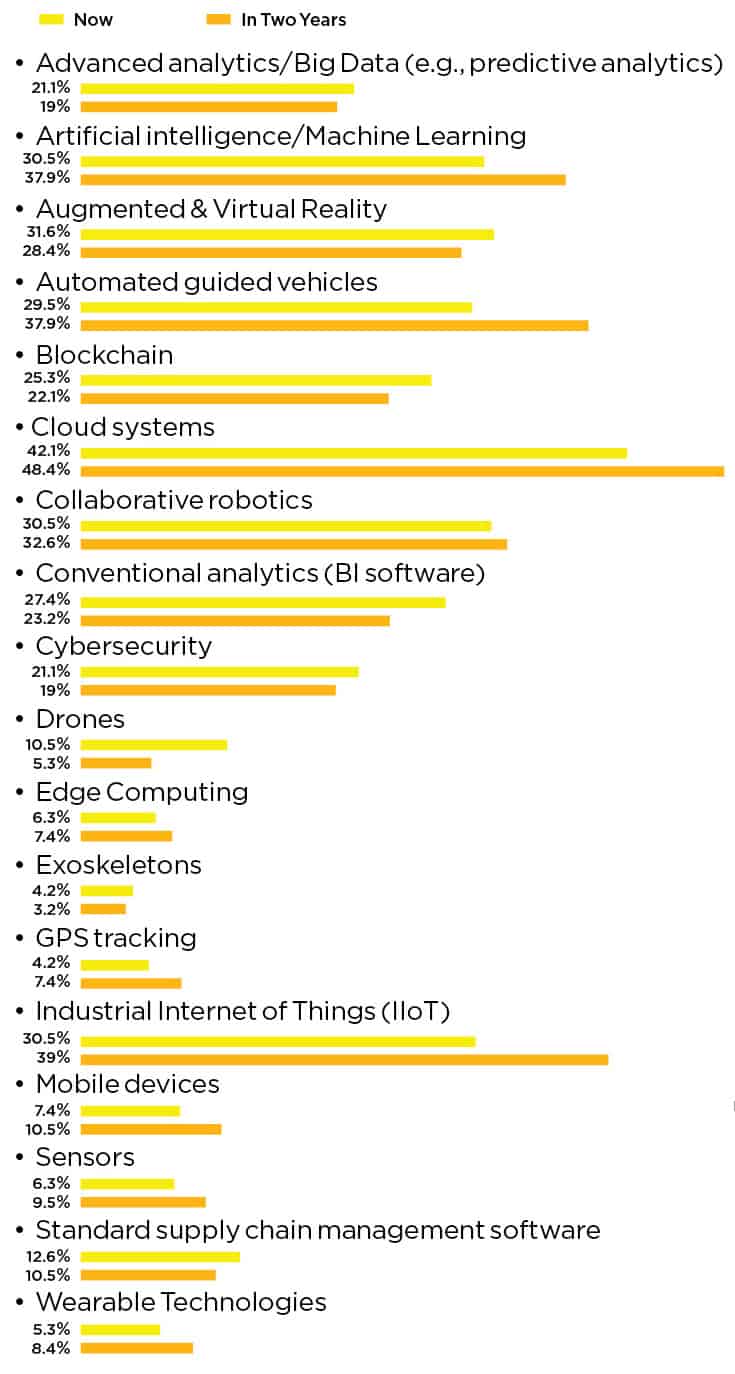

To that end, technology adoption in production operations continues to expand. Cybersecurity, manufacturing execution systems (MES), cloud computing, product lifecycle management software (PLM) and robotic process automation are the highest technologies deployed at scale today. These technologies are increasingly viewed as foundational rather than optional. Looking ahead to 2028, smart planning and scheduling tools, adaptive process control, digital twins, and digital thread are poised to make the largest leap forward. (Chart 13)

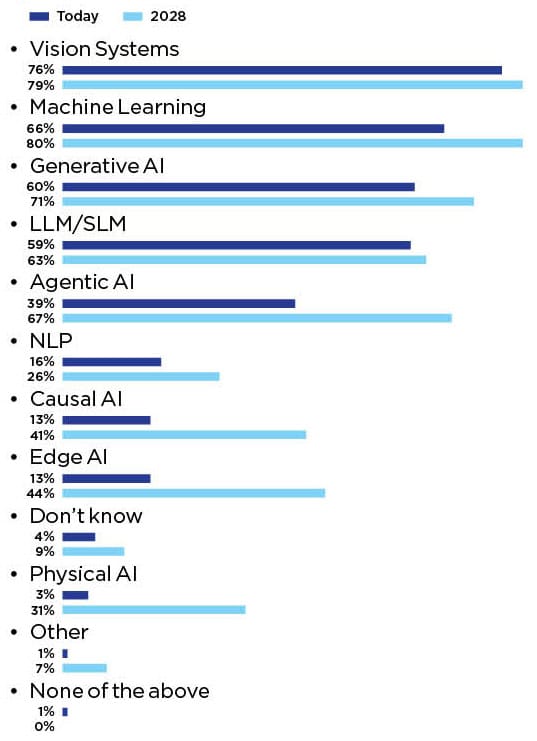

AI adoption is also advancing, with at least two-thirds of manufacturers reporting active deployment of traditional AI tools like vision systems (76%) and machine learning (66%). Across the board, every AI solution we asked about is expected to grow in its usage by 2028. Edge AI, causal AI and physical AI are expected to see the largest increases in use in that timeframe, while machine learning is expected to just surpass vision systems to become the most deployed AI solution. (Chart 14)

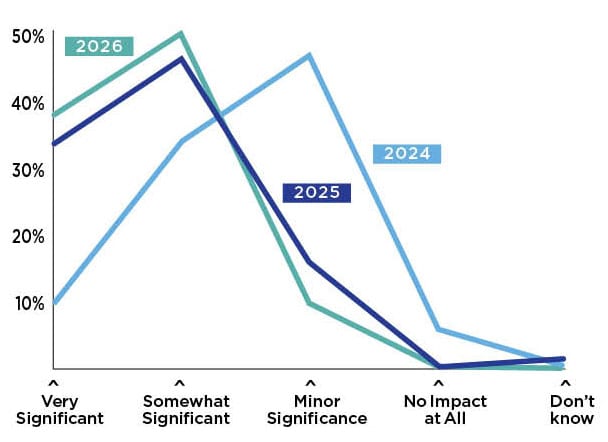

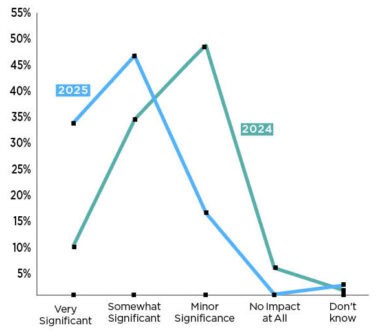

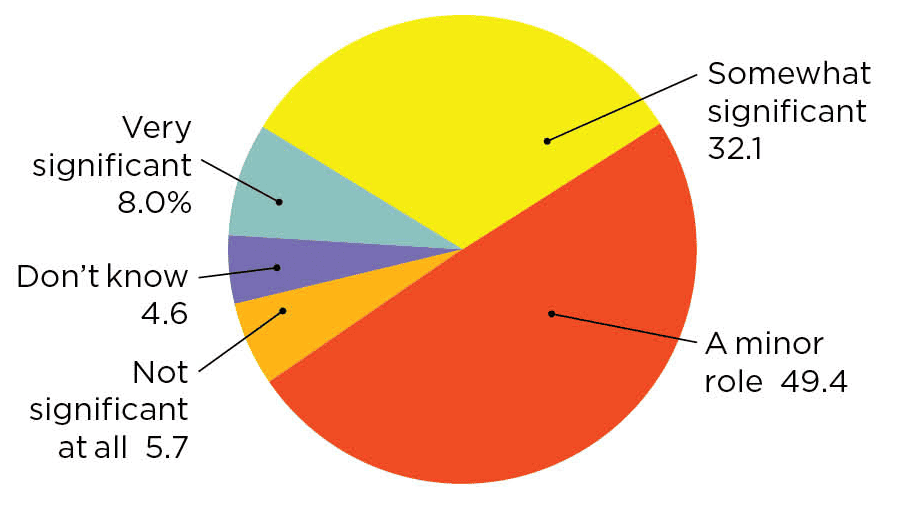

This measured pace is reflected in perceptions of AI’s impact. A growing percentage of respondents describe AI’s future impact on production as very significant (39%), continuing the upward trend from 2025 (34%) and 2024 (10%). (Chart 15)

Together, these findings suggest AI has moved beyond hype, entering a phase of value-driven deployment.

13. Multiple production operation technologies now surpass 50% scaling mark

Q: Where does your company stand in regard to the following technologies in its production operations? (Select one answer per technology)

14. Future growth ahead for every type of AI solution

Q: What types of AI solutions are you using today? (Select all that apply)

15. AI expected to have significant impact on production operations

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations? (Select one)

SECTION 6: Challenges and Benefits of Digital Transformation

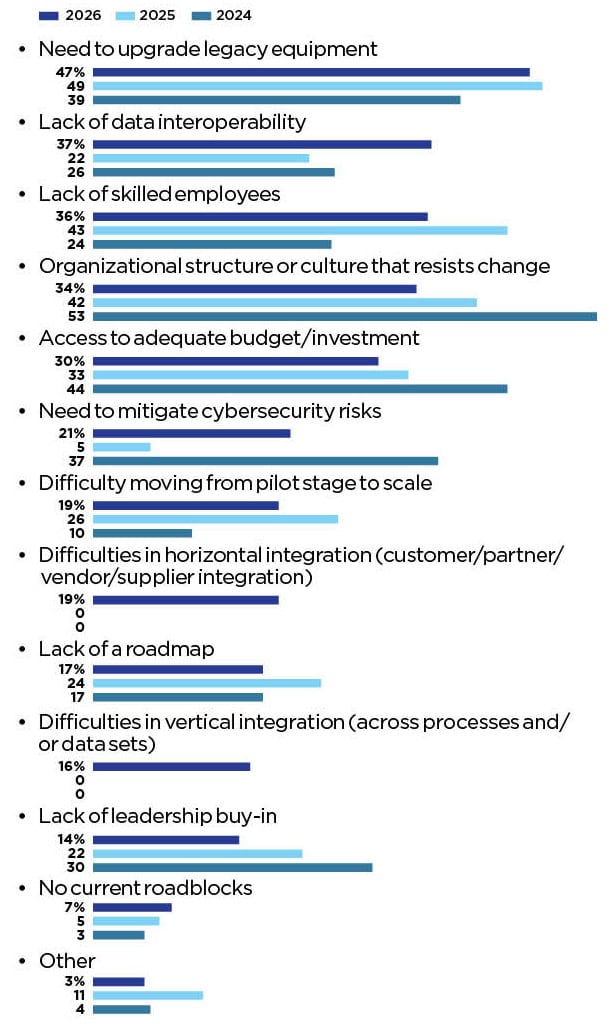

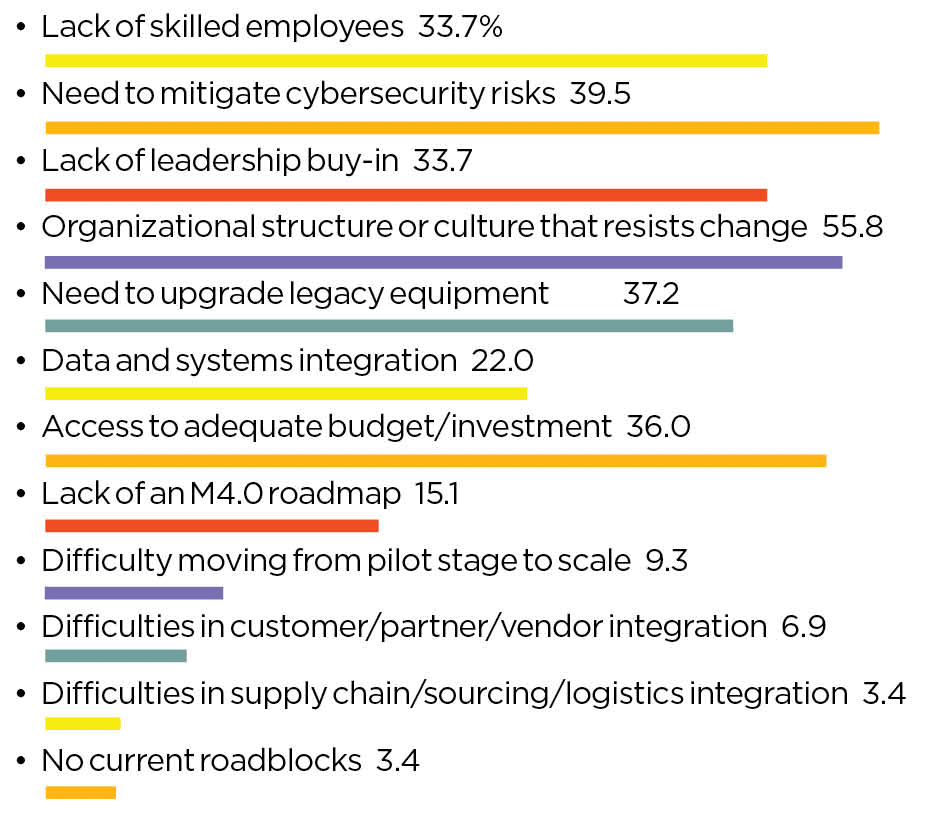

As digital transformation matures, so do the challenges manufacturers face. Legacy equipment remains the most frequently cited obstacle, though this concern has dropped slightly from 2025’s survey. Meanwhile, there has been a sharp increase in those identifying data interoperability as a roadblock to their smart factory strategy. In 2025, only 22% of respondents identified data issues as a primary roadblock, but that has increased to 37% in 2026. Only cybersecurity had a larger increase. In a sign of progress, five roadblocks fell by at least seven percentage points from 2025 to 2026: lack of leadership buy-in, organizational structure or culture that resists change, lack of a roadmap, difficulty moving from pilot to scale, and lack of skilled employees. (Chart 16)

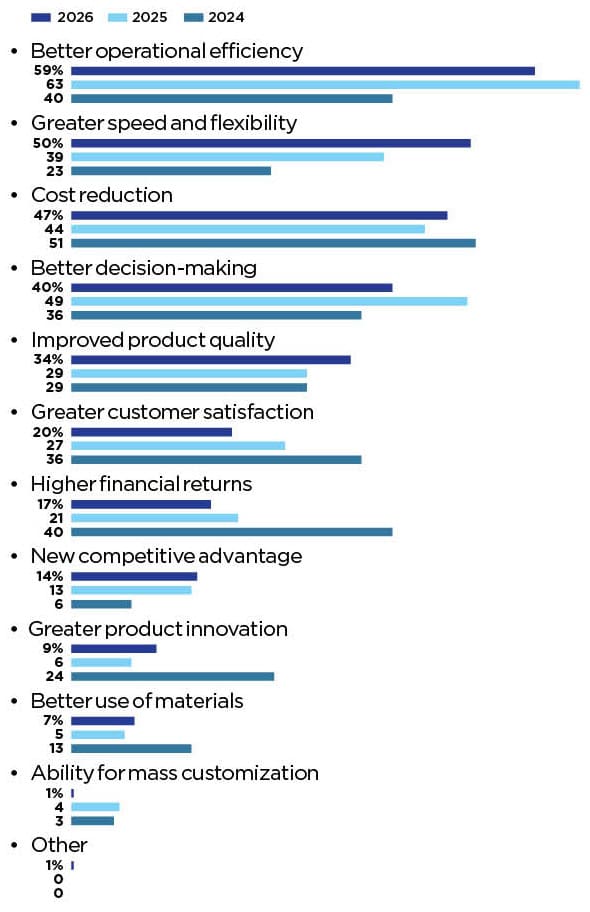

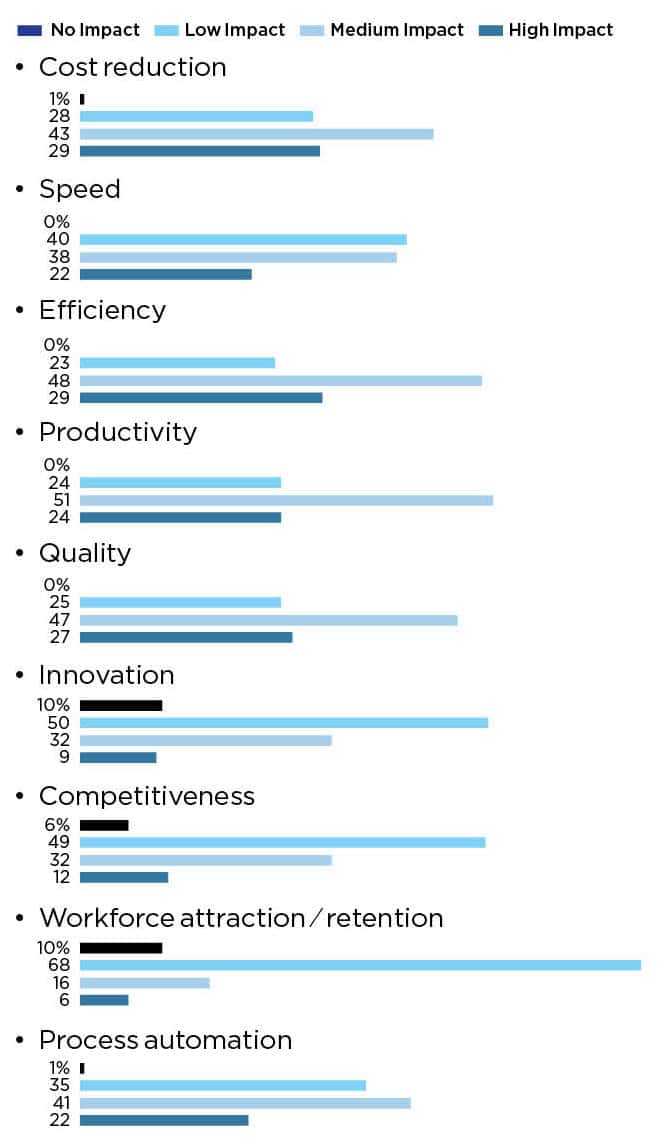

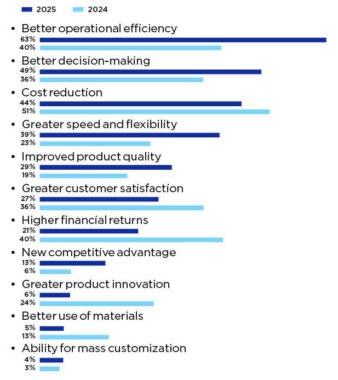

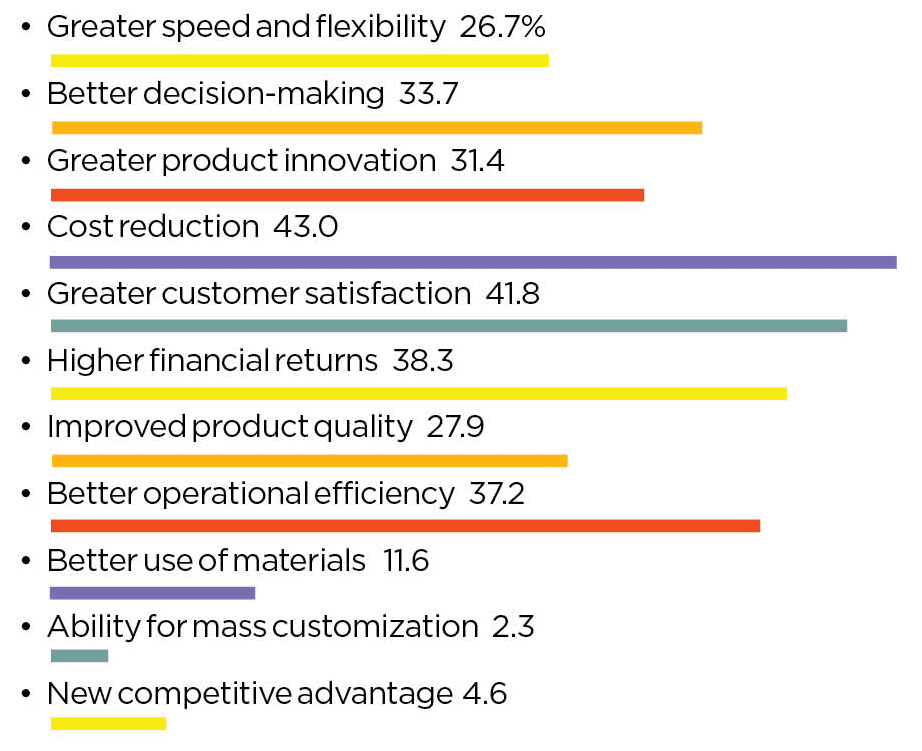

At the same time, perceptions of benefit continue to strengthen. Operational efficiency remains the top expected outcome, with greater speed and flexibility and cost reduction close behind. These results reinforce the growing belief that digital transformation is about more than technological advancement—it delivers measurable business value. (Chart 17)

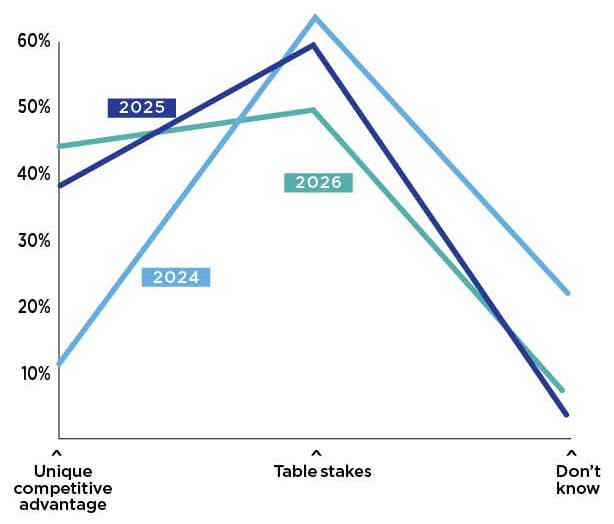

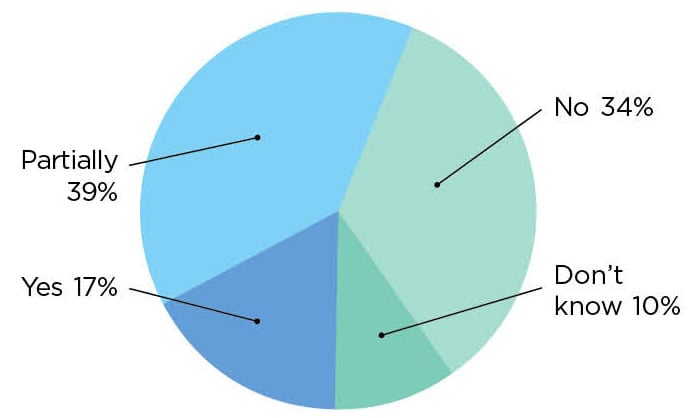

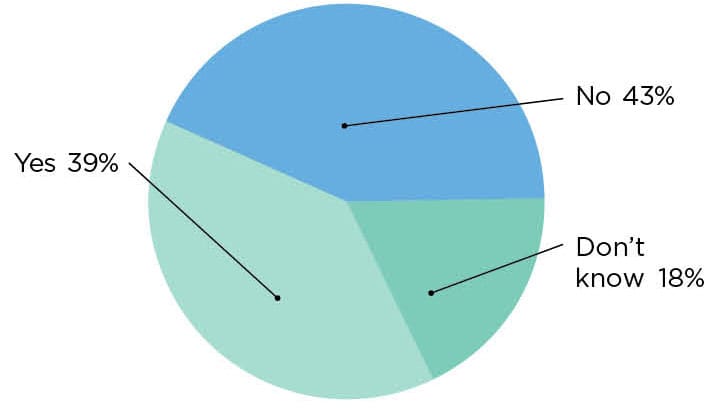

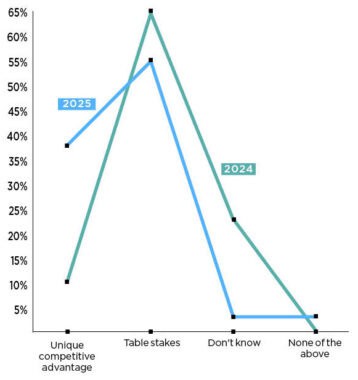

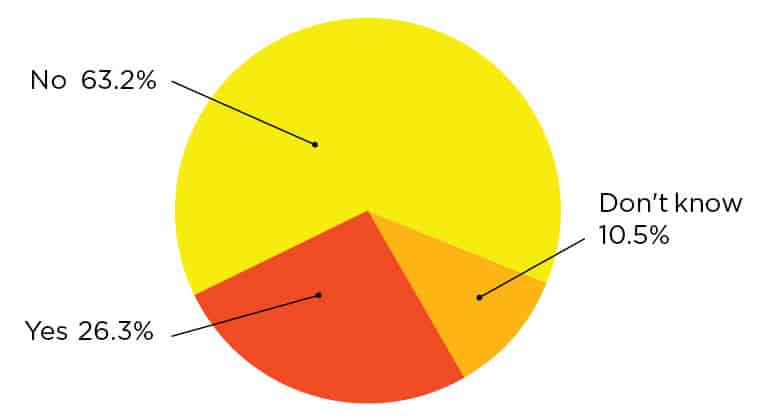

Importantly, while the largest group of manufacturers continue to believe that digital transformation is table stakes to stay in the game, 43% now view digital transformation as a competitive advantage—the highest percentage in the past three years. Because different companies progress on their digital transformation journey at different paces and with different success rates, those who are more successful are seeing a competitive advantage arise. While table stakes still dominate, the momentum is unmistakable. (Chart 18)

16. Legacy equipment, data and workforce are top roadblocks

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top three)

Note: horizontal and vertical integration difficulties were not included on 2025 or 2024 surveys

17. Better operational efficiency remains top benefit of smart factories

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top three)

18. Digital transformation seen as table stakes by nearly half

Q: Do you believe that digital transformation of your company’s manufacturing operations will create a unique competitive advantage for your company or is it merely table stakes to remain in the game?

SECTION 7: The Strategic Value of Digital Transformation

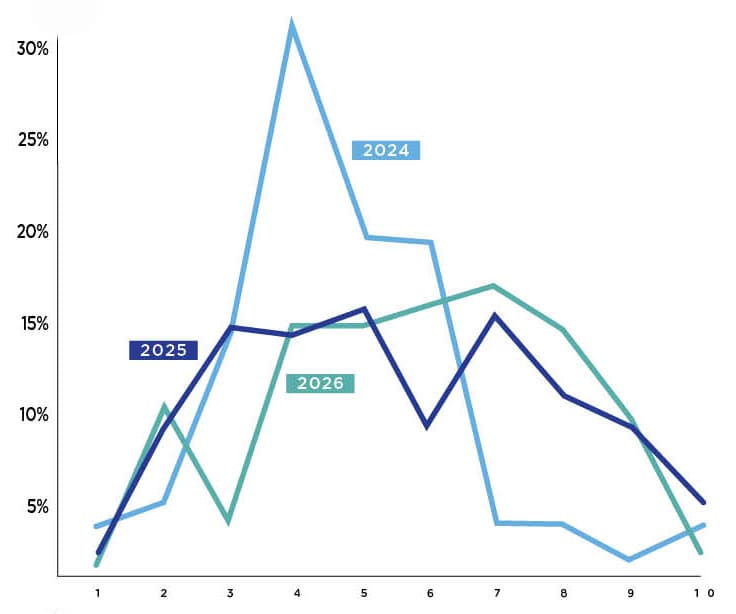

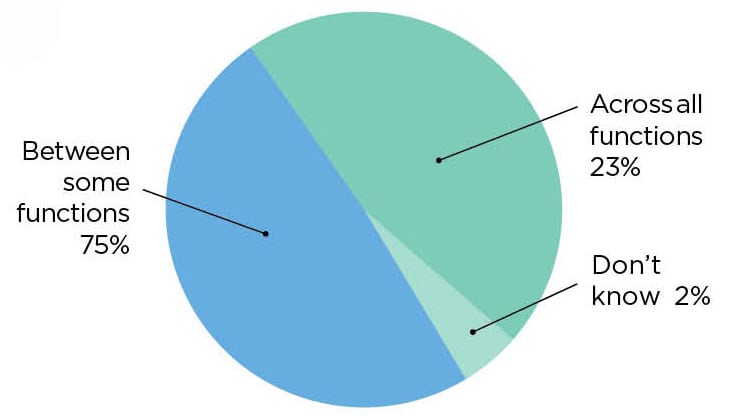

Manufacturers’ views on the strategic importance of digital transformation remain overwhelmingly positive. Perhaps that is why we have seen an increase in those reporting better integration of their smart factory strategy with their company’s overall business strategy. In 2026, 58% say they have passed the midway point (6 or higher) on their integration journey. That is up 11 percentage points from 2025 and a full 30 percentage points from 2024. (Chart 19)

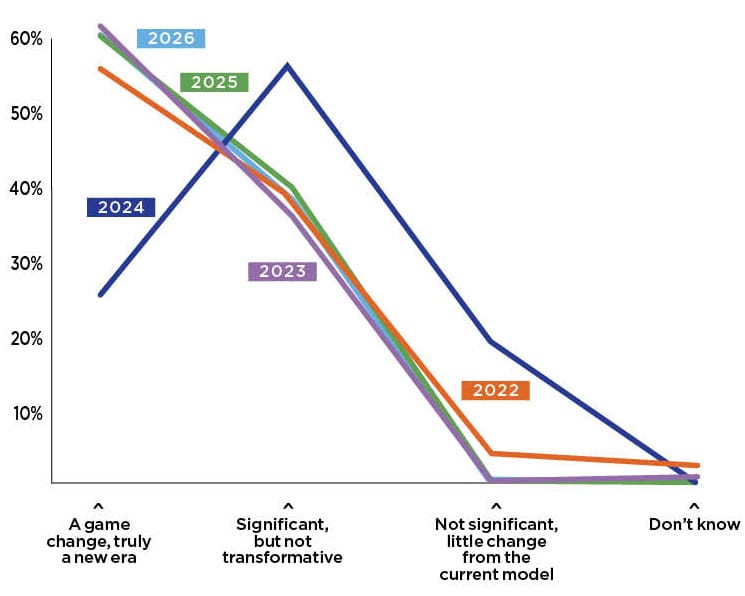

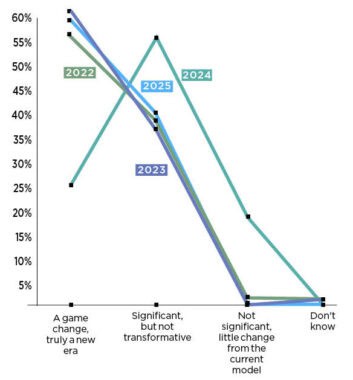

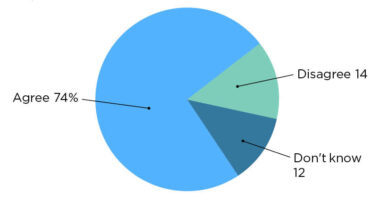

As digital transformation becomes more aligned with overall business strategy, it is not surprising that a clear majority believe digital transformation represents a fundamental shift in the manufacturing industry. Consistent with sentiment seen in 2025 and well above the dip recorded in 2024, 61% of respondents tell us that digital transformation is a game changer, indicating a truly new era for manufacturers. (Chart 20)

19. Smart factory strategy shows stronger alignment with business goals

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy? (Scale of 1–10, where 10 is fully integrated)

20. Optimism around digital transformation impact remains steady

Q: Ultimately, how significant an impact will digital transformation have on the manufacturing industry?

The Bottom Line

What has changed is tone. The 2026 survey reflects less exuberance and more resolve. Digital transformation is shifting from proving its value to delivering on it. As manufacturers move deeper into execution, the 2026 Smart Factories and Digital Production Survey confirms that Manufacturing 4.0 has entered perhaps its most consequential phase yet. The leaders of the next decade will be defined by who executes best on the new technologies available to manufacturers. M

About the author:

Jeff Puma is content director at the NAM’s Manufacturing Leadership Council.

Survey: Manufacturers See Data, Lack Strategy

Despite persistent challenges, data has made measurable impacts on performance and decision-making.

KEY TAKEAWAYS:

● Manufacturers recognize that data is the essential fuel for digital transformation, but without governance and analytics, they lack the “map” to turn data into strategy.

● While many companies report measurable gains in efficiency, cost reduction, and decision-making from data use, nearly half still lack a corporate-wide governance plan and processes to ensure data quality.

● Disparate systems, legacy equipment, and limited organizational data skills remain major obstacles, yet manufacturers increasingly view data as a quantifiable business asset tied to strategic outcomes.

Manufacturing data is the commodity that promises manufacturers a pathway to operational excellence. It can also act as an accelerant toward discovering new markets, new customers and innovation for both products and processes. Coupled with the urgency that many companies feel to bring AI into the business, there is no question that data is the necessary fuel for the digital transformation journey.

But if data provides the pathway, then governance and analytics are the map. Creating a map that is accurate relies on validated, contextualized, high-quality data. But met with the common challenges of disparate systems, legacy equipment, and a lack of organizational data skills, many manufacturers are instead left frustrated that the wayfinding they so desire is just out of reach.

Despite those challenges, manufacturers are seeing significant progress in utilizing data to make better decisions, while also increasing the frequency with which those data-driven decisions are made. They are seeing improvements in cost reduction, speed and quality. A growing number of companies are determining how to best put a quantified value on their data, adding a direct tie to the bottom line.

For manufacturers who diligently strive toward forging that data-driven pathway, improved business outcomes lie on the route ahead.

SECTION 1: Data is Valuable – Strategically and Financially

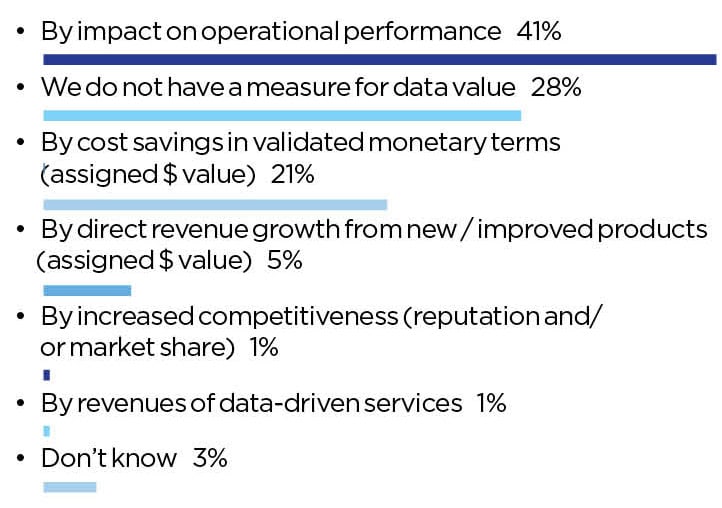

It could be said that data, like happiness, really can’t have a price tag, because it is by nature priceless. In the quest to assign its best value to align with business goals, companies value data differently. The greatest share of respondents reported that data’s value was measured by impact on operational performance (41%), while around a fifth (21%) said that data is assigned a dollar value.

Still, nearly a third of respondents (28%) said that they do not have any such measure for their manufacturing data (Chart 1). Without such quantifiable measures, leaders can find it challenging to gain support and investment for data-related investments or to initiate data pilot projects.

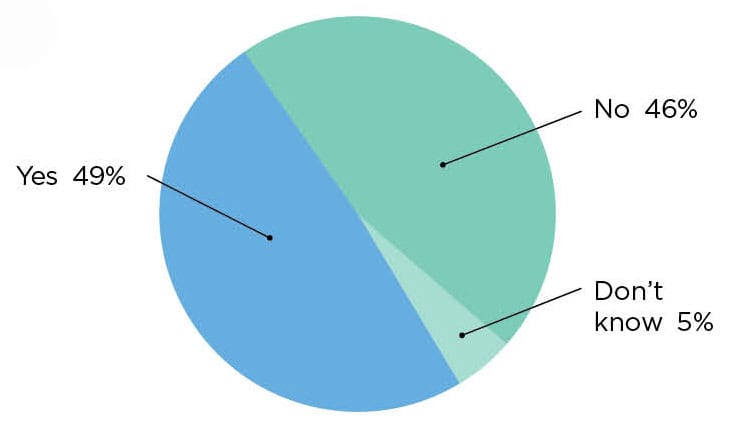

Likewise, the structure for making that aforementioned data-driven map is lacking at nearly half of all manufacturers—46 percent of respondents said that their companies lack a corporate-wide data governance plan (Chart 2). As data-sharing is fairly common for internal cross-functional teams (75%) (Chart 5), it seems likely that more companies will move toward a more strategic approach.

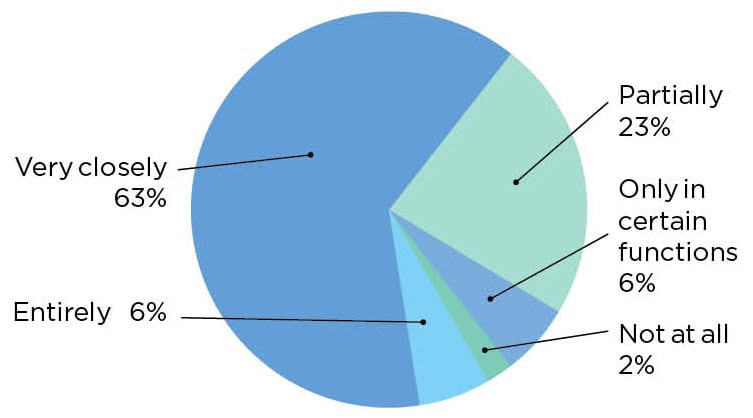

For companies that do have a data strategy, there is a payoff in alignment with overall corporate business strategy—70% say their company’s data strategy aligns with overall business strategy either entirely or very closely (Chart 3). And while only 17% of executives currently find their annual incentives or KPIs tied to data collection and management (Chart 4), it’s not hard to foresee a future where this becomes more ubiquitous.

1. Data is Valued by Performance and Cost Savings

Q: How do you measure the value of the data in your organization? (Select one)

2. Companies Divided on Corporate-Wide Governance

Q: Does your company have a corporate-wide governance plan, strategy, or formal guidelines for how data is collected, organized, accessed, and utilized across the enterprise, including manufacturing operations? (Select one)

3. Data Strategies Closely or Partially Align with Business Strategies

Q: How closely do you feel this data strategy is aligned to your company’s overall business strategy? (Select one)

4. Data Management has Tentative Ties to Executive Incentives

Q: Is data collection/management/analysis included in annual incentives, KPIs, or business imperatives for company executives/leadership? (Select one)

5. Cross-Functional Data Sharing Has Limited Reach

Q: Is data routinely shared cross functionally in your company? (Select one)

SECTION 2: The State of Data Sourcing and Quality

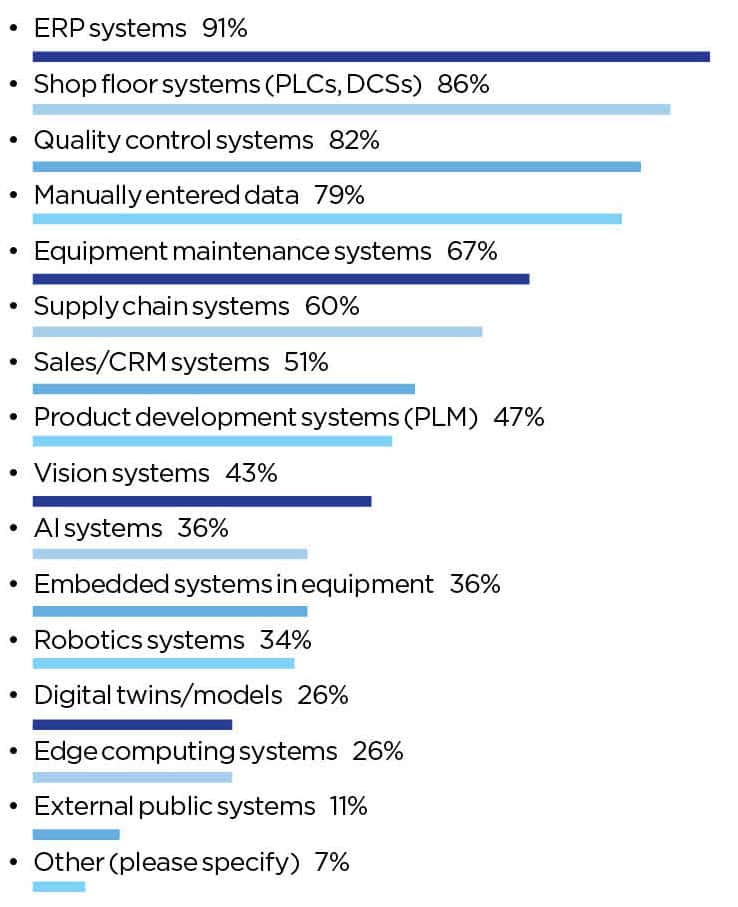

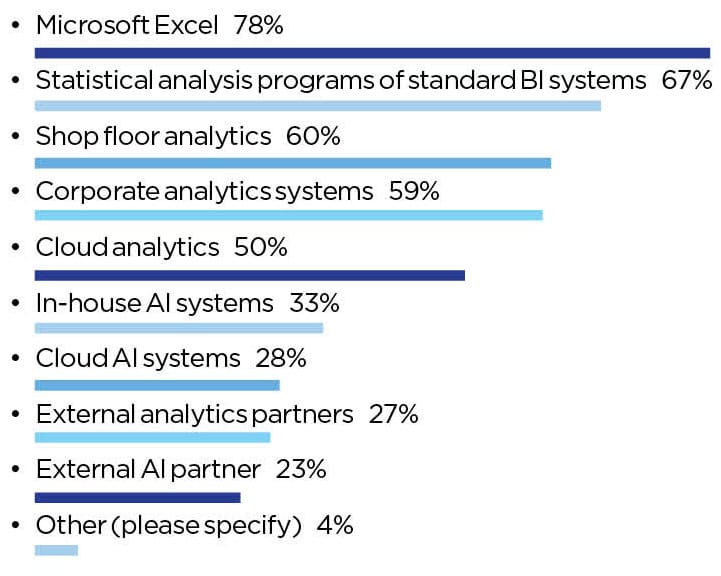

Most frequently, the well of manufacturing data is made up of enterprise-level data (ERPs), shop floor systems, and quality control systems (Chart 6). That said, 79% of manufacturers also include manually entered data—a potential source of data contamination downstream. Microsoft Excel still reigns as the undisputed champion for data analytics (Chart 7).

Respondents were somewhat pessimistic in their companies’ ability to collect the right data for business needs (Chart 8), but far more untrusting in the ability to collect AI-ready data (Chart 9). Alarmingly, only 39% said that their company has a process to verify data accuracy and quality (Chart 10).

6. ERP, Shop Floor and Quality Control Systems Lead the Data Supply

Q: What are the sources of your manufacturing data today? (select all that apply)

7. Microsoft Excel is the Most-Used Data Analytics Tool

Q: What systems do you use to analyze the manufacturing data you collect? (Select all that apply)

8. Companies are Moderately Skilled at Collecting the Right Business Data …

Q: How would you rank your company’s ability to collect the right data the business needs from your manufacturing operations? (Select one)

9. … But are Less Skilled at Collecting AI-Ready Data

Q: How would you rank your company’s ability to collect AI-ready data? (Select one)

10. Only 4 in 10 Have a Process to Verify Data Accuracy or Quality

Q: Does your company have a process to verify the accuracy and quality of manufacturing data? (Select one)

SECTION 3: Data Has Proven Value – But Challenges to Realizing It

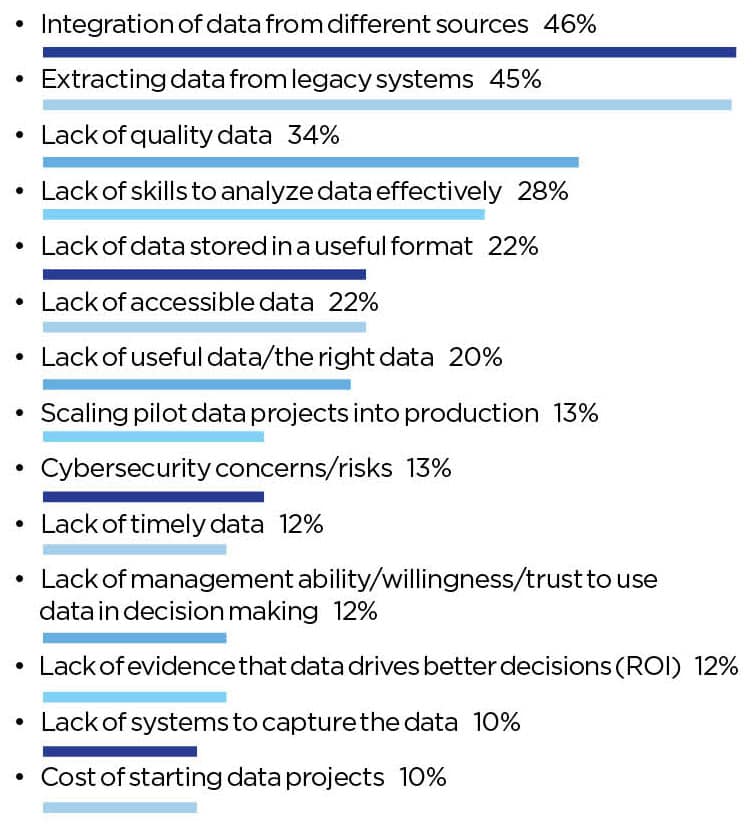

What stands between manufacturers and this promising data-driven future? The most persistent challenges include data from disparate sources (46%), the ability to extract data from legacy systems (45%), and the lack of quality data (34%). (Chart 14)

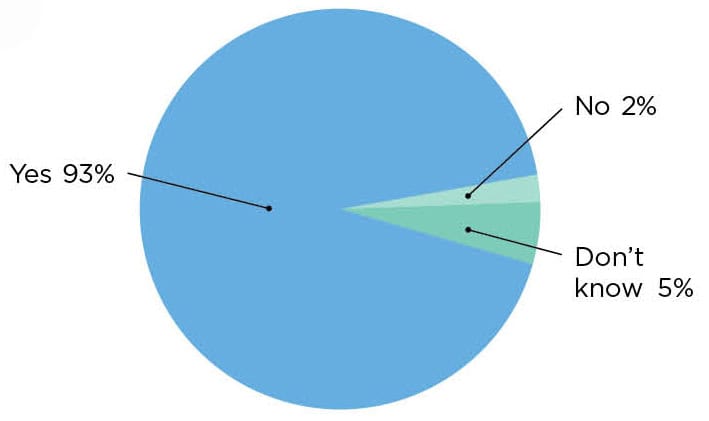

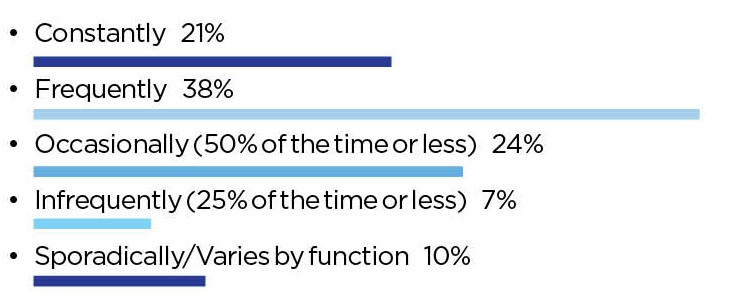

Despite the halting steps along the way, manufacturers are seeing true value from operational data. The highest level of impact has been seen on cost reduction, efficiency and quality. (Chart 11) Overwhelmingly, respondents say that data has improved their company’s decision-making process (93%). (Chart 12)

11. Cost Reduction, Speed and Quality All See Improvements

Q: What degree of impact has manufacturing data had in improving your manufacturing organization since the start of your digital journey?

12. 93% Say Using Data Improves Decision-Making

Q: Has the use of data improved your company’s manufacturing decision-making process? (select one)

13. Data-Driven Decisions Gaining in Frequency

Q: How often would you say your organization makes data-driven decisions today? (Select one)

14. Integration, Extraction, Quality Create Barriers to Leveraging Data

Q: What are the most important challenges or obstacles hindering your organization from making more data-driven decisions? (select top three)

About the author:

Penelope Brown is the Senior Content Director, Manufacturing Leadership Council

Survey: Tariff Tumult Roils Supply Chains

More than 40% are already seeing a negative impact from tariffs, resulting in rising costs, a new MLC survey shows. Greater resiliency using digital tools is a key mitigation strategy.

![]()

KEY TAKEAWAYS:

● Only 17% say their supply chains are “very resilient” today.

● 78% say they are engaged in supply chain process redesign as they bring in new digital tools.

● 90% believe that digital tools are critical in achieving greater resiliency.

Managing complex supply chains has never been easy, but it has gotten a whole lot harder in the first few months of 2025.

Manufacturers say that the Trump Administration’s on-off-on again tariffs have created disruptions and uncertainty, and they have no clear idea when it all may end.

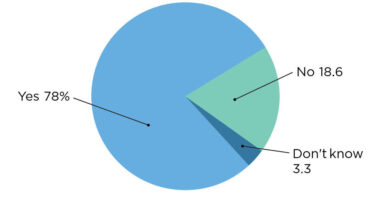

A new supply chain poll by the Manufacturing Leadership Council reveals that 43% of respondents are already experiencing a negative impact in their supply chains because of the tariffs, with nearly 20% saying the impact is significant. Uncertainty reigns for many others, with 45% saying it is too early to assess the impact of the trade measures (Q1).

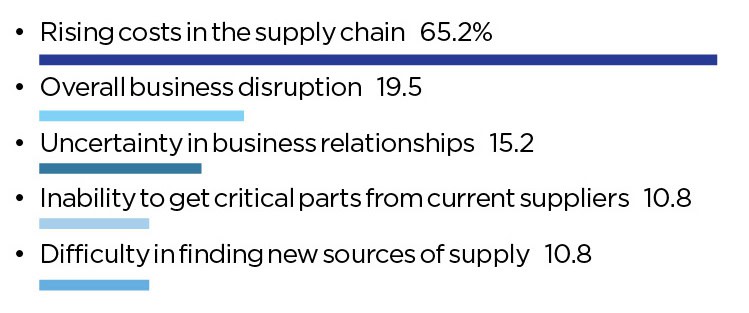

The most damaging effect from the tariffs, say 65% of respondents, is rising costs, followed by business disruption and growing uncertainty in their business relationships (Q2).

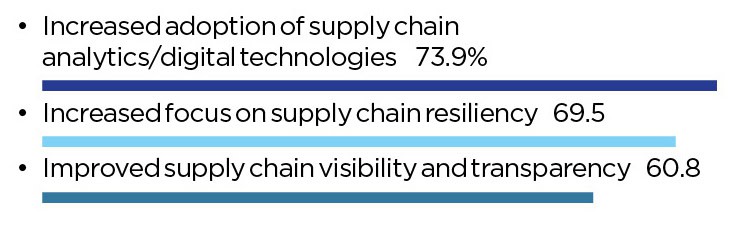

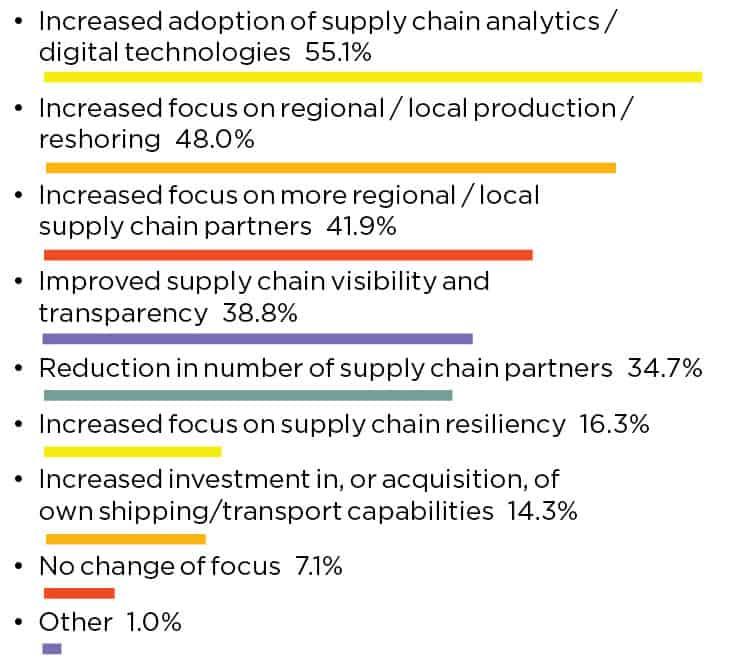

The result of the trade policy tumult is that manufacturers are doubling down on trying to achieve greater resiliency and visibility in their supply chains using digital tools, disciplines that rose to prominence during the COVID pandemic. Nearly 74% of respondents cited increased adoption of supply chain analytics as a key mitigation strategy in the current environment. And nearly 70% said they would be increasing their focus on ways to make their supply chains more resilient using those tools (Q3).

1. More than 40% Say Trump Tariffs Are Having a Negative Impact

Q: What impact are tariffs announced by the Trump Administration having on your company’s supply chain?

2. Rising Cost Is Most Severe Impact of Tariffs

Q: If your company is concerned about the impact of tariffs, what degree of importance would you assign to the following factors? (Percentage selecting 5, the highest level of importance)

3. Digital Tools, Resiliency Are Top Mitigation Strategies

Q: What strategies are you adopting to mitigate future supply chain disruption? (Top three)

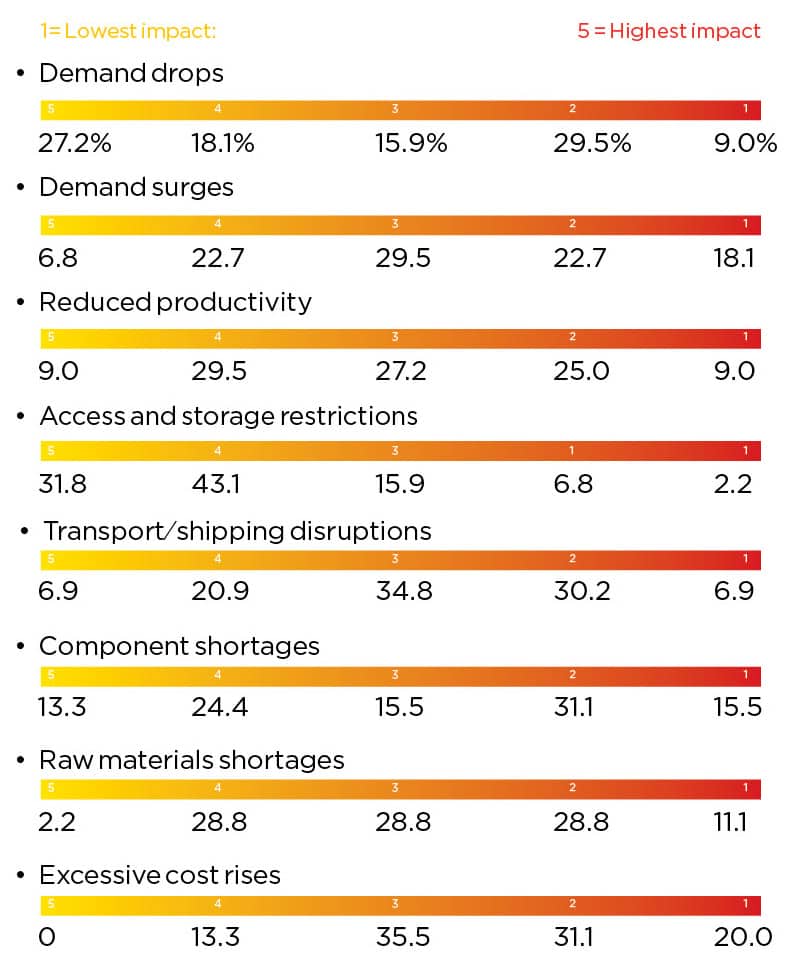

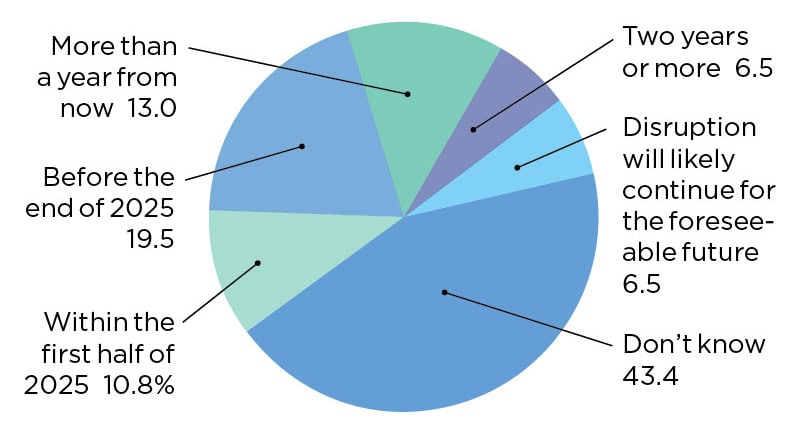

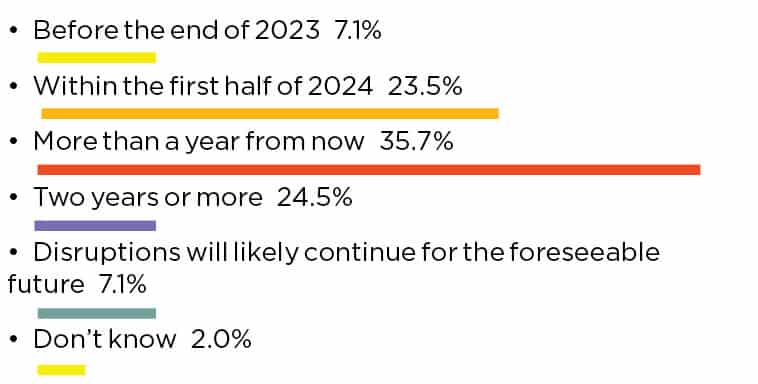

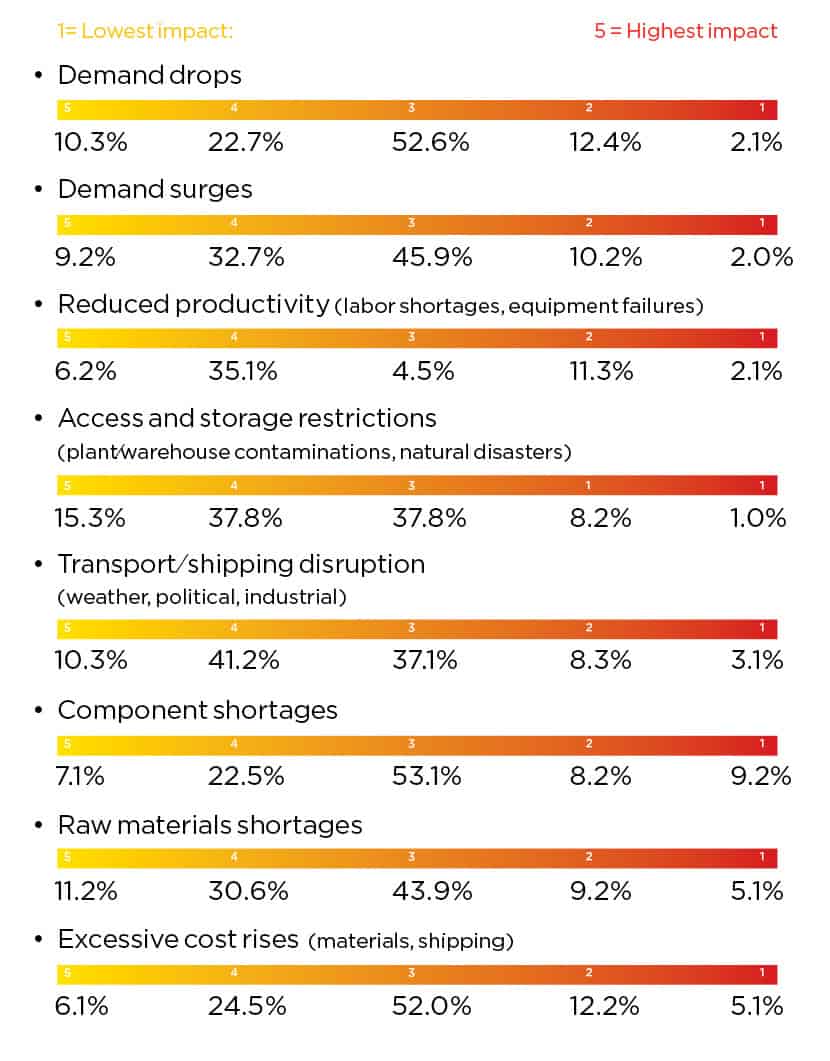

Manufacturers will need these tools not only for tariff-related mitigation. Market disruptions seem to have become the new normal. In recent years, cost pressures, demand surges, and component shortages have also adversely affected manufacturers’ supply chains, according to the survey. For those still dealing with them, there is little consensus on when they might ease. More than 40% say they simply don’t know when disruptions will subside (Qs4,5)

4. Rising Costs, Component Shortages Have Been Key Disrupters

Q: Over the last several years, what have been the most impactful types of supply chain disruptions you have encountered? (Ranked on a scale of 1-5, with 5 the highest level of impact)

5. Most Cannot Say When Disruptions May Ease

Q: If you are still experiencing supply chain disruptions, when do you expect the disruptions to subside?

Tracking Resiliency and Integration

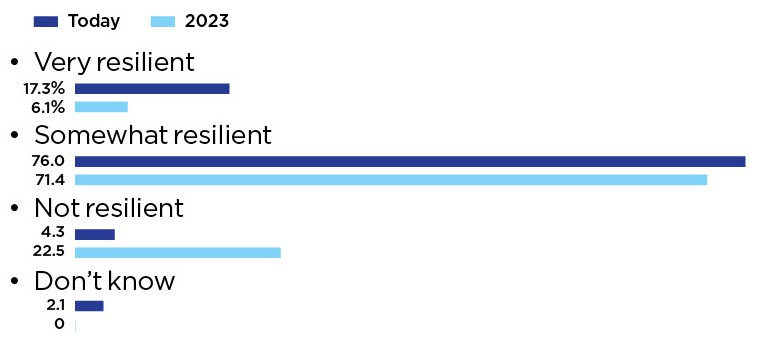

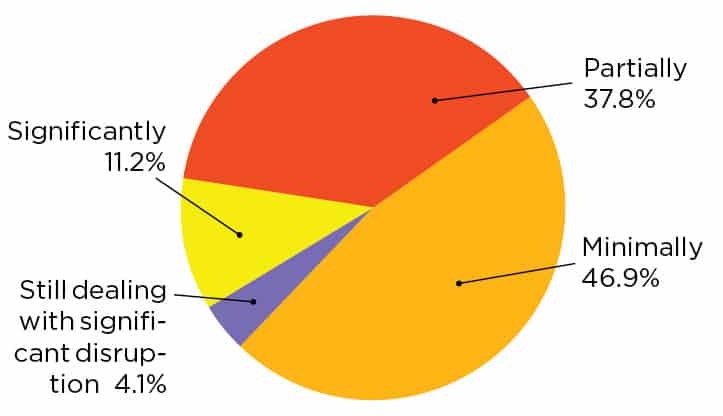

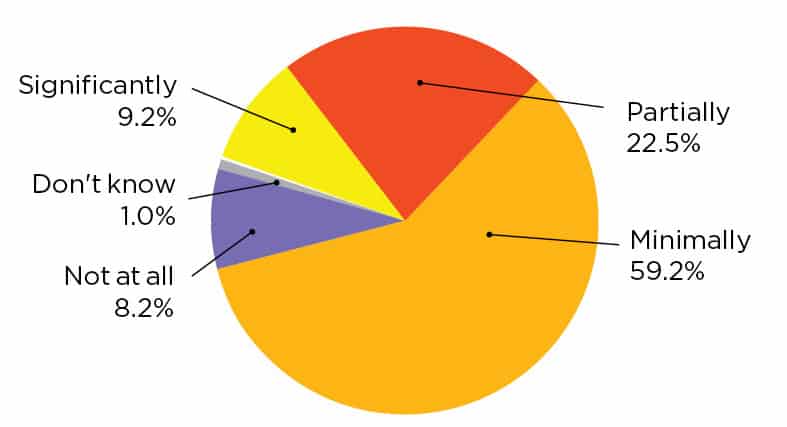

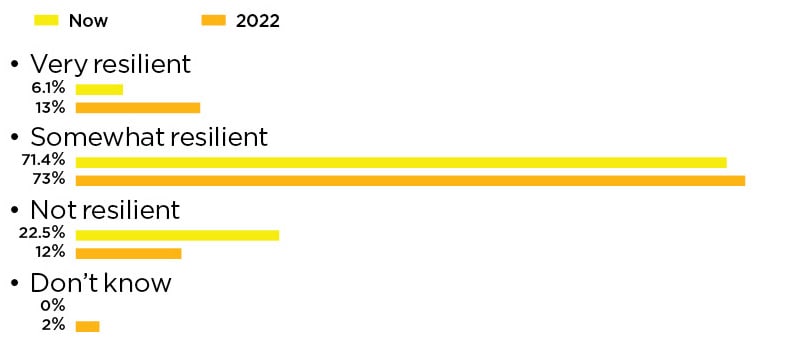

Considering all of the forces affecting supply chains, a determined, sustained focus will be necessary to push the resiliency cart further up the hill given that most manufacturers, 76% according to the survey, are only “somewhat” resilient today. But progress is being made. In the new survey, 17% say their supply chains are “very resilient” today. That compares with only 6% saying so in 2023, the last time MLC undertook a supply chain study (Q6).

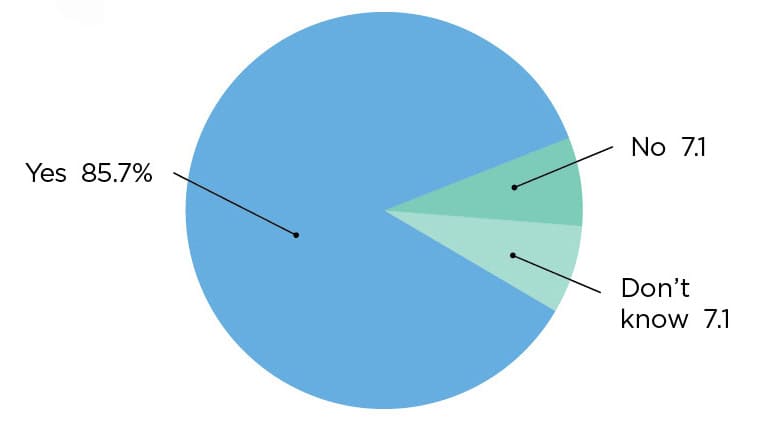

Central to this effort are three related things – supply chain process redesign, which 78% in the new poll say there are doing; reducing supply chain complexity, underway by 85%; and the increased adoption of digital tools, which 90% believe are critical to building greater resiliency into their supply chain operations (Qs7, 8, 9).

6. Greater Resiliency Is on the Rise

Q: How would you rate your current supply chain’s resiliency?

7. A Strong Majority Redesigning Supply Chains in Light of Digital

Q: As you adopt more digital technologies across your supply chain, are you also taking the opportunity to redesign your supply chain processes?

8. Reducing Complexity is a Key Goal

Q: Are you making specific efforts to reduce supply chain complexity and increase responsiveness and resiliency to disruption?

9. Digital Seen as Playing Significant Role in Achieving Resiliency

Q: Ultimately, how significant an impact will digital technologies have on creating more resilient manufacturing supply chains in the years ahead?

Of course, digitization and integration are required steps in creating a foundation for greater resiliency.

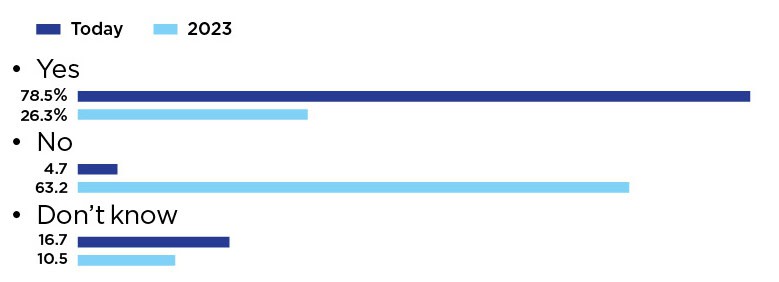

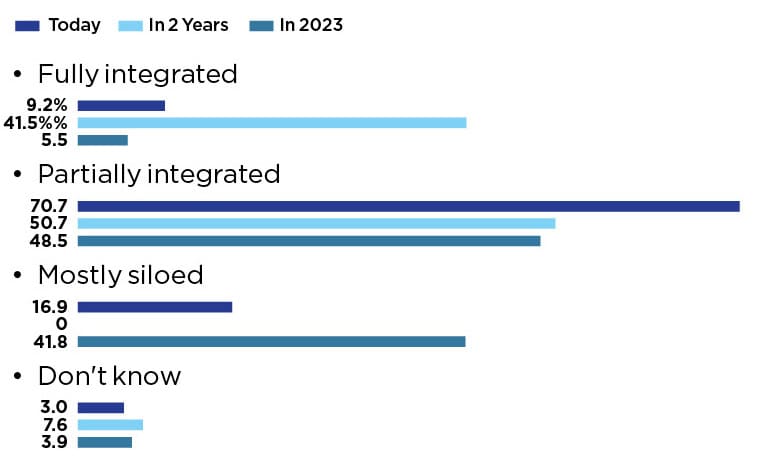

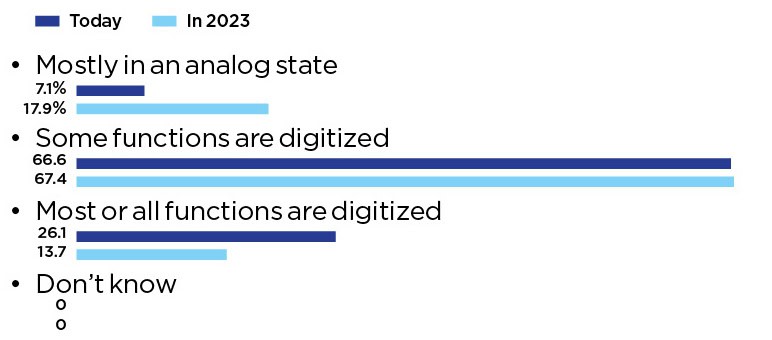

On the digital front, manufacturers are reporting progress, with 26% in the new poll saying that most or all of their supply chain functions have been digitized, up from 13% in 2023. A steady 66% say that some functions have been digitized at this point in time (Q10).

10. Strong Aspirations for Full Supply Chain Integration

Q: To what extent are your supply chain functions integrated today and to what extent do you expect them to be integrated in two years’ time?

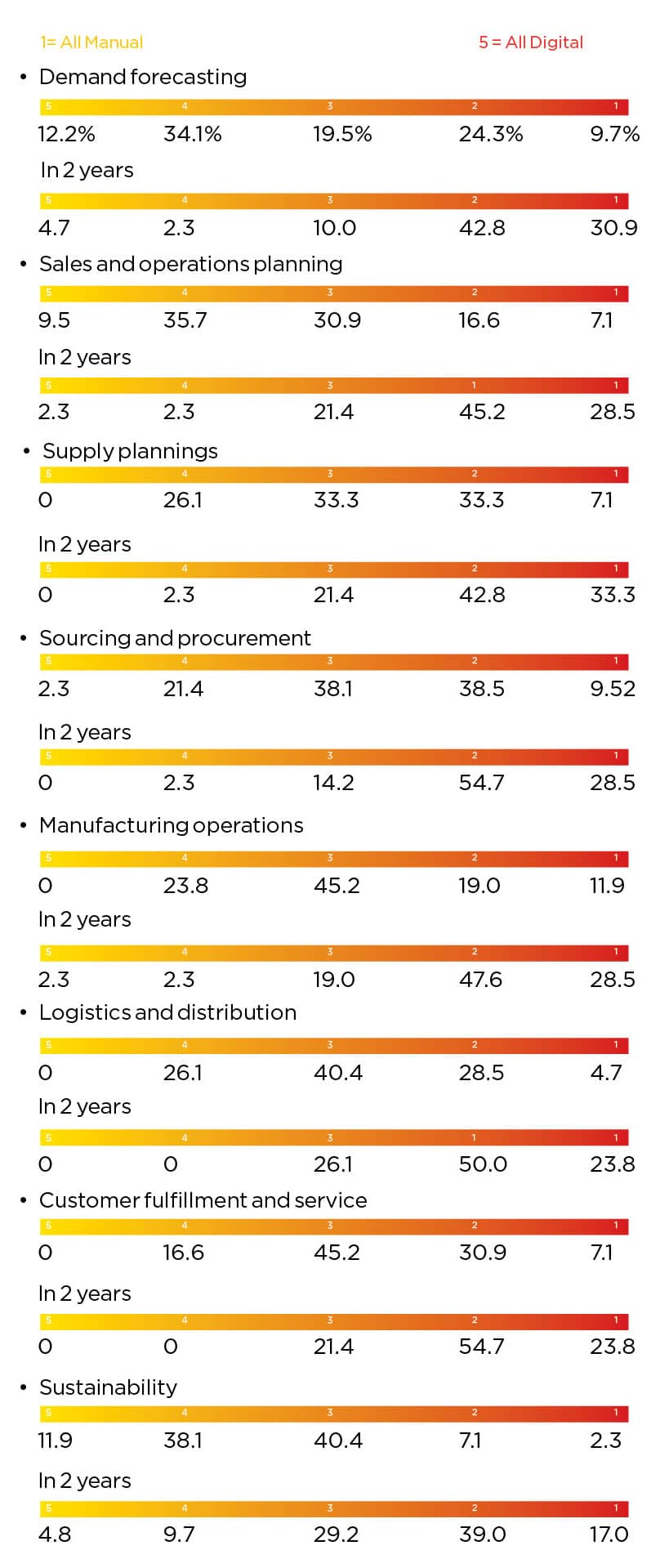

Over the next two years, digital aspirations are strong across functional supply chain areas.

Asked to mark the extent of digitization in eight functional areas today and in two years’ time, survey respondents in each case indicated they want to double and even triple the extent of digitization in their supply chain operations.

For example, only 9.7% say that their demand forecasting process is fully digitized currently. Within two years, though, more than 30% aspire to fully digitize this important process. In manufacturing operations, much the same dynamic is in evidence. Today, 11.9% of respondents say their manufacturing operations are fully digitized, but by 2027, 28.5% expect to be able to claim that achievement. (Qs11,12)

11. Internal Chains Have Become Increasingly Digitized

Q: Which description best characterizes the digital maturity of your internal supply chain functions today (plan, source, make, deliver)?

12. Operations Leads in Digitization but Many Functions Slated for Growth in Next 2 Years

Q: To what extent have you digitized the following supply chain functions today and what do you expect the extent will be in two years’ time? (Ranked on a scale of 1-5 where 1 indicates all manual, and 5 indicates all digital)

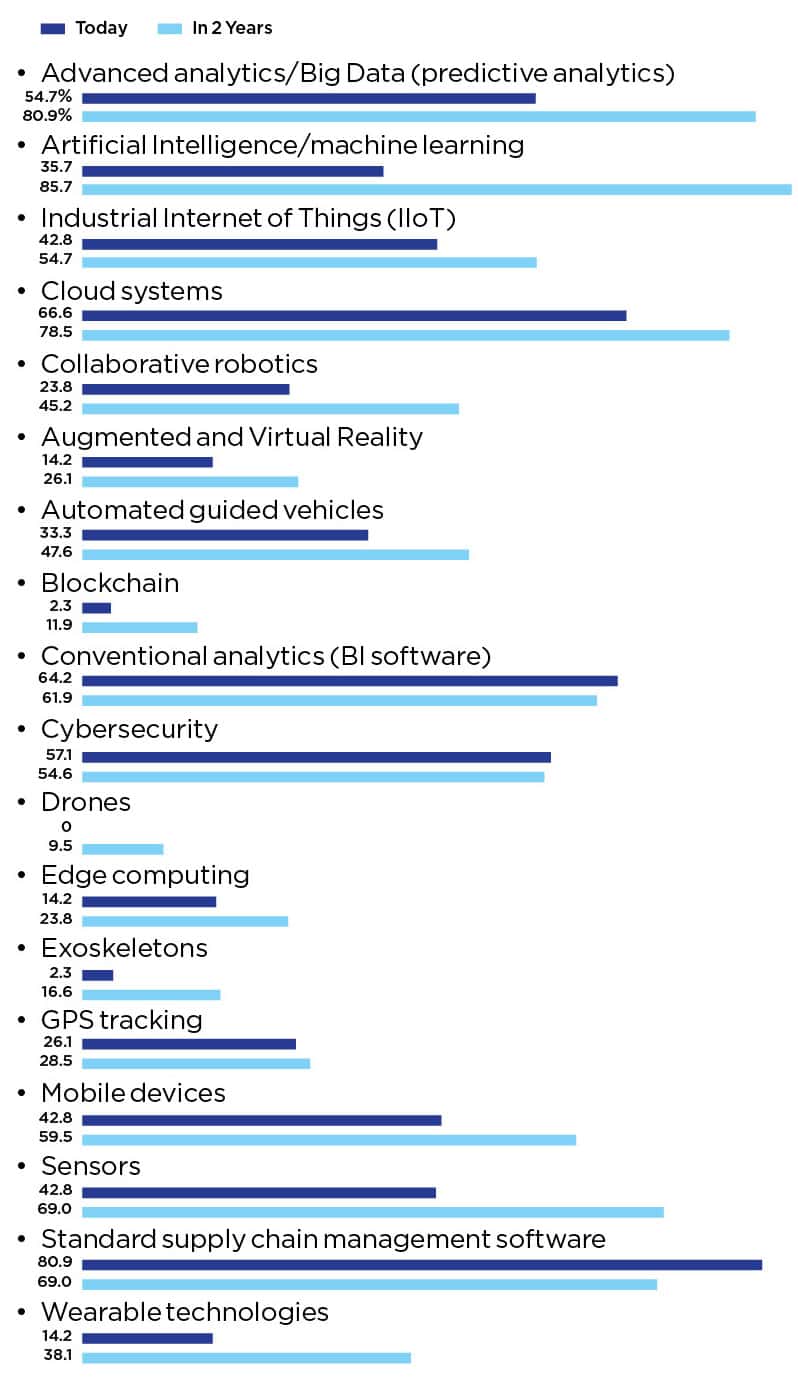

Much the same pattern emerges when survey respondents were asked about the technologies they are deploying to manage their supply chains today and by 2027. Only two technologies – standard supply chain management software and cyber tools – show declines in the next two years, while the rest show, in some cases, very substantial increases.

For example, 54.7% said they are currently using predictive analytics software in their supply chain operations, but by 2027, almost 81% expect to be doing so. Intentions with artificial intelligence and machine learning are even stronger, with 35.7% today rising to 85.7% over the next two years. And more than 80% believe that AI will have a significant impact on their supply chain operations over the next few years (Qs13,14).

13. Increasing Reliance on Technologies Foreseen in Next 2 Years

Q: What technologies are you currently using to digitize your supply chain and what do you expect to be using in two years’ time?

14. Significant Role Foreseen for AI

Q: Looking ahead over the next few years, how significant an impact will AI have on your supply chain?

Opportunities and Challenges

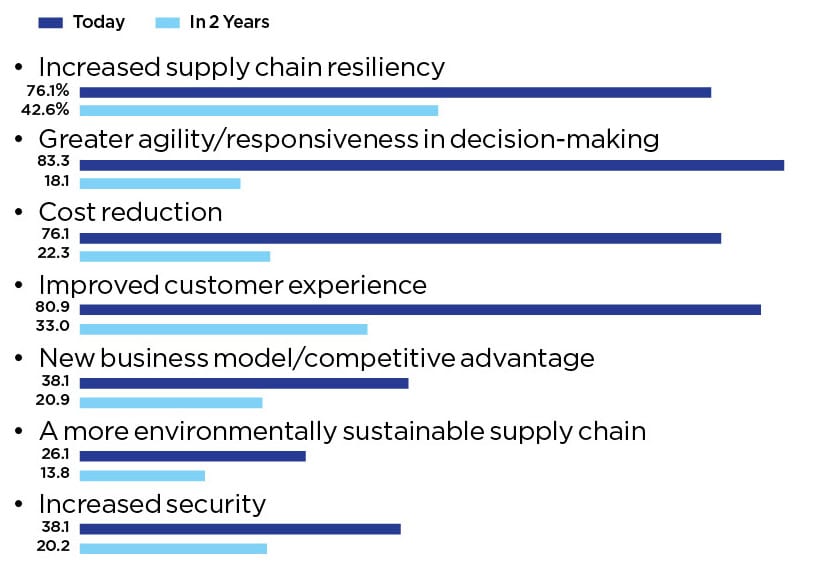

Given the recent experience with the pandemic and the current situation with trade and tariffs, it is not hard to understand why manufacturers are putting so much emphasis on agility, visibility, and resiliency of their supply chains. They have to be able to react quickly to market changes and pivot when necessary. Overwhelming majorities of survey respondents say their top goals are greater responsiveness in decision-making, increased resiliency, cost reduction, and the ability to deliver an improved customer experience (Q15).

15. Agility, Resiliency, Cost Are Top Business Goals

Q: How important are the following business goals associated with your digital supply chain transformation? (Rated high in importance)

But reaching these goals requires streamlined processes and systems that can provide accurate data — and herein lies one of the challenges many manufacturers face.

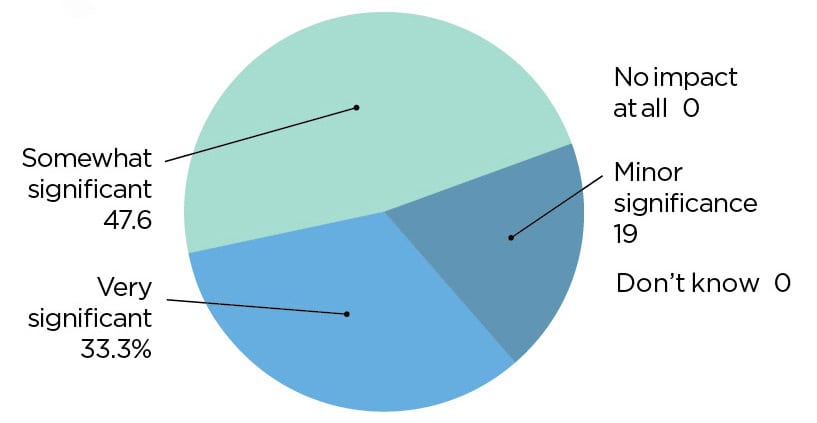

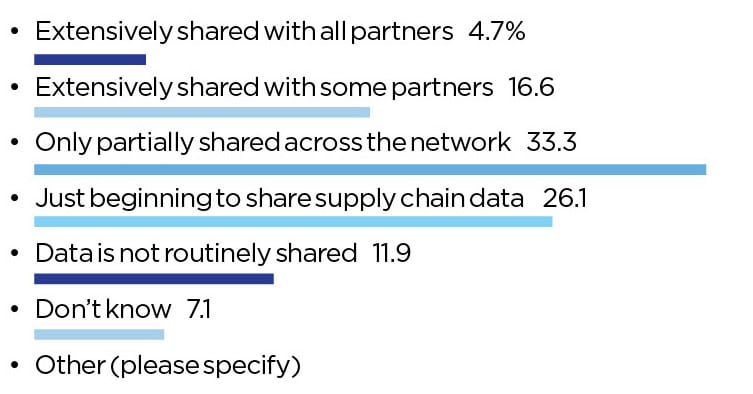

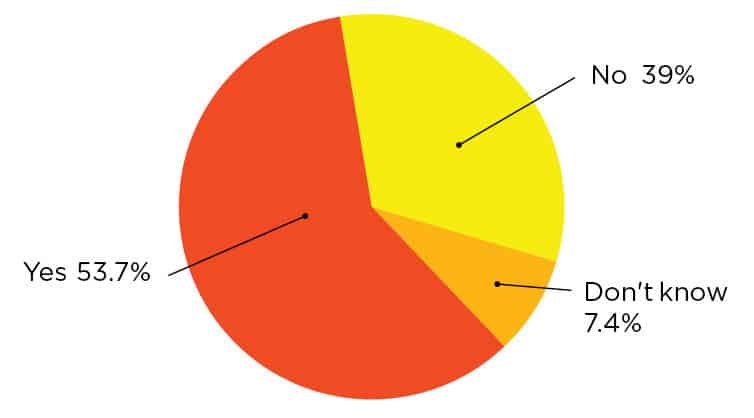

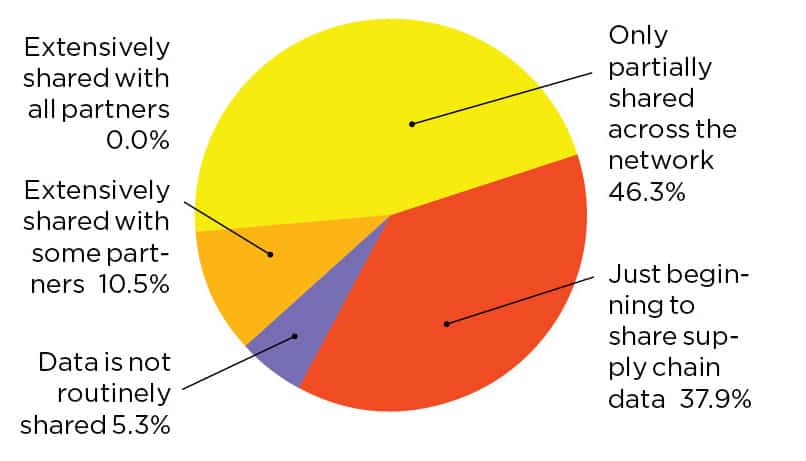

Many companies are still fairly early on in sharing data with partners in their supply networks. Less than one quarter of survey respondents say that data is “extensively” shared with network partners. About one third share data partially across their networks (Q16).

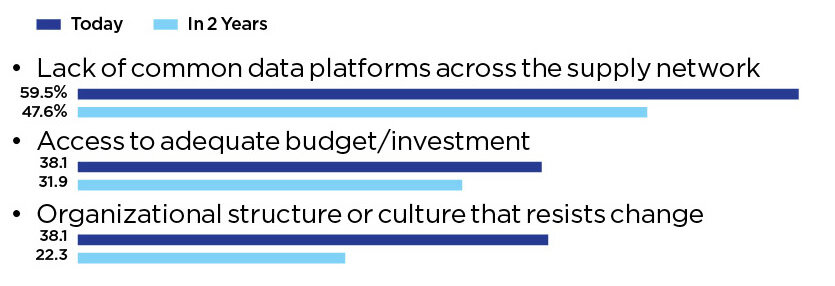

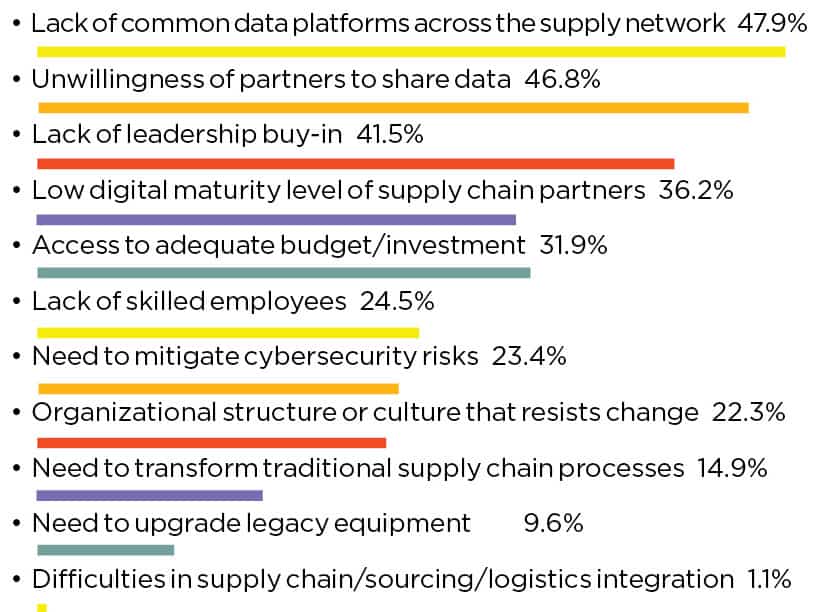

A key reason this is the case, the survey suggests, is a lack of common data platforms in their networks. A strong majority, 59.5%, say the lack of common data platforms is a major challenge in being able to implement an end-to-end digital supply chain strategy (Q17).

If manufacturers need any additional motivation to make progress on this front and achieve the agility and resiliency they desperately need in these turbulent times, they’ve got it now.

16. Data Sharing is Still in its Infancy

Q: To what extent is data routinely shared between any or all of your supply chain partners?

17. Primary Digital Constraint is Lack of Common Data Platforms

Q: What are your company’s primary challenges in implementing an end-to-end digital supply chain strategy? (Top 3)

About the author:

David R. Brousell is the Founder, Vice President and Executive Director, Manufacturing Leadership Council

Survey: M4.0 Appears Poised for A Significant Leap

Manufacturers are ramping up digital investments, with AI, automation, and smart factories reshaping the industry faster than ever.

![]()

KEY TAKEAWAYS:

● Digital transformation is a game changer. Sixty percent see it as a defining shift for the industry, marking a strong rebound in enthusiasm after a dip in 2024.

● Manufacturers digital maturity continues to increase as 75% believe they are at a mid-level maturity—up significantly from the 2024 and 2023 survey results.

● AI expectations have rebounded. A full 80% now fully or partially agree that self-managing and self-learning facilities powered by AI and machine learning are on the horizon.

Manufacturers are charging ahead with their digital transformation efforts. The Manufacturing Leadership Council’s Smart Factories and Digital Production Survey reveals an increase in smart factory maturity and optimism about continued digitization and adoption.

Fueled by an expectation of economic growth and a corresponding plan to increase or maintain smart factory investments, respondents share an outlook that includes AI adoption, end-to-end digitization, and belief that the game changing power of digital transformation is moving beyond mere table stakes.

Section 1: Economic Outlook and Investment Trends

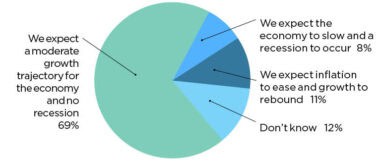

Manufacturers are optimistic about the economy in 2025, with 69% expecting moderate growth and no recession, while only 8% anticipate an economic slowdown. Encouragingly, 11% expect inflation to ease and growth to rebound, signaling greater confidence in market stability. (Chart 1)

This optimism extends to smart factory investments, with 89% of manufacturers planning to maintain or increase spending in 2025. Within that number, it’s notable that 44% expect to ramp up investments, aligning with a broader push for digital transformation. (Chart 2) In the 2024 version of this survey, only 9% expected to increase their Manufacturing 4.0 investment.

Meanwhile, only 8% foresee a decline in spending in 2025, underscoring that despite economic fluctuations, smart factory adoption remains a strategic priority. The data suggests that as confidence in economic growth solidifies, companies are doubling down on automation and digitalization efforts to remain competitive.

1. Strong Majority See Growth on the Horizon

Q: What is your company’s outlook for the economy in 2025? (Select one)

2. 89% see smart factory investments increasing or remaining unchanged

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2025? (Select one)

Section 2: Smart Factory Maturity and Adoption

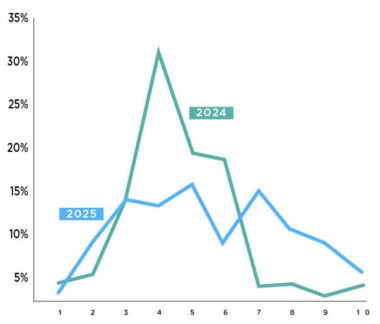

The digital transformation journey continues to advance, with manufacturers steadily maturing their smart factory strategies. Compared to previous years, the percentage of companies rating themselves at lower maturity levels (1-3) has declined significantly, from 57% in 2024 to just 16% in 2025. Meanwhile, those ranking their factories at a mid-level maturity (4-7) increased to 75%—up from 42% in 2024 and 58% in 2023—and 9% now place themselves in the advanced range (8-10). (Chart 3)

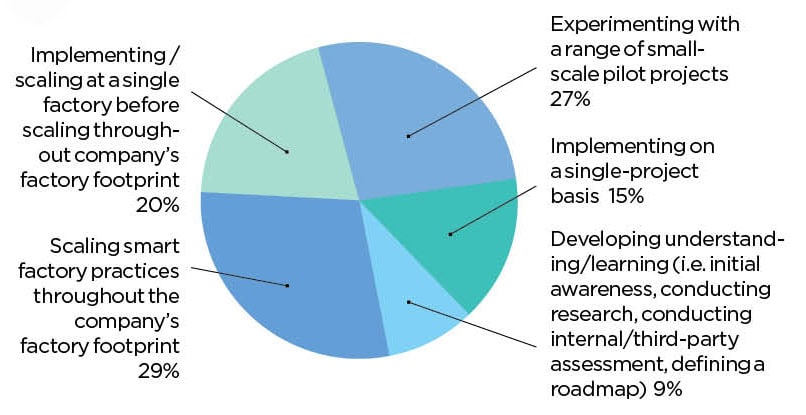

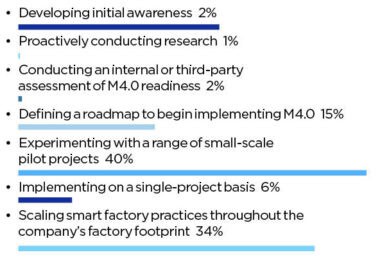

While progress is evident, most companies are still in experimental phases—40% are piloting small-scale projects and 6% are implementing on a single-project basis. Meanwhile, 34% are scaling these initiatives company-wide. Only 15% are just beginning their digital journey, emphasizing a strong industry-wide shift toward implementation. (Chart 4)

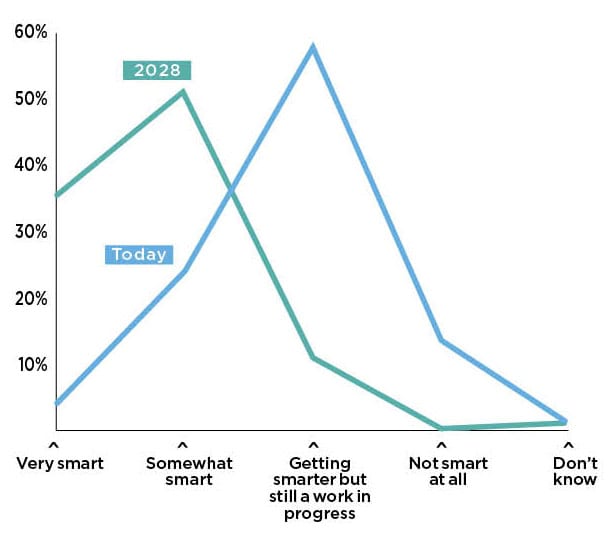

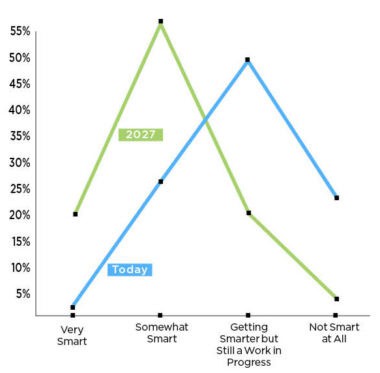

In fact, only 28% believe their factories are very smart or somewhat smart today. That number is expected to skyrocket to 76% by 2027. (Chart 5)

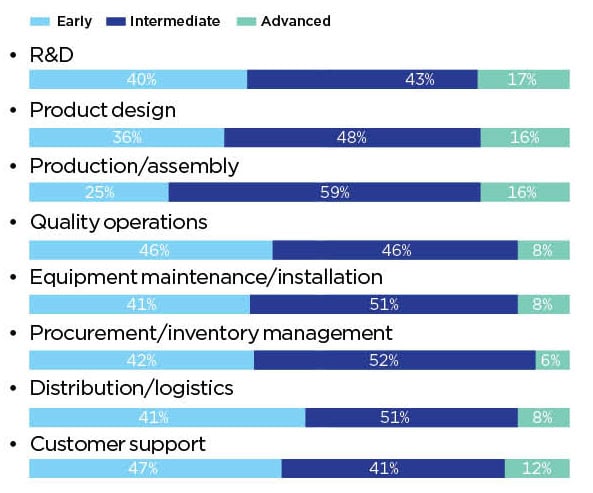

For this to happen, specific functional areas must advance. So it is a positive that manufacturers aspire to reach advanced adoption in every area included in our survey. Many find themselves in the intermediate range, with procurement/inventory management the area most ripe to move from early adoption to this stage. (Chart 6)

Despite this, full integration with business strategy remains a work in progress, with just 24% rating their integration at eight or higher on a 10-point scale, though this is an improvement from 7% in 2024. (Chart 7)

3. Smart factory journeys continue to mature

Q: How would you assess the maturity level of your smart factory journey? (Scale of 1-10, with 10 being the highest level of digital maturity)

4. Most experimenting with small-scale pilots or scaling smart factory practices

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today? (Select one)

5. Smart factory explosion expected by 2027

Q: How “smart” do you consider your factory and plant operations to be today and what do you anticipate they will be by 2027?

6. Manufacturers still striving to reach advanced digital adoption stages

Q: At what stage of digital adoption are the following functions in your company? (Rate as early, intermediate or advanced)

7. Smart factory strategy becoming more integrated with business strategy

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy? (Scale of 1-10, where 10 is fully integrated)

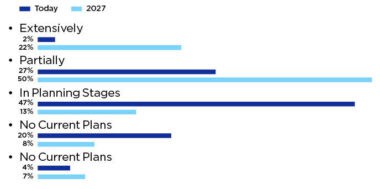

Section 3: Digitization and Automation Growth

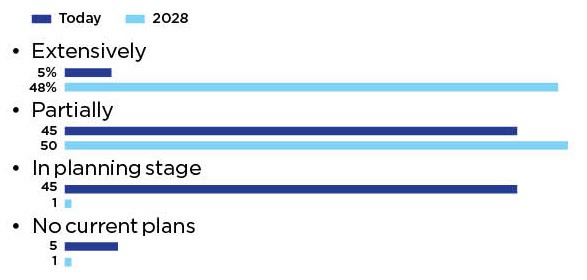

Manufacturers anticipate a significant leap in factory-wide digitization by 2027. Today, only 2% report being extensively digitized, but this is expected to surge to 38% within the next two years. Similarly, partial digitization is set to grow from 47% to 52%, while the number of companies still in planning stages will plummet from 43% to just 5%. (Chart 8)

Production and assembly processes are on a similar trajectory. Only 6% of companies currently consider these processes extensively digitized, but this figure is projected to jump to 45% by 2027. (Chart 9)

Integration with customers and suppliers, however, remains a weak spot—just 2% report extensive digital connectivity today, though 22% expect to achieve this by 2027. (Chart 10)

Taken together, these findings highlight a growing recognition of end-to-end digital transformation as essential for operational agility and supply chain resilience, while identifying an opportunity for improved digitization between manufacturers and their customers and suppliers.

8. Significant end-to-end digitization on the horizon

Q: To what extent are your factory operations fully digitized end to end today, and what do you anticipate they will be by 2027?

9. 92% predict extensive or partial digitization of production/assembly by 2027

Q: To what extent are your production/assembly processes digitized today, and what do you anticipate they will be by 2027?

10. Digital integration with customers and suppliers lags behind in-house digitization

Q: To what extent are your production functions digitally integrated with customers and suppliers today, and what do you anticipate they will be by 2027?

Section 4: Future of Factory Models and AI-Driven Operations

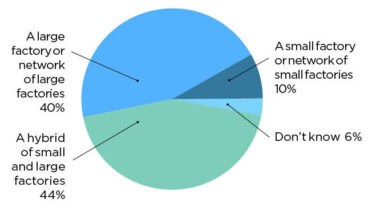

Manufacturers envision a hybrid future for their factory networks, with 44% expecting a mix of small and large facilities, reflecting the need for both localized agility and economies of scale. Large-scale production remains dominant, with 40% favoring large factories or networks of large facilities, while only 10% see a shift toward smaller, more agile production models. (Chart 11)

AI-driven automation is also gaining traction. Almost one quarter (23%) of manufacturers fully agree that factories will evolve into self-managing, self-learning facilities, a dramatic increase from just 6% in 2024. Another 57% partially agree, suggesting growing confidence in AI’s ability to optimize operations. This shift reflects the industry’s increasing focus on AI-driven decision-making and predictive analytics as key enablers of the smart factory vision. (Chart 12)

11. Only 10% see small, agile factories and networks as the future

Q: What is the expected future state of your factory model?

12. Expectation of self-managing, self-learning factories increase significantly

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.”

Section 5: Technology Adoption and Priorities

The 2025 survey highlights strong momentum in advanced technologies, particularly cybersecurity (73% scaling/at scale), IIoT sensor networks (46% scaling/at scale), and advanced analytics (56% scaling/at scale). AI adoption is also accelerating, with 22% of manufacturers now scaling/at scale with AI solutions, and another 42% piloting at least one AI project. Machine learning follows a similar trend, with 21% scaling/at scale and 29% planned for future deployment by 2027. (Chart 13)

AI’s perceived impact is rising sharply—34% now see it as very significant, compared to just 10% in 2024. (Chart 14) This signals a shift from experimentation to real-world application, as manufacturers increasingly leverage AI for predictive maintenance, process optimization, and adaptive automation. However, emerging technologies like the metaverse, blockchain, and exoskeletons remain niche, with over 70% of companies having no plans to adopt any of them. (Chart 13)

13. Cyber, advanced analytics, IIoT sensor networks top production operations tech list

Q: Where does your company stand in regard to the following technologies in its production operations?

14. AI’s expected significance increases

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations?

Section 6: Challenges and Benefits of Digital Transformation

Manufacturers continue to grapple with major roadblocks in their smart factory journeys. Nearly half (49%) cite outdated legacy equipment as their top challenge, up from 39% in 2024, highlighting the complexity of modernization. Workforce-related barriers are also growing—43% point to a lack of skilled employees, a sharp increase from 24% in 2024. Resistance to change remains a persistent issue, with 42% citing organizational culture as a challenge, though this has improved from 53% last year.

But it’s not all bad news. In 2024, a lack of leadership buy-in and access to adequate budget/investment both ranked among the top four roadblocks. Improvements have been seen in both these issue areas. Leadership buy-in and increasing budgets may very well prove to be leading indicators that the current issues discussed above may become lower hurdles rather than roadblocks. (Chart 15)

Despite these current roadblocks, companies recognize the benefits of transformation. Nearly two-thirds (63%) rank operational efficiency as the top expected gain, a significant jump from 40% in 2024. Better decision-making (49%) and cost reduction (44%) follow closely, demonstrating that digital adoption is increasingly seen as a performance and profitability driver. (Chart 16)

Notably, the percentage of companies expecting digital transformation to create a competitive advantage has soared from 11% in 2024 to 38% in 2025. While the majority still see digital transformation as table stakes, the dramatic increase in those who see it as a competitive advantage marks a major shift in strategic thinking. This shift suggests that as adoption accelerates, digital capabilities are becoming key differentiators rather than mere necessities for survival. (Chart 17)

15. Legacy equipment, lack of skilled employees and organizational culture are biggest smart factory roadblocks

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top 3)

16. Better operational efficiency outpaces all other smart factory benefits

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top 3)

17. Digital transformation still seen as table stakes for majority, but increasing number see it as a competitive advantage

Q: Do you believe that digital transformation of your company’s manufacturing operations will create a unique competitive advantage for your company or is it merely table stakes to remain in the game?

Section 7: The Strategic Value of Digital Transformation

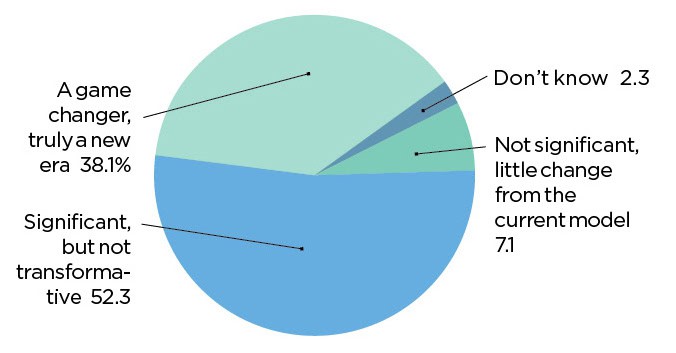

After a dip in enthusiasm in 2024, manufacturers now overwhelmingly see digital transformation as a game-changer—60% believe it signals a new era for the industry, up from just 26% last year. Another 40% still see it as significant but not transformative, while no respondents consider it insignificant. Apart from our 2024 survey, these numbers have remained largely consistent over the past four years. (Chart 18). M

18. After dip in 2024, majority now see digital transformation as a clear game changer

Q: Ultimately, how significant an impact will digital transformation have on the manufacturing industry?

About the author:

Jeff Puma is content director at the NAM’s Manufacturing Leadership Council.

Survey: Leadership Preparedness Improves, but Gaps Remain

MLC’s Digital Leadership survey finds that while more organizations have restructured to build an M4.0 advantage, organizational readiness continues to lag.

![]()

KEY TAKEAWAYS:

● Digital manufacturing leaders need to build traditional leadership qualities with new skills such as fostering a data-driven culture and guiding the workforce through change.

● Despite progress in creating digital strategies, many manufacturers lack formal training programs for upskilling their workforce, and many feel that leadership is unprepared for the future.

● Effective digital leadership is characterized by collaboration both internally and externally, while successfully building and navigating digital ecosystems.

While there are many tried-and-true qualities of good leadership that stand the test of time – innovation, integrity, confidence – the additional skills required of digital manufacturing leaders have evolved just like the technologies giving rise to Manufacturing 4.0.

Today’s operational leaders need an eye toward building data-driven business cultures and decision-making; the ability to collaborate with teams both inside and outside of their organization; the skill to help their teams adapt in times of change; and much more. There are also more traditional leadership skills that look different than they used to; for example, continuous improvement in a digital ecosystem, and a focus on upskilling the workforce on new technologies and methodologies.

The Manufacturing Leadership Council’s 2024 Digital Leadership survey reveals that while organizational structures are adjusting to the needs for digital manufacturing, there are still gaps to address for full business readiness.

Section 1: The Organizational Motto: Be (Mostly) Prepared

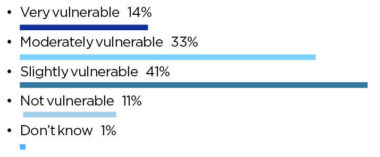

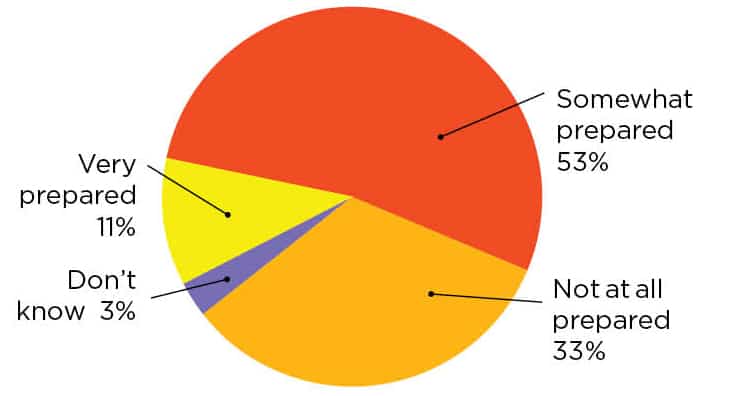

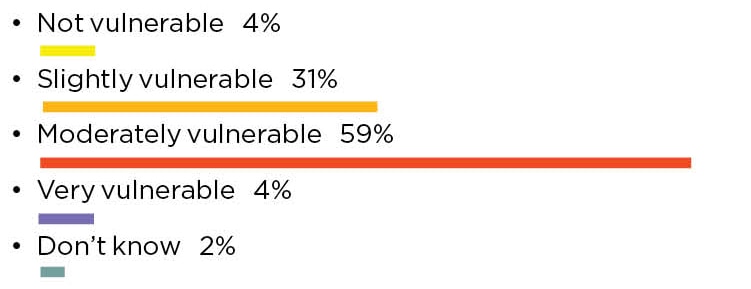

Anyone who has been involved with a scouting organization in their youth is likely to recall the famous motto: “Be Prepared.” It seems that more digital manufacturing leaders, as well as their organizations, are (mostly) coming around to this motto as good advice. But at the same time, more than half of manufacturers are not offering any formal digital training to educate or upskill the workforce and leadership (Chart 3), and 88% of respondents feel that their company’s future has at least some future vulnerability due to its current digital transformation preparedness (Chart 5).

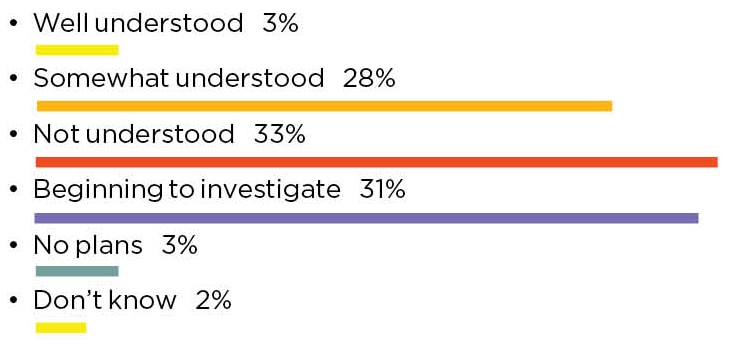

Meanwhile, more organizations have created a change management strategy around digital transformation (Chart 1) and/or have restructured or redesigned themselves to better manage digitalization (Chart 2). But understanding the digital roles and skills that will be required by the future manufacturing enterprise is only somewhat understood by most (Chart 4.)

1. Most Have a Change Management Strategy in Place

Q: Has your leadership team created an organizational change management strategy to help support its digital strategy? (Select one)

2. Organizations are Restructuring Around Digital

Q: As part of its digital transformation work, has your company undertaken organizational redesign to better manage the impact of digitalization? (Select one)

3. Still, Formal Training Programs are Lacking

Q: Does your company have a formal training plan to educate workers and leadership around the requirements of digital transformation? (Select one)

4. Future Roles and Skills Needs Only Somewhat Understood

Q: How well prepared do you think your company is in understanding the new digital roles and skills that you will need in the next few years? (Select one)

5. Current Levels of Digital Readiness Create Vulnerabilities

Q: How vulnerable will your company’s future success be as a direct result of your company’s current level of digital transformation preparedness? (Select one)

Section 2: Digital Leadership is a Team Sport

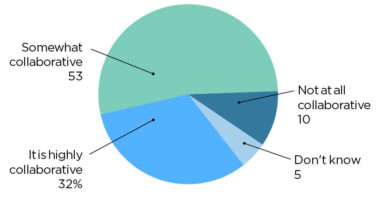

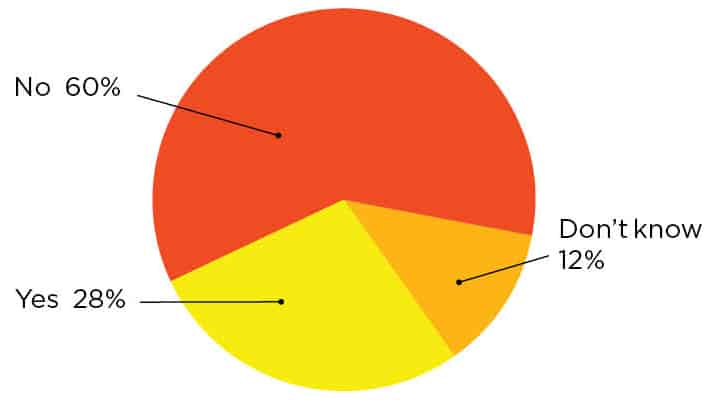

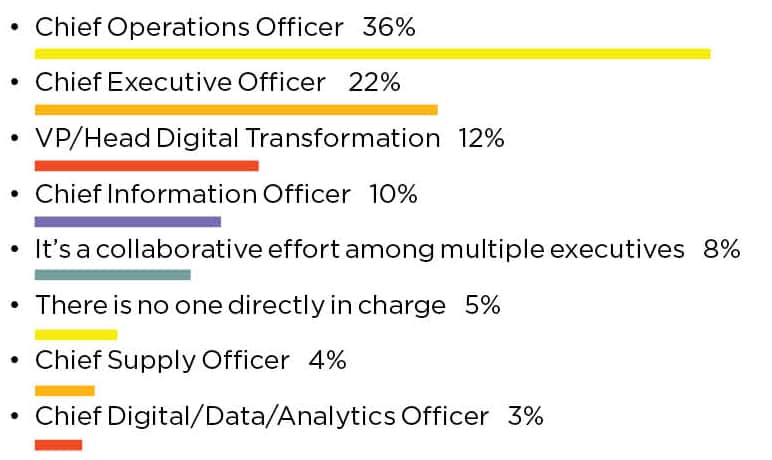

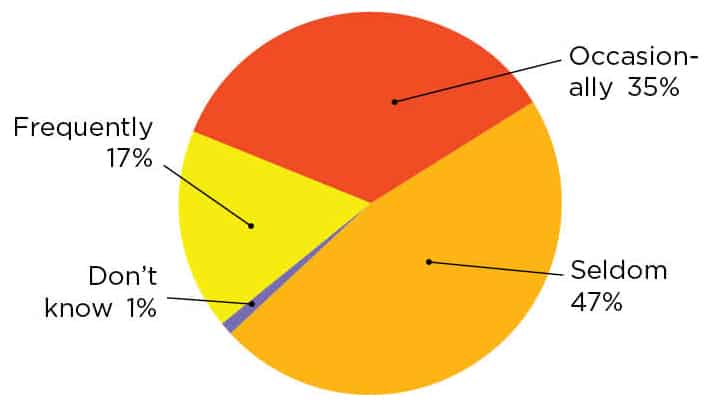

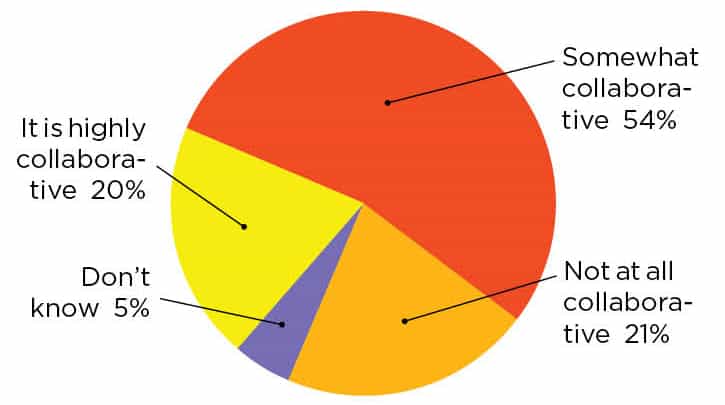

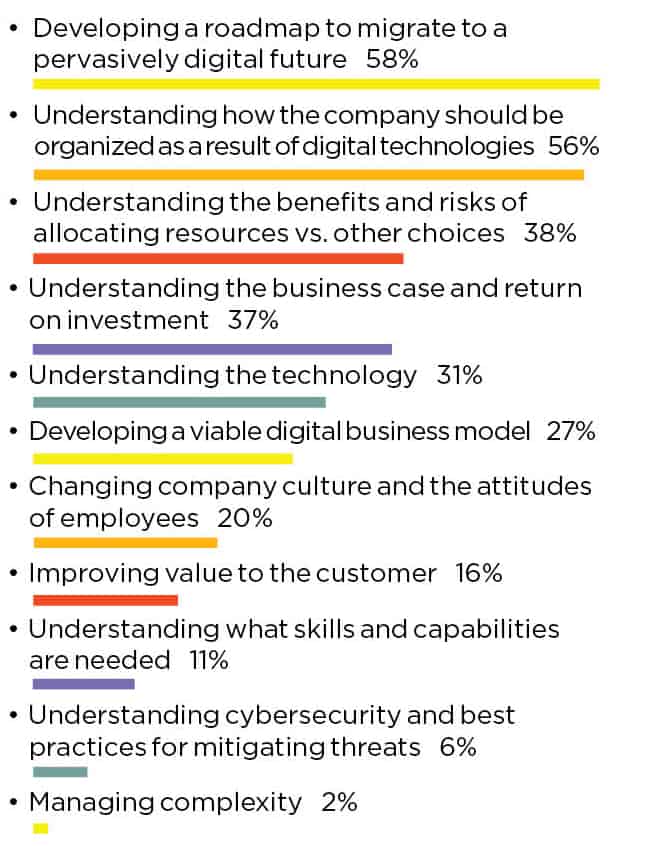

As technology enables individuals and teams to become more connected both internally and to external customers and partners, the ability to collaborate is key. So too is it key among leadership teams, as leaders need to understand the impact that digital investment and deployment will have on different areas of the enterprise. The top response for “who is in charge” for digital transformation efforts was that it is a collaborative effort (Chart 6). It’s likely a positive sign that most respondents — 85% — rates their leadership teams as either “highly” or “somewhat” collaborative (Chart 8).

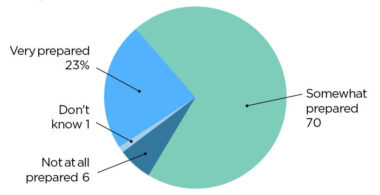

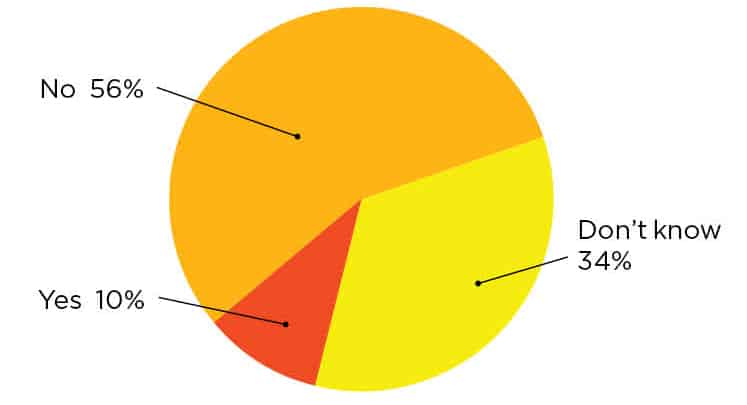

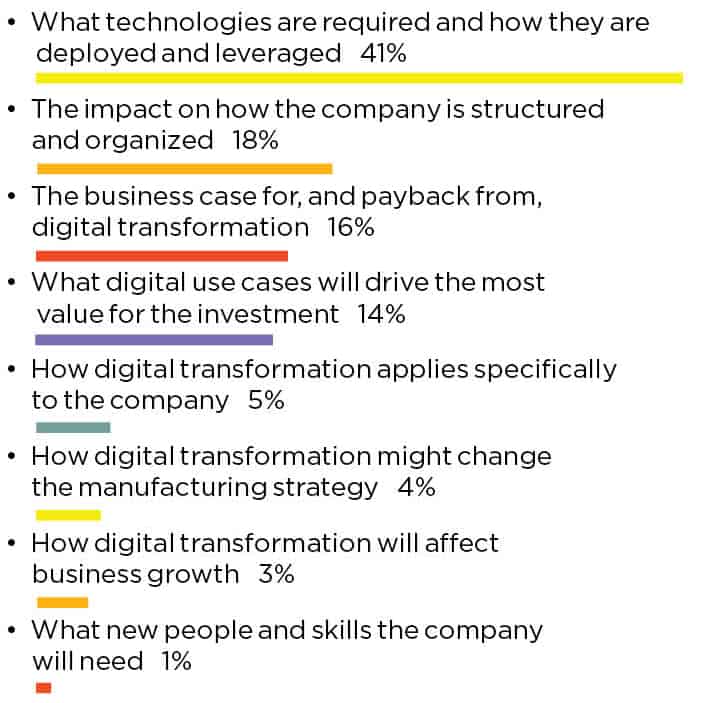

Perhaps unsurprisingly, executive management teams most frequently want to know the value of digital investments – the business case for them, and what specific use cases will bring the most bang for the buck (Chart 7). But only 23% rate their executives as “very prepared” to lead and manage digital transformation (Chart 9).

6. Leadership is Most Often Collaborative

Q: Who is leading the charge around the digital transformation efforts in your organization?

7. Executives Most Often Want to Know Business Value

Q: What is the most important thing your company’s executive management team wants to know about digital transformation? (Select top 3)

8. Cross-Organizational Leaders Collaborate on Strategy

Q: How collaborative is your leadership team across multiple areas of the organization in the development and assessment of its digital strategy? (Select one)

9. Executive Management is Only Somewhat Prepared for Digital Transformation

Q: How prepared do you think your company’s executive management team is to lead and manage digital transformation? (Select one)

Section 3: The Meaning of Leadership in the M4.0 Era

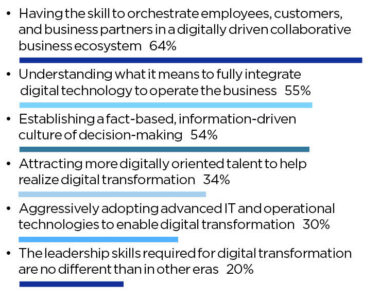

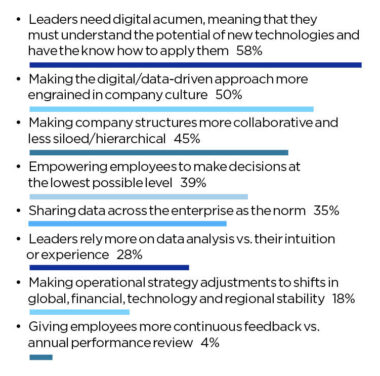

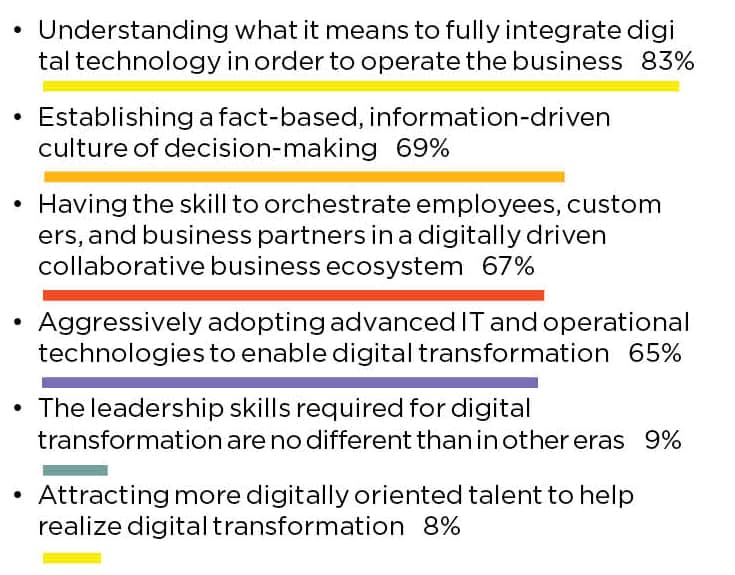

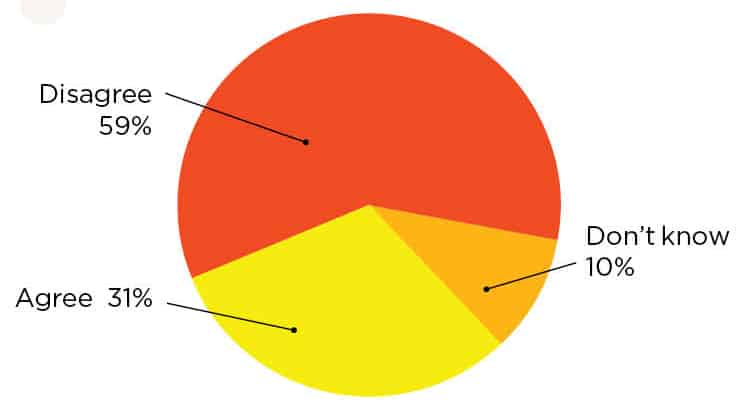

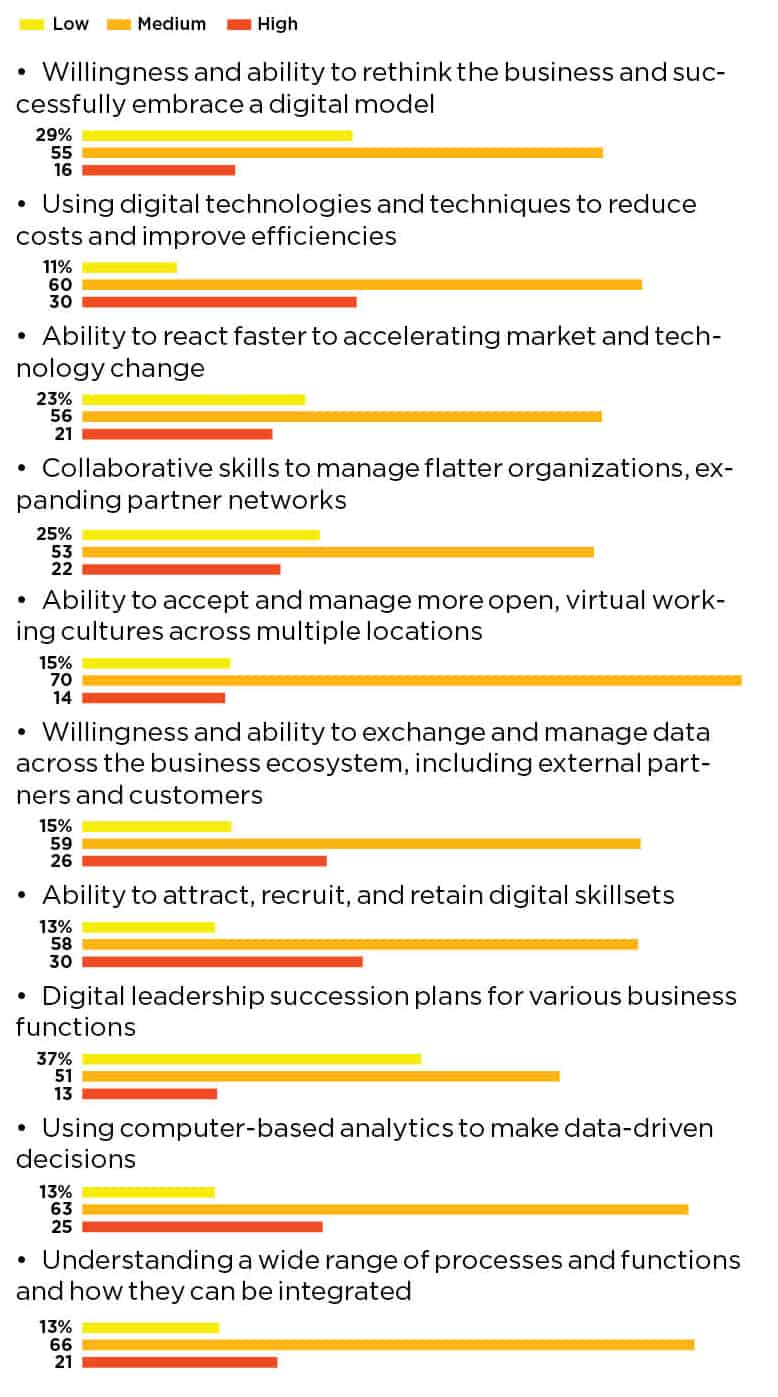

When asked which statements best describe an M4.0 leader, ecosystem-based external and internal collaboration once again came up as a key theme, along with understanding technology integration and creating an information-driven culture (Chart 10). Additionally, most respondents — 74% — believe that digital operations require a substantially different approach and skill set for leaders (Chart 11).

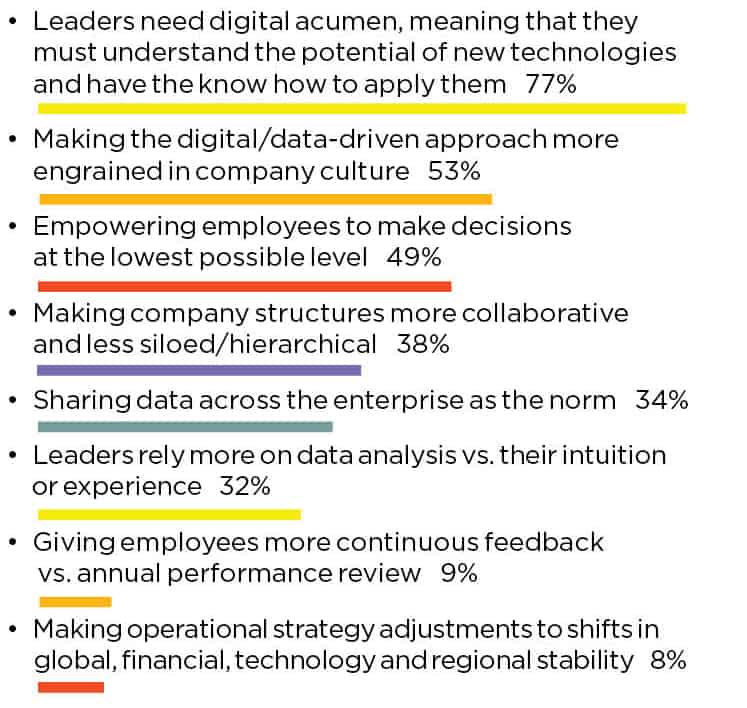

As for the skills and abilities that respondents believe are most important, the highest degree of importance was placed on using digital technology to reduce costs and improve efficiency, followed by the willingness and ability to rethink traditional business to successfully embrace a digital model (Chart 13).

In business, the definition of a good leader has been and will continue to be one who inspires and brings out the best in others, in addition to making smart business decisions to bring about success. Technology is a burgeoning part of the play, but those individuals who dare to act as visionaries in creating winning strategies will continue to be the ones who find success. N

10. Leaders Must Navigate Digital Ecosystems and Understand Digital Integration

Q: Which statements best describe what leadership means in the digital era? (Select top 3)

11. Digital-Era Leadership Requires a Substantially Different Approach

Q: Do you agree or disagree with this statement: The emergence of digitally driven operations and business models will require a substantially different approach and set of skills on the part of manufacturing company leadership. (Select one)

12. Digital Acumen, Building a Data-Driven Culture Most Important for Leaders

Q: Which leadership approaches do you feel are most important in the digital era? (Select top 3)

13. Most Important Skills: Reimagined Business Models; Successful Technology Deployment

Q: Looking ahead, what degree of importance would you assign to the following digital leadership skills and abilities? (Rate each on scale of Low/Medium/High)

About the author:

Penelope Brown Senior Content Director, Manufacturing Leadership Council

Survey: Manufacturers See AI as a “Game-Changer” as They Ramp Up Investments

As they climb up the maturity curve, manufacturers see a host of benefits as well as challenges with AI, says a new MLC survey.

![]()

KEY TAKEAWAYS:

● 78% of surveyed manufacturers say they plan to increase spending on AI tools in the next two years.

● 46% are already using generative AI tools such as Chat GPT or Microsoft’s Copilot in manufacturing operations.

● 55% expect AI to change the rules of the industry by 2030, despite issues with data and a lack of AI-related workforce skills.

Manufacturers are planning significant investments in artificial intelligence technologies, including generative AI tools, in the next two years in order to improve their production capabilities, their decision-making processes, and to generate more predictive insights into operations, even as they struggle with data issues and a lack of AI-related skills in their workforces.

Moreover, most manufacturers are moving ahead with AI in a strategic way, with AI closely aligned with their digital transformation and business strategies. And in looking ahead to 2030 and beyond, a majority of manufacturers expect that AI will be a “game-changer” for the industry that will shape the rules of competition for years to come.

These are some of the top-line findings of the Manufacturing Leadership Council’s new survey on AI in manufacturing. The study explored seven major areas of manufacturers’ involvement with AI. These include the maturity level of AI usage, spending intentions on AI tools including GenAI, how companies have organized around the AI opportunity, what benefits manufacturers are looking for from AI, the impact of AI on the workforce, challenges with AI implementations, and the expected future impact of the technology.

Status of AI Adoption and Spending Plans

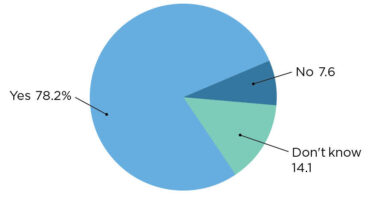

Over the next 12 to 24 months, 78% of surveyed manufacturers said they plan to increase spending overall on AI tools, with one-fifth expecting to increase their AI investments by more than 30%. Regarding GenAI tools such as Chat GPT or Microsoft’s Copilot, nearly half of survey respondents are currently using these tools in their manufacturing operations and more than 80% said they expect to increase their use in the next two years (Charts 1, 2, 3).

1. Strong Majority to Increase AI Spending

Q: Does your company plan to increase spending on AI tools in the next 12 to 24 months?

2. GenAI Tools Already in Wide Use

Q: Are you currently using GenAI tools such as ChatGPT or Microsoft Copilot in manufacturing operations?

3. More Than 80% Will Increase GenAI Usage

Q: What are your plans for GenAI tools in the next two years?

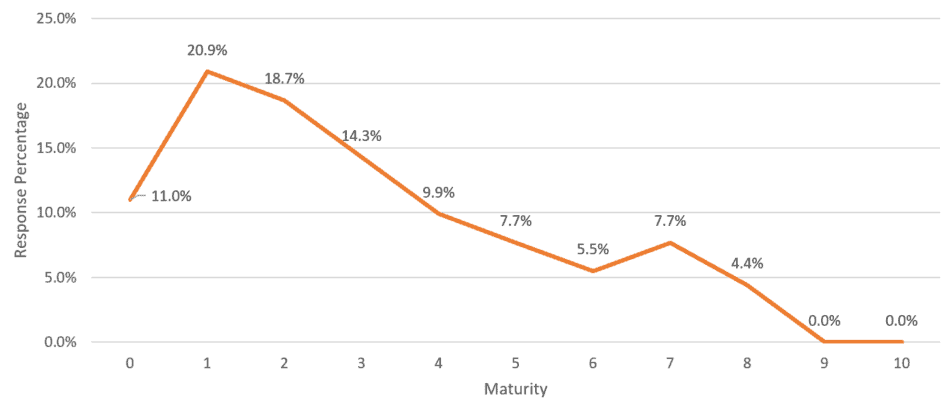

Should these investment intentions pan out over the next two years, they will do so against a backdrop of experience with AI that is at an early stage in most companies. Overall, survey respondents indicated that their level of maturity with AI tools in manufacturing operations is nascent (Chart 4). For example, only 5.4% of respondents assessed the maturity of AI tool usage in their manufacturing operations as “advanced”, with 66% indicating it is at an “early” stage and 28% at a “moderate” stage. The findings are similar across 14 other corporate functions, including supply chain, research and development, and quality operations, surveyed by MLC.

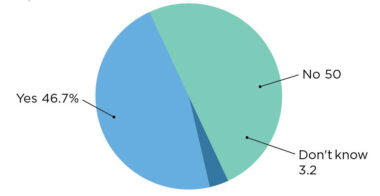

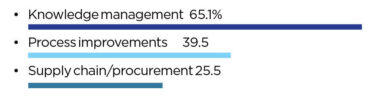

This may change as the pace of experience with AI picks up. The adoption of GenAI tools such as Chat GPT and Microsoft Copilot has been remarkable. Currently, 46.7% of survey respondents indicate they are using GenAI tools in knowledge management, to help identify process improvements, in quality operations, and in preventative and predictive plant floor equipment maintenance (Chart 5).

More than one-third of respondents say they plan to substantially increase the use of GenAI tools over the next two years. Another 49% say they are planning a moderate increase in usage of these tools. And a majority, 52.7%, say they will do so according to corporate policies that have been established on the selection and use of GenAI tools (Chart 6).

4. Manufacturing Operations AI Tools are Nascent

Q: Overall, how would you characterize the present maturity of artificial intelligence usage in your company’s manufacturing operations? (on a scale of 1-10, with 10 being the highest level of maturity)

5. Knowledge Management is Primary Area of GenAI Usage

Q: If yes, in which areas have you implemented generative AI? (top 3)

6. A Majority Have a Corporate Policy on GenAI

Q: Has your company established a corporate policy on the selection and use of GenAI tools?

AI Strategy and Organization

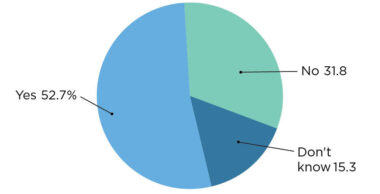

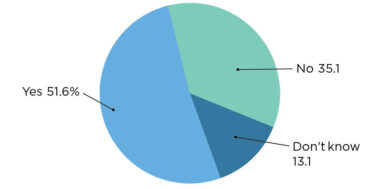

Perhaps a result of many years of using traditional AI tools such as business intelligence and machine learning technologies, most manufacturers say their companies have a corporate AI strategy (Chart 7). Moreover, 78% say their AI initiatives within manufacturing operations are part of their company’s larger digital transformation and business strategies (Chart 8).

In addition, a substantial percentage of survey respondents, 42.8%, say that their company’s AI governance process is part of their overall data governance strategy. Nearly 20% indicate that they have an AI governance strategy but that it is not part of data strategy, while 27% say their companies do not have an AI governance strategy at all.

But when it comes to being able to identify who or what corporate unit oversees AI initiatives, the lines are blurry. The chief information officer was cited by just over 21% of respondents as the corporate officer in charge of AI initiatives, but an equal number of respondents say that authority is unclear in their companies. Given the proliferation of technology-oriented executive titles and functions in recent years, it is perhaps not surprising that involvement and even responsibility for AI projects has crossed organizational boundaries in many companies (Chart 9).

7. Manufacturers Are Thinking Strategically About AI

Q: Does your company have a corporate AI strategy?

8. Digital, AI Linked in Vast Majority of Companies

Q: Are your AI initiatives within manufacturing operations part of a larger digital transformation strategy for your company? (select one)

9. The CIO is Most Often in Charge of AI

Q: Organizationally, who or what department is in charge of AI initiatives in your company?

Expected Benefits of AI

At the end of the day, what benefits are manufacturing companies looking to get out of their investments in AI? The answers are to be found in the rapidly increasing volumes of data companies are generating from their extensively connected businesses.

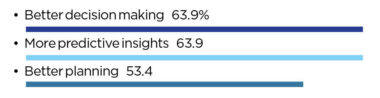

When asked to assess a list of 11 potential business benefits using a low/moderate/high scale, the three potential benefits that motivated a strong majority of respondents for their “high” potential were more predictive insights from data, better decision making, and better planning (Chart 10).

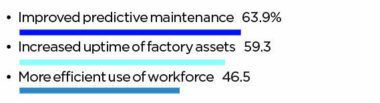

In operations, the three potential benefits scoring a “high” ranking were improved predictive maintenance, increased uptime of factory assets, and a more efficient use of the workforce. In the supply chain category, the three were better supply chain planning, more predictive insights, and increased supply chain agility (Chart 11).

Aspirations aside, one of the disciplines that manufacturers will have to get better at as their experience with AI matures is measuring effectiveness. Currently, 66% of respondents say their companies do not have a specific set of metrics to measure the effectiveness and impact of AI implementations (Chart 12).

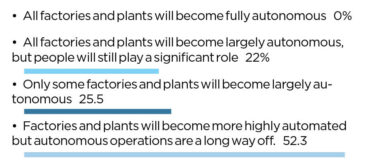

Although the prospect of AI-supported autonomous factory and plant operations is being widely discussed in the industry today, survey respondents take a nuanced view of the concept. The idea of “fully autonomous” operations is a foreign one, but noteworthy percentages of respondents do expect a substantial degree of autonomy to be achieved in their plants and factories in the distant future (Chart 13).

10. Better Insights, Decision Making Are Top Business Benefits

Q: How would you assess the potential business benefits of AI in your company ? ( top 3 benefits ranked by highest level of response)

11. Maintenance, Uptime Seen as Operational Benefits

Q: How would you assess the potential benefits of AI in manufacturing operations? ( top 3 benefits ranked by highest level of response )

12. Most Do Not Have AI Metrics

Q: Do you have a specific set of metrics to measure the effectiveness and impact of AI implementations?

13. A Majority Believes that Autonomous Plants Are in the Distant Future

Q: What statement would best describe your expectation about the future state of factories and plants as a result of the use of AI by 2030?

AI’s Effect on the Manufacturing Workforce

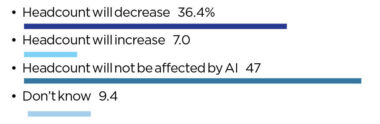

As other MLC studies have previously indicated, manufacturers are largely not buying into the fear that AI adoption will result in widespread worker displacement. Nearly one half of survey respondents, 47%, do not expect their company’s workforce headcount to be affected by AI. However, just over one third, 36.4%, do expect that headcount levels will decrease, and seven percent expect that headcount will increase because of AI adoption (Chart 14).

For those expecting some workforce displacement, 56% say that those displaced will be retrained or reassigned to one degree or another, with 22% saying that 20% of more of those displaced will be offered other opportunities.

14. Nearly a Majority See No AI Effect on Workforce Levels

Q: What impact do you think AI will have on your workforce headcount by 2030?

AI Challenges, Policy Considerations, and Future Impact

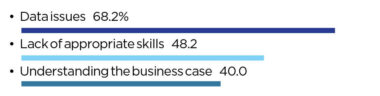

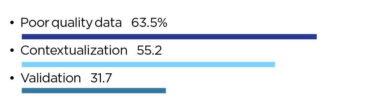

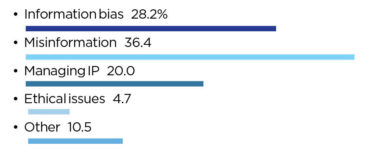

As it is with any IT or OT technology, there are always challenges associated with their implementation and use. By far the most significant challenge with AI has to do with data, say 68% of survey respondents, with data quality, validation, and contextualization at the top of their punch lists (Chart 15, 16). The lack of AI-related skills in the workforce and understanding the business case for AI were also cited as key challenges.

Although it did not make the top three challenges indicated by survey respondents, embedded bias in algorithms was cited by one-fifth of survey takers as an issue. Misinformation was also cited as a key risk factor (Chart 17).

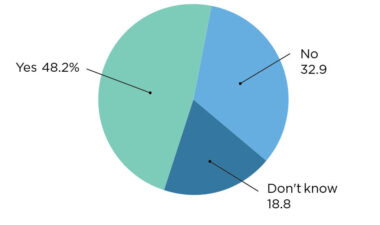

On the question of whether the U.S. should have a federal-level industrial policy on AI, nearly half of survey respondents are in favor of such a policy. Furthermore, nearly half also support regulation of AI by the federal government (Charts 18,19).

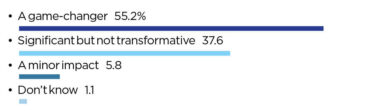

And, for the first time on a question that has been asked in previous MLC surveys, a majority of respondents now feel that AI will be a “game-changer” for the industry in the future (Chart 20).

Just how fast that future could arrive will no doubt be on the minds of manufacturing executives as they think about how to remain competitive in the years ahead.

15. Data Issues Are the Biggest Challenge with AI

Q: What do you see as the biggest challenges to AI adoption and use?

16. Data Quality, Contextualization Are Top Challenges with AI Data

Q: What areas of working with AI-related data are proving most challenging?

17. Misinformation is Seen as the Biggest Risk with AI

Q: What do you see as the most significant risk in using AI?

18. Nearly a Majority Are in Favor of a Federal AI Policy

Q: Should the U.S. have a federal-level industrial policy to encourage AI development and adoption?

19. Nearly Half Favor Federal Regulation of AI

Q: Do you think AI should be regulated by either the states or the federal government? (select one)

20. Most See AI as A Game-Changer for the Industry

Q: Ultimately, how significant an impact will AI have on the industry by 2030 and beyond?

About the author:

David R. Brousell is the Founder, Vice President and Executive Director, Manufacturing Leadership Council

Survey: Smart Factories Are Still a Work in Progress

Manufacturers are moving ahead with creating smarter factories as they grapple with cultural resistance and integrating new technologies.

![]()

TAKEAWAYS:

● A majority of manufacturers say their investments in M4.0 technologies to create smart factories will continue unchanged this year.

● Most manufacturers are at an intermediate stage with M4.0 adoption.

● The most significant roadblock to implementing a smart factory strategy is an organizational structure or culture that resists change.

Tracking the evolution of factories and plants to become so-called smart facilities is a bit like trying to discern the movement of a glacier. You can watch intently but it is hard to detect change. And when change does occur, it is measured in inches. But like a glacier, over time the movement to smart factories and plants will encompass all a production facility does and in a profound way.

The manufacturing industry is inexorably marching toward a day when smart factories and plants, powered by intelligent, sensor-based networks that generate vast volumes of data that are analyzed by artificial intelligence systems, will operate with less human intervention. Highly automated, increasingly intelligent and flexible, the smart factory of the future beckons.

As we head toward that promised land, we look for markers along the way, indications that may tell us where we are making progress and where the obstacles to that progress may lie. The Manufacturing Leadership Council’s new Smart Factories and Digital Production survey sheds light on those markers.

Section 1: STATUS OF DIGITAL INVESTMENT AND ADOPTION

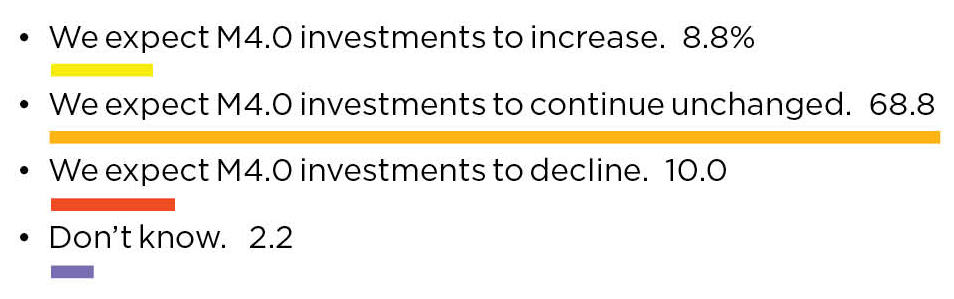

At the highest level, the industry’s posture with regards to investing in Manufacturing 4.0 technologies to create smart factories appears to be on solid footing. In the new survey, nearly 69% of respondents indicated that their M4.0 investments this year would continue unchanged from last year. Nearly 19% said they would increase investments and only 10% said their investments would decline (Chart 1). Concerns about a recession have evidently eased.

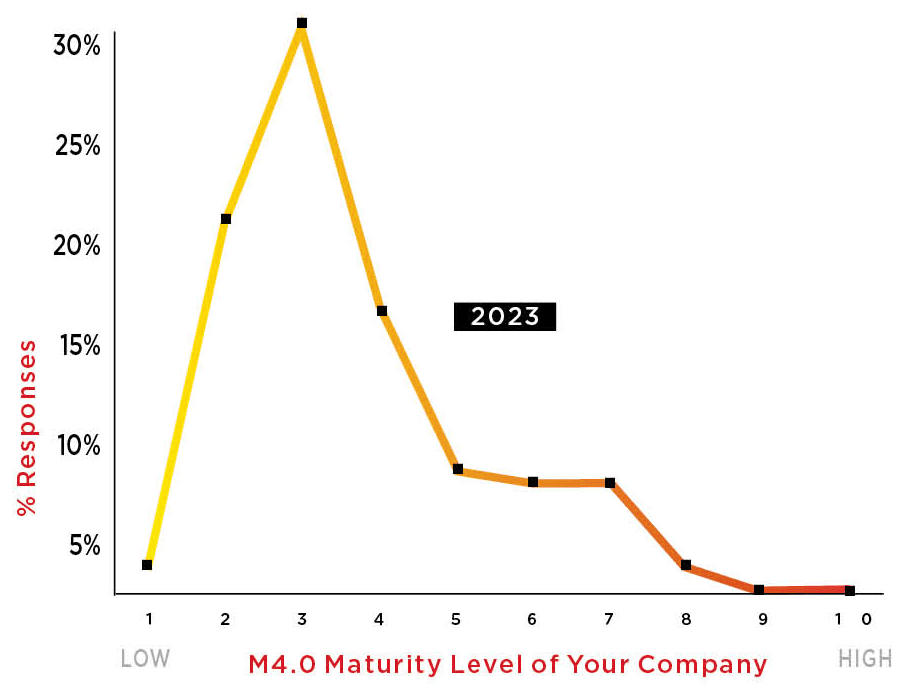

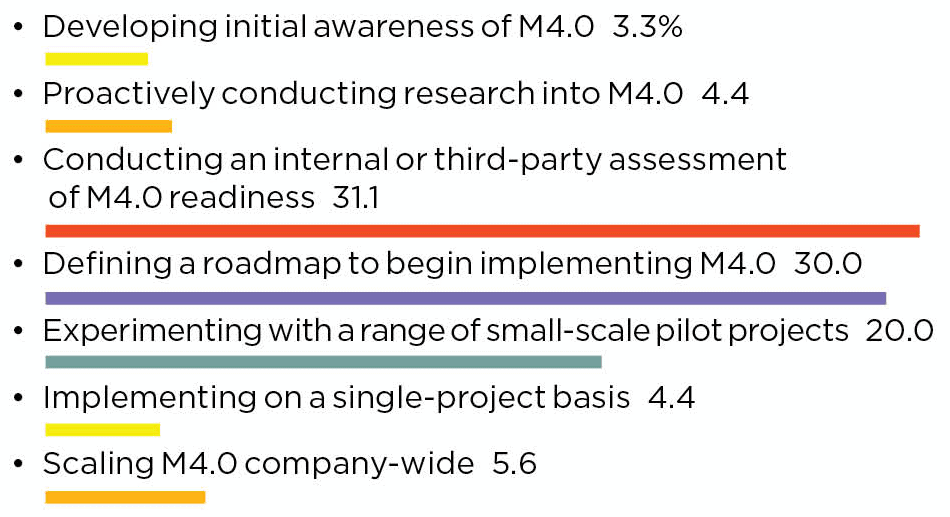

As manufacturers continue to invest in digitalization, they have moved from the initial stages of developing awareness and conducting research into M4.0 to action. Thirty percent of the respondents to the survey say they implementing small-scale pilots, experimenting with a range of projects, or scaling M4.0 companywide. Interestingly, about 31% report they are at the stage of conducting M4.0 readiness assessments, which, when completed, should spawn many pilots and projects (Chart 3).

“The manufacturing industry is inexorably moving toward a day when smart factories and plants …will operate with less human intervention.”

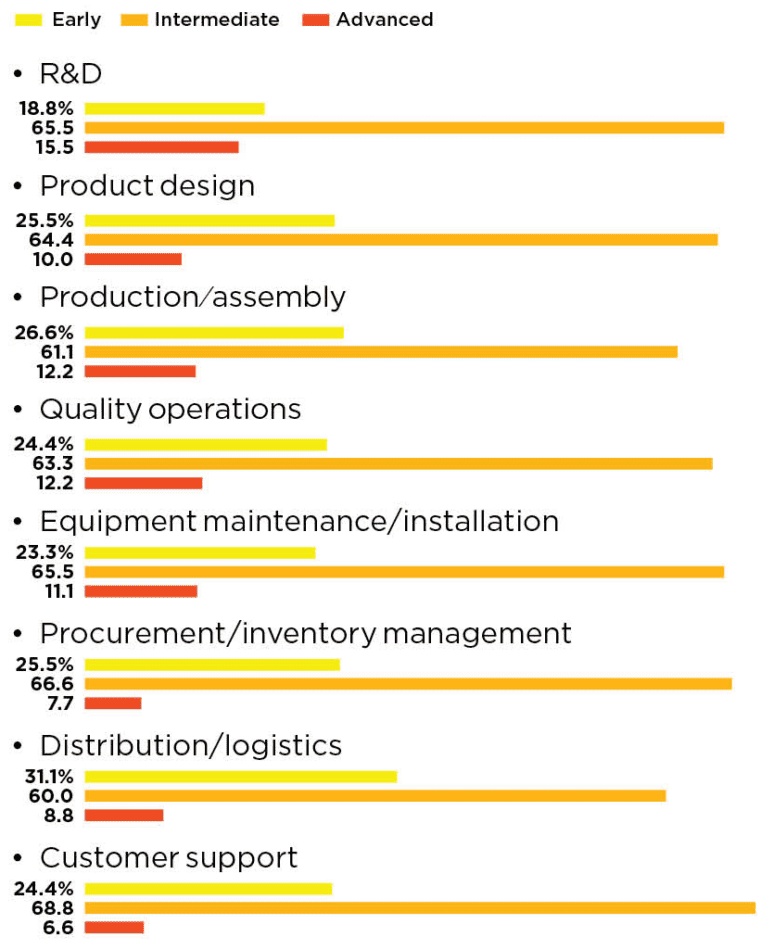

When looked at the stage of adoption functionally – in R&D, product design, and in production and assembly, for example – a strong majority of respondents say they are at an “intermediate stage” with M4.0. Those at an “advanced” stage represent only single-digit or low double-digit constituencies (Chart 4).

Overall, when respondents were asked to assess the digital maturity level of their manufacturing operations, about 58% said that, on a scale of one to 10, they are in the three to five range, which supports the view that the industry has moved beyond the initial stages of M4.0 and is approaching an early majority of those embracing the digital model (Chart 2).

1. Economy Notwithstanding, Strong Majority Sees No Change to M4.0 Investments

Q: How do you expect your company’s outlook for the economy to influence M4.0 smart factory and production technology investments for 2024?

2. Nearly Half Are in Early Stage of Digital Maturity

Q: How would you assess the digital maturity level of your manufacturing operations?

3. Readiness Assessments, Roadmaps Dominate Stage of M4.0 Efforts

Q: Which activity best describes the primary stage of your company’s M4.0 digital efforts today?

4. Functionally, Most Firms Are in the Middle Stage of Digital Adoption

Q: At what stage of digital adoption are the following functions in your company?

5. Few Have Fully Integrated Smart Factory Strategies With Business Strategies

Q: To what extent has your smart factory strategy been integrated with the company’s overall business strategy?

Section 2: MEASURING DIGITIZATION

Not surprisingly, only a fraction of manufacturers, 6.8%, report that they have “extensively” digitized their factory operations today. Most have either partially digitized or are in the planning stages of doing so. But when asked to anticipate the extent of digitization by 2026, 14.7% said they expect to be extensively digitized on an end-to-end basis in that timeframe (Chart 6).

Correspondingly, only a fraction of respondents, 4.5%, would be ready to say their factories are “very smart” today, but, once again, aspirations are high. By 2026, 11.3% expect to be able to affix that label to their operations. But for the moment, a majority of respondents, 53.4%, say their factories and plants are getting smarter but are still a work in progress (Chart 7).

6. More Fully Digitized Operations on the Horizon

Q: To what extent are your factory operations fully digitized end to end today, and what do you anticipate they will be by 2026?

7. “Smart” Factories Still a Work in Progress

Q: How “smart” do you consider your factory and plant operations to be today?

Section 3: FACTORY ORGANIZATION AND MANAGEMENT

So where is all this digital work heading? What do manufacturers expect their factory models to look like in the years ahead?

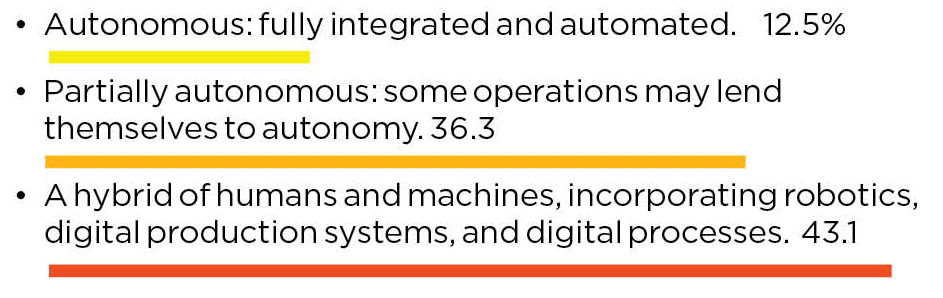

The idea and prospect of some level of autonomous operation is clearly on radar screens. Nearly half of the respondents, 48.8%, expect their future factory models to be autonomous, defined as fully integrated and automated, or partially autonomous, defined as some operations or processes conducted autonomously (Chart 8).

8. Autonomous Operations is on the Radar Screen

Q: What is the expected future state of your factory model?

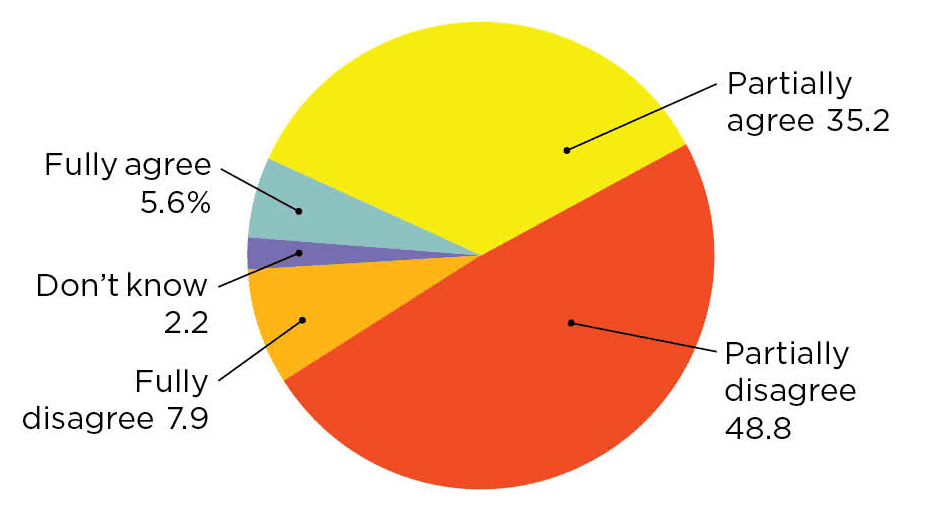

9. A Majority Does Not See Self-Learning Factories in the Future

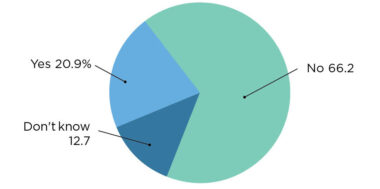

Q: Thinking about the impact of technologies such as AI and machine learning, to what extent would you agree or disagree with the following statement: “Tomorrow’s factory will evolve to be a self-managing and self-learning facility.”

Section 4: TECHNOLOGY USAGE

There is an expanding basket of advanced technologies manufacturers will be using to create their smart factories and plants.

When asked about adoption status on 21 technologies, the most striking thing was how strong planned adoption was by 2026. Eight of the technologies surveyed – for example, machine learning, edge computing, digital threads, AR/VR, and Metaverse technologies – all received 60% or higher planned adoption responses. Eight others garnered 50% or higher responses (Chart 10).

Interestingly, there is a split within the respondent base as to how significant an impact AI will have in operations, perhaps reflecting the still early stage of usage in many companies. Only 40% say that AI will be either very significant or somewhat significant, while nearly half, 49.4%, see AI as playing a minor role in the next few years (Chart 11)..

While it may be obvious that it takes a multitude of technologies to create a smart factory, the underlying message is that real power of being smart will only be realized when these technologies are integrated within the factory. That’s a whole new level of work ahead for manufacturers.

10. Strong Aspirations for a Basket of Technologies by 2026

Q: Where does your company stand in regard to the following technologies in its production operations?

11. Views on AI Significance Diverge

Q: Looking ahead over the next few years, how significant an impact will AI have on your production operations?

Section 5: M4.0 OPPORTUNITIES AND CHALLENGES

Manufacturers also expect a basketful of benefits from creating smart factories and plants. Although there is no breakout factor, cost reduction, greater customer satisfaction, and higher financial returns top the list of expected benefits.

But when it comes to roadblocks in implementing a smart factory strategy, there is clearly a breakthrough factor – organizational structure or culture that resists change. More than 55% of respondents cited this factor as the primary issue in realizing their smart factory vision, considerably higher than a lack of skilled employees, cybersecurity issues, or the need to upgrade legacy equipment (Chart 12).

This may be why, when asked how well their smart factory strategies have been integrated with their company’s business strategy, very few respondents indicated that these two things were fully integrated (Chart 5).

As the famed management consultant Peter Drucker once said: “Culture eats strategy for breakfast.”

Is that glacier moving? M

12. Culture is Biggest Roadblock to Smart Factories

Q: What do you feel are your company’s primary roadblocks to implementing your smart factory strategy? (Select top 3)

13. Cost Reduction, Customer Satisfaction Chief Desired Benefits

Q: What are the most important benefits and opportunities your company hopes to realize from embracing a smart factory strategy? (Select top 3)

About the author:

David R. Brousell is Founder, Vice President, and Executive Director at the NAM’s Manufacturing Leadership Council.

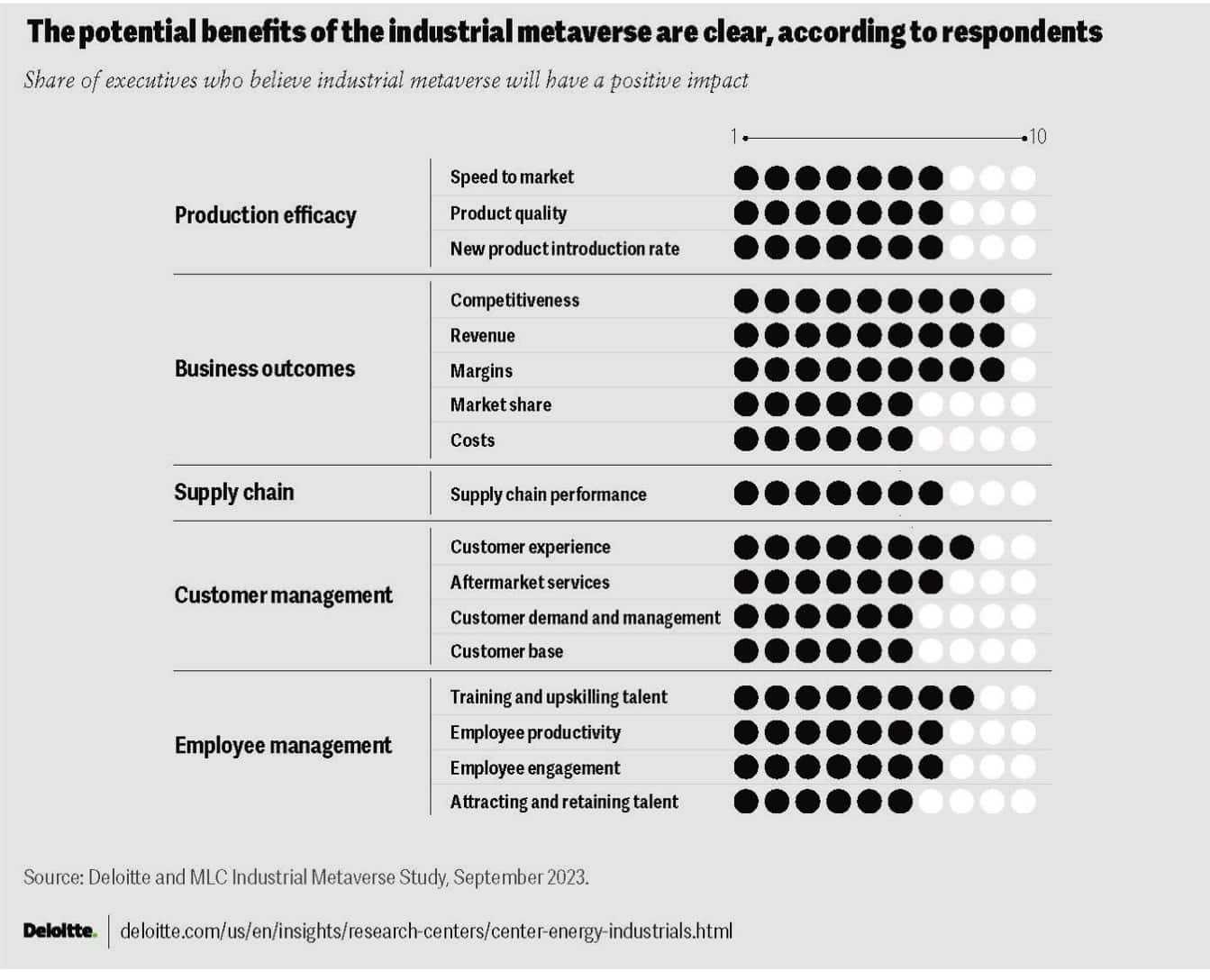

The Industrial Metaverse May Be Closer Than You Think

Nearly 80% of manufacturing executives seem confident that the metaverse will transform aspects of manufacturing in the next five years, a new Deloitte/MLC study reveals.

![]()

TAKEAWAYS:

● Executives say that the Industrial Metaverse offers new ways to solve a variety of pressing challenges they face in the near term.

● Attracting and retaining top talent and building resilience and visibility in supply chains are top goals.

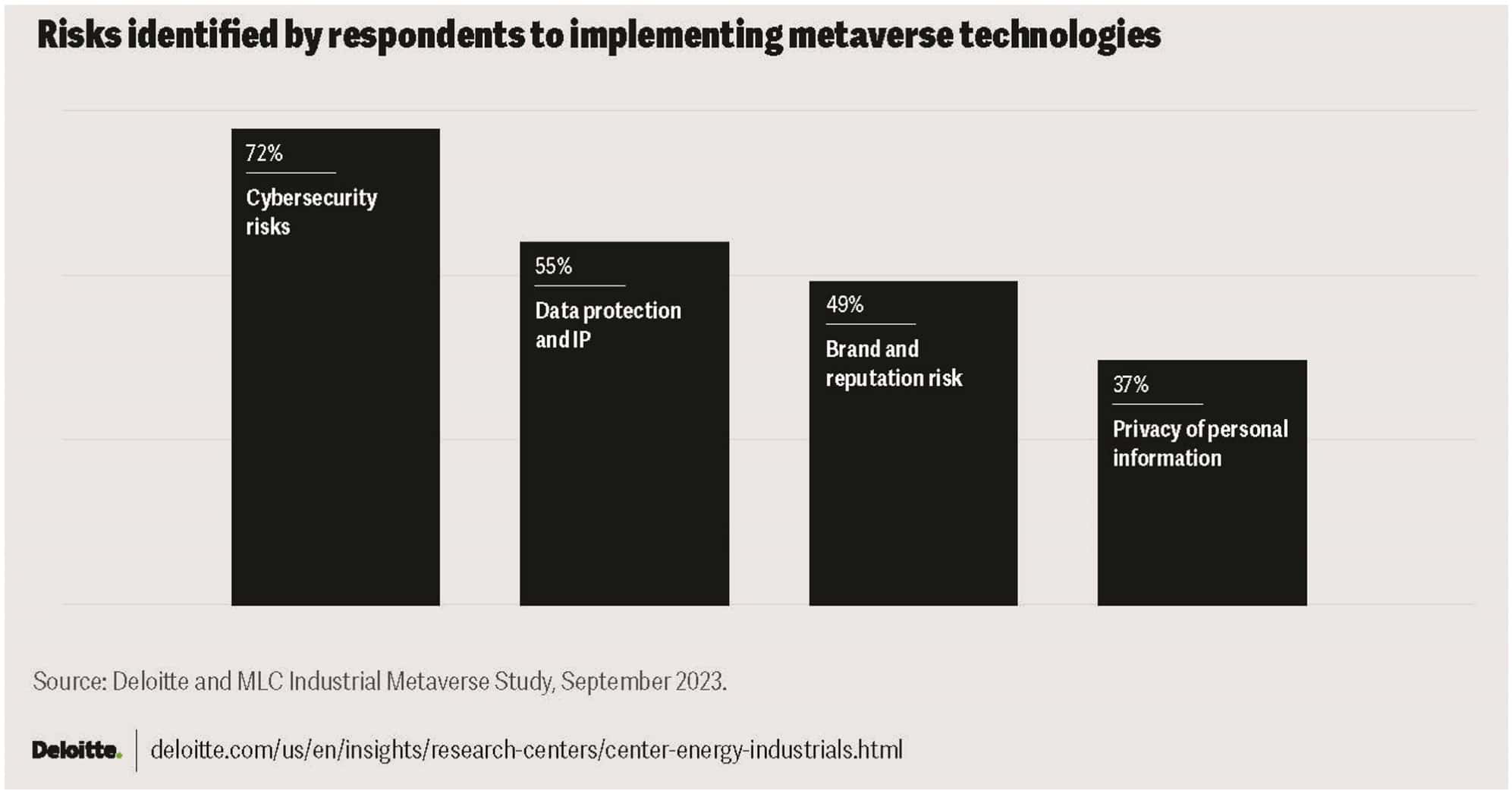

● Among the chief challenges with the Industrial Metaverse are cybersecurity, data protection and IP, brand, and safeguarding personal information.

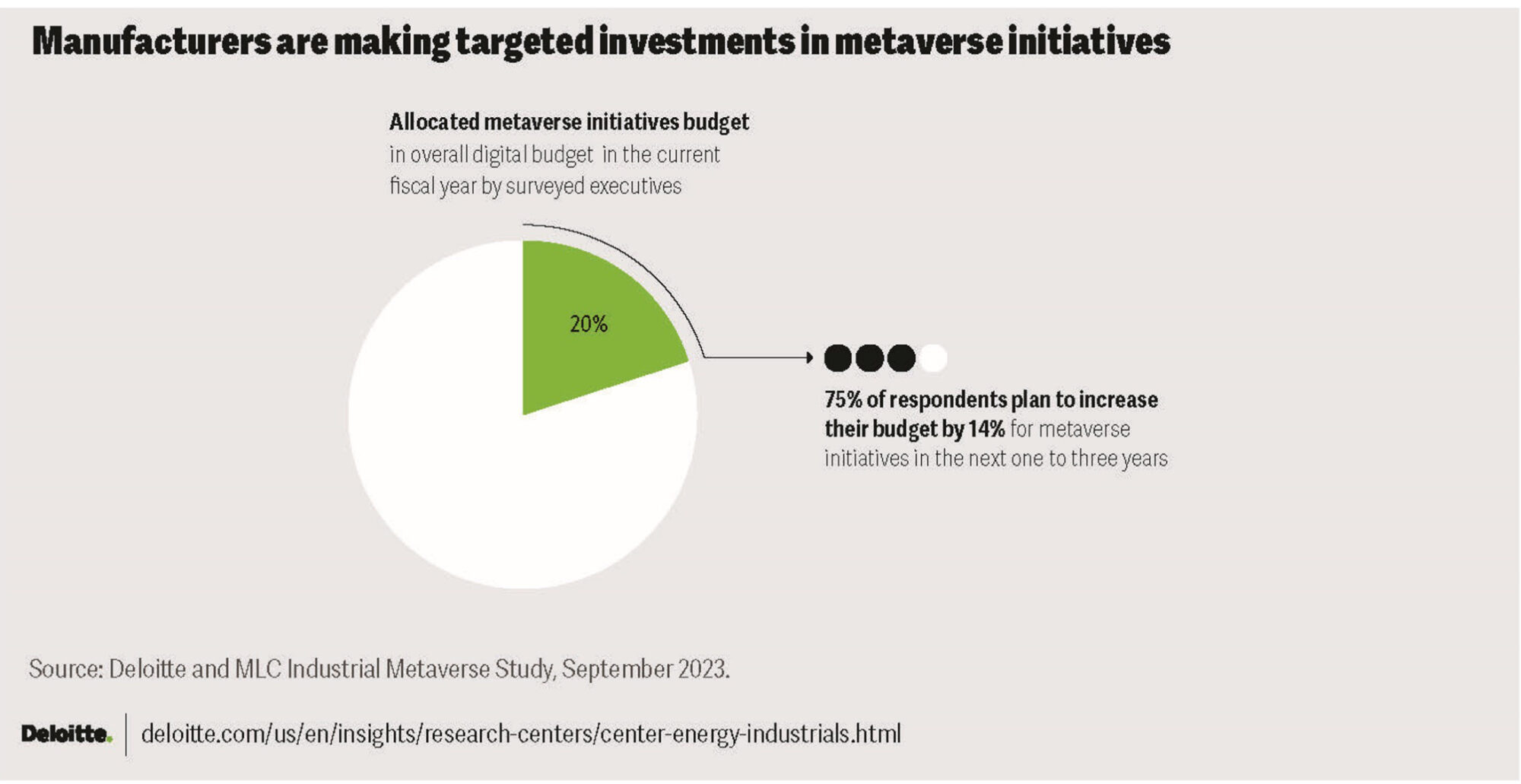

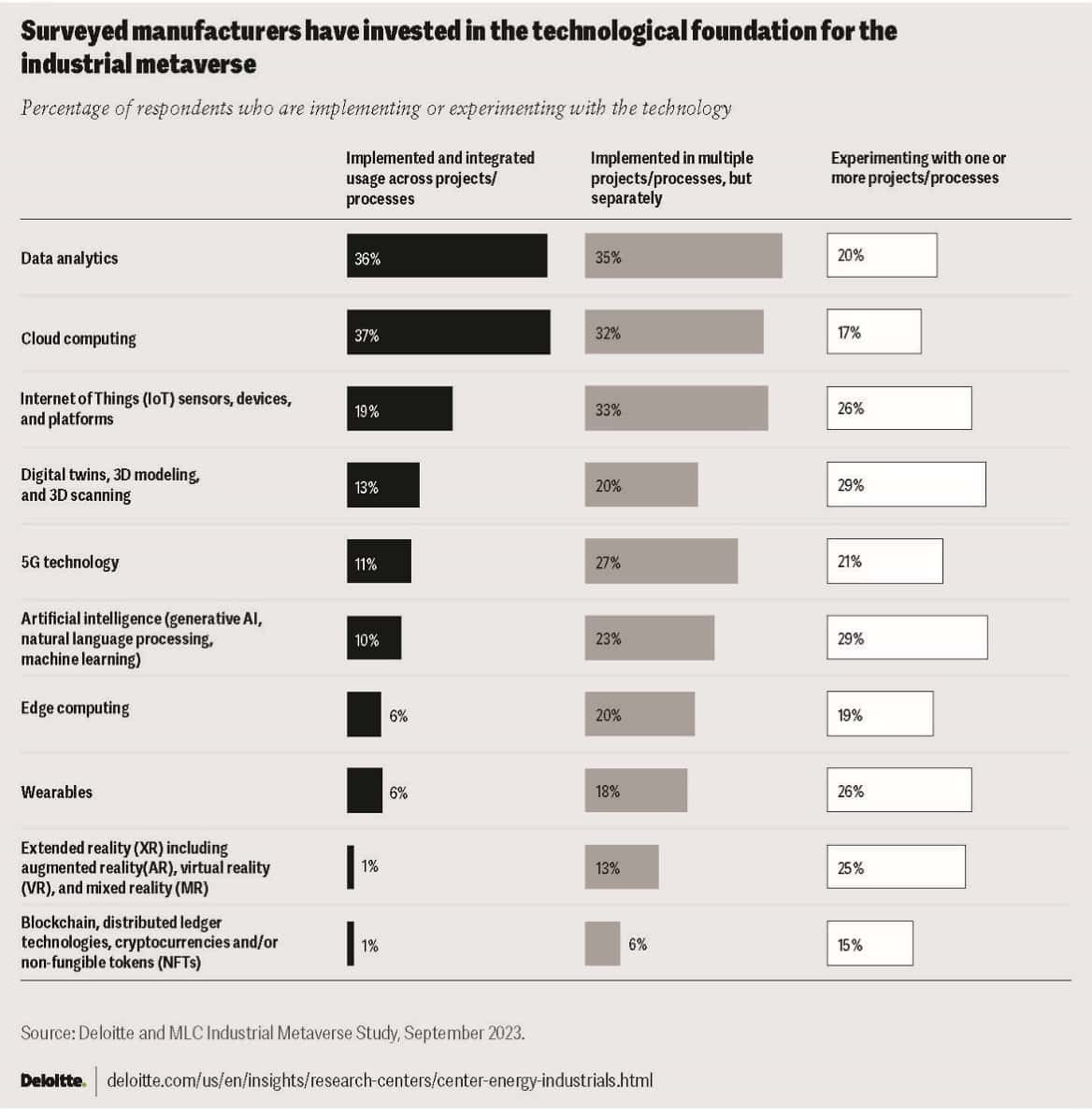

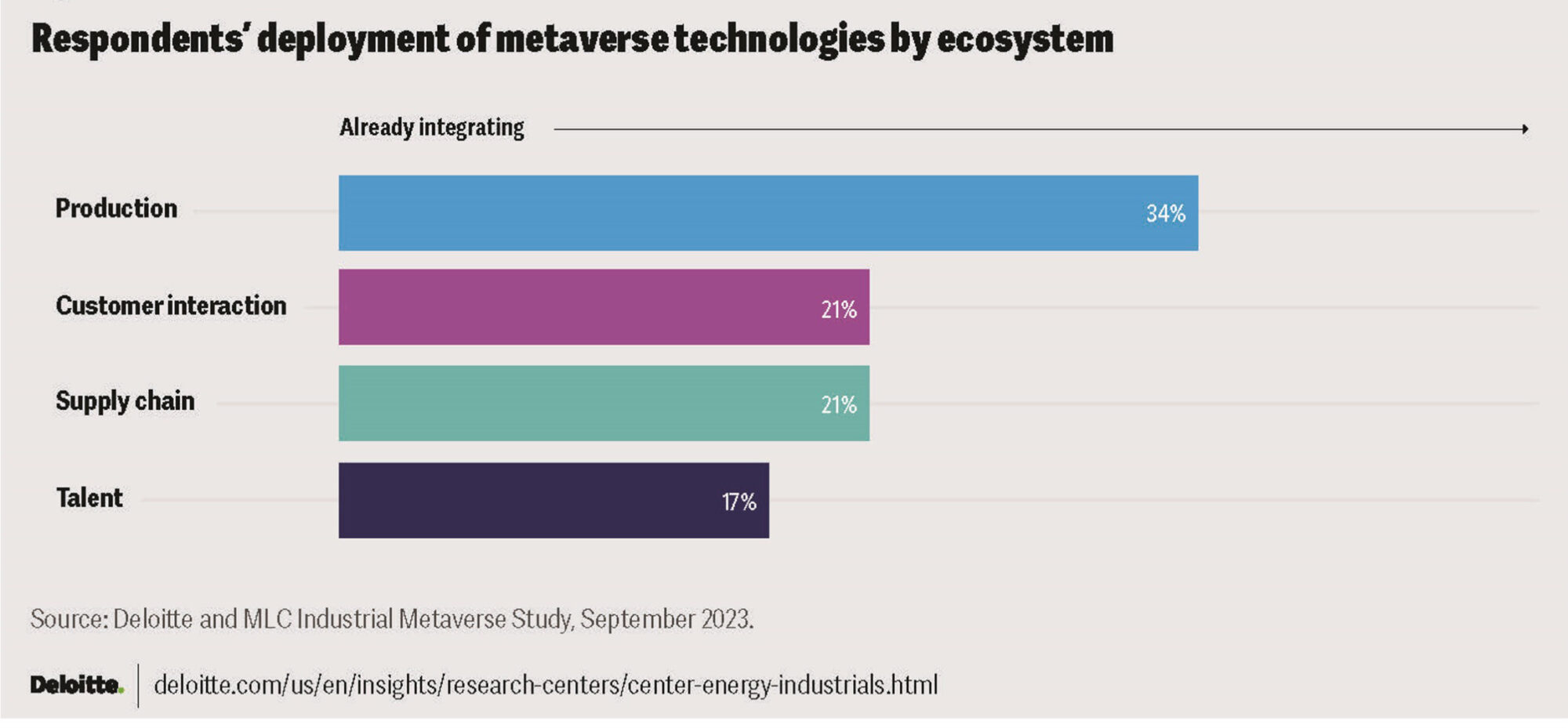

In May 2023, Deloitte and the Manufacturing Leadership Council (MLC) embarked on a study to better understand the industrial metaverse and its applications in manufacturing. This article presents some of the key highlights from the resulting publication “Exploring the industrial metaverse” (referred to as “the study” in this article), including findings that the majority of manufacturers surveyed are already progressing on their industrial metaverse journey and are deriving benefits from even partial adoption.

A Paradigm Shift

The industrial metaverse is the convergence of individual technologies that, when used in combination, can create an immersive three-dimensional virtual or virtual/physical industrial environment. As technology evolves, the industrial metaverse will likely allow access to these immersive 3D environments from any internet-connected device, including virtual reality (VR) and augmented reality (AR) devices, as well as smartphones, tablets, laptops, and equipment, from anywhere in the world.

A majority of manufacturing executives surveyed[1] are bullish on the potential of the industrial metaverse in the near term. More than 70% of surveyed executives believe that in the next five years it will have a high rate of adoption in the manufacturing industry. Nearly 80% are confident that the metaverse will transform R&D, design, and innovation and enable new product strategies.[i]